Uploaded 3 more videos in the past week-ish. Trying to keep em short and sweet. Still plan to write here, but the videos for the time being are taking a higher priority.

Debt Free Alpha on YouTube

2 Replies

Uploaded 3 more videos in the past week-ish. Trying to keep em short and sweet. Still plan to write here, but the videos for the time being are taking a higher priority.

This took out about an hour of my evening. Final Cut Pro X has a bit of a learning curve and I had to get my thoughts together. Hard to find energy sometimes after a long day at work + commute. Not giving up though.

401k: $65,831.25

Roth IRA: $4,425.07

HSA: $633.38

Total Retirement: $70,889.70

Car Loan: $5,374.98

Car Warranty: $517.00

iPhone 11 Pro: $1,235.68

Credit Card: $1,557.14

Total Debt: $8,684.80

Some of my payments will be posted next week, but I do plan on posting a 2019 year in review post in a few weeks. Overall observations about his month:

1. I really considered going on a vacation either to Austin or San Antonio, but I don’t think I would have the level of experience I’d desire with my current budget. I refuse to fly Spirit after my last claustrophobic experience in the back of the plane stuck behind the restroom. Places I want to stay are close to $200/night, my budget would be $100/night. The hotel we were going to stay at has some really sketchy reviews, charges a daily parking fee. The weather isn’t that nice right now either. Maybe I’m just making excuses.

2. Apple gave me more for my trade-in than I thought considering I got a credit on the taxes. Ended up being $1,515 vs $1,400. That’s fairly close to what I would have netted out to between ebay fees. Let’s break it down.

eBay Listing Fees:

Insertion Fee: $2.00

Listing Fees: Bold + Subtitle + Scheduled listing: $2.60

Electronics Fees (8% of the initial $50.00, plus 5% of the next $50.01 to $1,000.00, plus 2% of the remaining final sale price balance). Assuming $1700 sale price that would be $4+$47.50+$14: $65.50

PayPal Fees: 2.9% + $0.30 of the total selling price: $49.60

Shipping: Estimated $50.00

Total Fees: $169.70

Fees – Sale Price: $1,530.30

Not much of a difference and a lot less aggrivation.

3. I bought a few things for Black Friday. Between new shoes, bedding, a pair of jeans, and a shiatsu foot massage machine I spent about $199.53.

4. I just switched insurance providers from State Farm back to Allstate. It costs a little more each month, but…

State Farm doubled my payment, I switched to a monthly plan through from a 6 month lump sum. then took a whole 2 weeks to give me a credit.

Around the same time, the rep in the office tried to cross sell me some insurance I wasn’t interested in but ultimately agreed to. Then after signing up I got a letter in the mail saying I don’t qualify due to my BMI.

Their office moved what is now 30 miles away from I work. I have never met the actual insurance agent. I tried to give them the benefit of the doubt by scheduling a Friday call after work since their Saturday schedules are always busy… She never called me back. Then she calls be back all happy go lucky about wanting to discuss my insurance renewal two weeks later…

Really thinking about the next few years of my life. Perhaps overly so…. I’m not 100% sure what direction things will go. From an earnings standpoint should I continue in Marketing, explore options in IT, or ramp up my side hustle game. I could have a Bachelors in Computer Science before the age of 40. If I start now I’m confident it would take me 2 years. Assuming it takes me 2 years to get the degree I’d have to start out taking a pretty big pay cut from where I am now. Would it be insane to start racking up certifications as a backup incase my industry starts to move toward automation or we have a crazy recession? I’ve gotten burned before being a one trick pony

Software Developer Salaries Compared – Courtesy of Salary.com

I don’t think this blog is able to be monetized and that’s not inherently a bad thing. The traffic isn’t there, it’s honestly all over the place, and really specific to my own experience. I write for my own pespective instead of someone just getting started in Personal Finance.

It’s also not a Brand in the typical sense. Too close to debtfee.com which is a licensed LLC. If I am to blog with the goal of generating ad, affiliate, etc. revenue I’d have to pivot to a different name.

My goal is to start modelling myself more after the top 11 people I follow in the space.

1. Alex Becker – Entreprenuer, Popular on YT – 387k subs

2. Clark Kegley – Refusing to Settle – Passive Income- Entpreneur – Mindset – 292k subs

3. Jaspreet Singh – Minority Mindset – 515k subs

4. Nate O’Brien – Millenial, saves a ton of his salary, minimalist – 343k subs

5. Mr. Money Mustache – He’s the standard 32k subs

6. Mike Rosehart – Young guy, into real estate, is completely crushing it, 14.7k subs

7. One Big Happy Life – Great to see things from a family perspective – 178k subs

8. Ryan Scribner – Personal Finance – Entrepreneurship – Stocks – 502k subs

9. Madfientist – He hit F.I.R.E. super young – 9k subs

10. Joseph Carlson – He dives into the world of investing weekly. Big on dividend investing (I’m also trying to increase my retirement stash quicker than he is lol) – 58k subs

11. Andrei Jikh – Magic of Finance – Big on dividend investing, has almost $195k invested at 30 years old, saves close to 50% of his income – 251k subs

Stay tuned….

Paying off a huge student loan balance without a bailout is a huge accomplishment. That’s exactly what a fellow blogger did on the Double Debt Single Woman blog.

Her student loan balance started off at a whopping $112,258.42. That’s more than double mine, plus she had additional credit card debt of $30,340. That’s freaking insane. Her journey took a total of 21 years, can you believe that? She switched jobs, had bosses from hell, roommate drama, but still managed to contribute to a six-figure retirement account, for a net worth of almost $200k.

Here is where she started: https://doubledebtsinglewoman.com/2016/03/19/the-epic-student-loan-saga-begins/

And her latest update from last week: https://doubledebtsinglewoman.com/2019/11/20/ddsw-is-debt-free/#more-5108

I’m inspired by her tenacity, have been reading her blog posts for years at this point. I still plan to be completely debt free in a few months, barring any emergencies. Then on to the massive wealth accumulation phase.

Hope we continue to see more blog posts Woman! Thanks for sharing your story with all of us!

401k: $63,709.07

Roth IRA: $4,354.17

HSA: $498.74

Total Retirement: $68,561.98

Car Loan: $5,902.88

Car Warranty: 646.25

iPhone 11 Pro: $1,235.68

Credit Card: $3,079.55

Total Debt: $10,864.36

My credit card balance went up since my last update. Why might you ask? Aside from my veterinarian visit the other week… I decided to purchase this bad boy.

2019 16″ MacBook Pro. I did buy my 15″ Certified Refurbished model in April but the changes were a little too good for me to pass up.

The configuration I purchased has the following specs: 16GB 2666MHz DDR4, Amd Radeon Pro 5500 w/ 4GB of GDDR6 memory, new keyboard, 1TB SSD. For me the biggest selling points were the added storage, traditional scissor switch keyboard, 3x improved GPU performance over my machine, 2 more CPU cores. Apple offered me $1400 for the old machine which will reduce the above credit card balance and I got the education store discount oin top of it. I absolutely love this new computer, I played some games on Parallels without any lag. I could type on it for hours without getting carpal tunnel flareups, something I could not say with my old system.

I’m thankful that my income allows me to purchase the gadgets I enjoy, and my housing costs are fairly low. I do regret not travelling more in 2019. 4 trips – Palm Springs, New York, Boston / Provincetown, Las Vegas. Ok I guess that is a lot… 😀 For 2020 I’d love to go to Key West, Seattle, San Francisco, see my family in New York. At least one international trip.

Come June my goal is to stay true to the name of this blog and be completely debt free. It’s also when my 0% APR credit card offer comes to an end. I know I’m not going to become rich through my investments alone so exploring other possibilities. Not comparing myself to my friends who make $120k-$200k+ per year but it does make me think about what I could be doing differently to get closer to that goal.

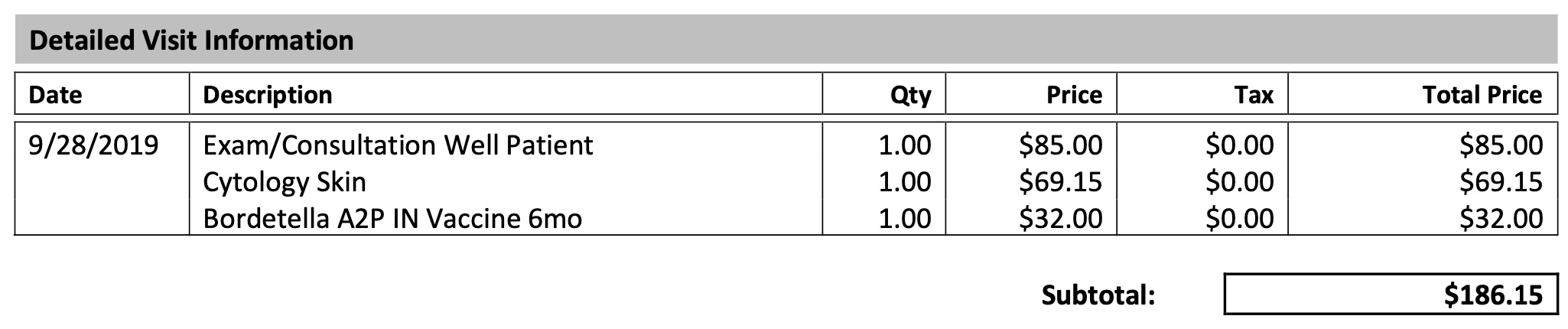

I love my dog. I recently spent over $1k related to her health matters.

The place gave me a quote for a dental cleaning + surgery removal that was been $900 and $1300. I decided that was too much and wanted a second opinion.

The place gave me a quote for a dental cleaning + surgery removal that was been $900 and $1300. I decided that was too much and wanted a second opinion.

The brings me to a combined total of $1,151.33. I love my dog, despite the huge vet bill. At least my card is 0% until May and I can probably pay this off in full within 30 days.

The brings me to a combined total of $1,151.33. I love my dog, despite the huge vet bill. At least my card is 0% until May and I can probably pay this off in full within 30 days.

“I’ll ruff to that”. She’s fine now, snoring away without a care in the world. Her stitches come out in a week 😀

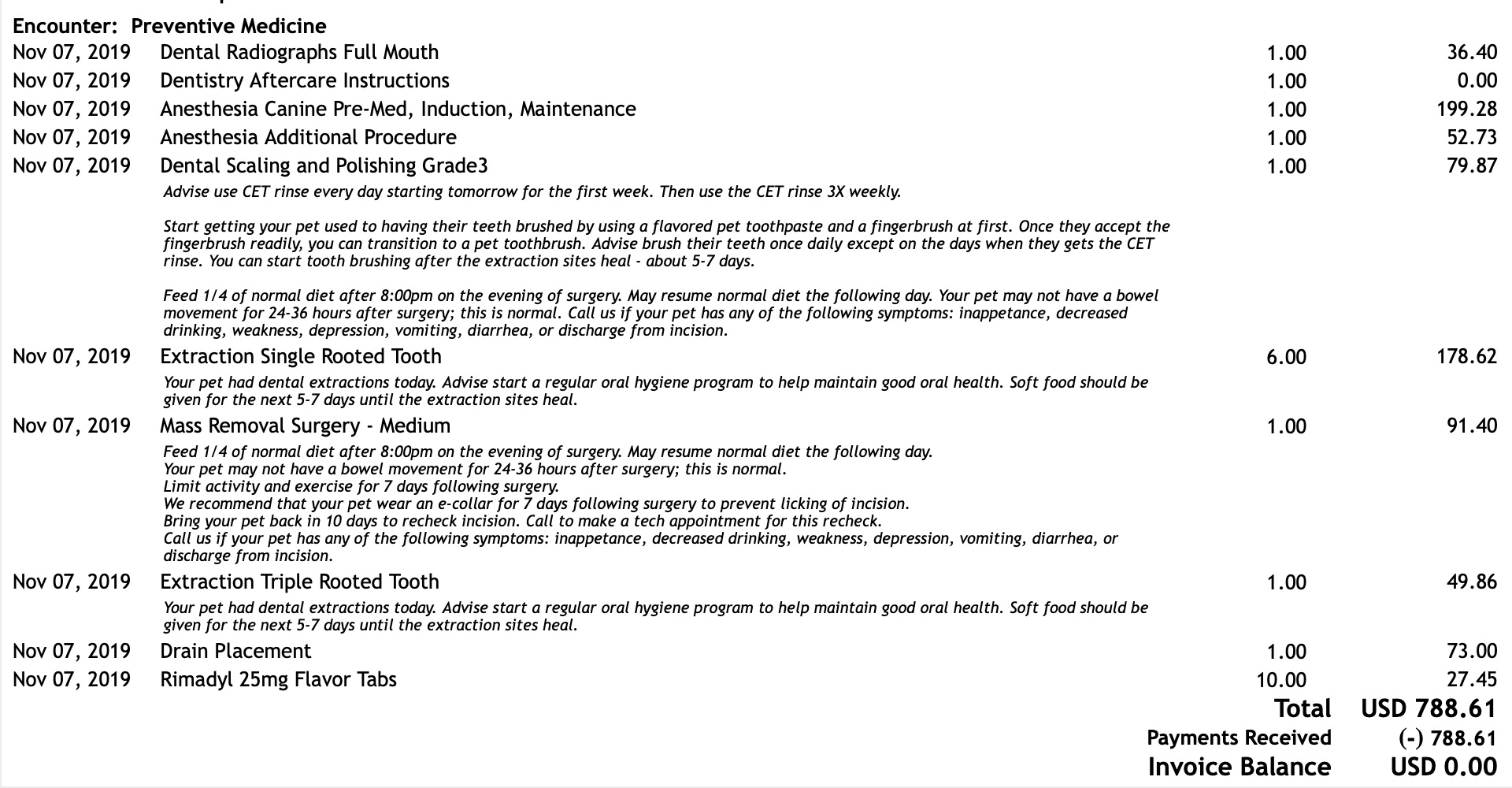

I’m chip chip chipping away at my debt, and investing. My dog is having a somewhat pricey vet bill coming up early next month. Cleaning and getting a small fatty lump removed. Probably will set me back around $400.

Recently found out that my employer is not giving out raises or bonuses this year. While miffed, I will take this over any type of layoff or downsizing. Many others are in situations where they are stressed beyond belief, facing health issues, or struggling to make ends meet. I’m just not growing as quickly as I want to. I need to commit to basically earning the 4% raise I deserve in my head through other activities.

401k: $59,897.07

Roth IRA: $4,184.82

HSA: 427.63

Total Retirement: $64,513.33

Total Debt:

Car Loan: $6,436.64

Car Warranty: $775.50

iPhone 11 Pro: $1,292

Credit Card: $1,328

Total Debt: $9,832.14

You may have seen my iPhone balance jump over the $505.60 last month. I’ve been on the iPhone upgrade program since June 2018 and decided to take advantage of it. Better battery life, camera, night mode, improved screen, fast charge. All features I will use on a regular basis. It’s still about $56/mo. After 12 months I can just swap it for the next new model.

I also have started experimenting with playing music as a hobby. At work I’m usually looking at spreadsheets, data, email. It’s nice to do something completely different, creative, and more right-brained in nature. So I bought an inexpensive MIDI USB keyboard that I can plug into my laptop and Logic Pro X. I played Twinkle Twinkle Little Star and the bass clef for Pachelbel’s Canon in D. My grandfather knows how to play, maybe some of that will rub off on me… 😀

Despite my recent purchases, I will be close to hitting a $0 credit card balance once I get paid tomorrow. Back to investing heavy in my 401k, getting the tax write off and hoping that I will have a huge nest egg in 2033.

Taking 5 minutes to type this up quickly before I head into work. Posting this to my network for a friend (who also happens to be a reader of this blog). He also used to be my neighbor, is a life coach and all around great guy. He and his partner recently had a house fire and lost everything. They have insurance but it won’t cover everything they have lost. Every little bit helps. So far they have 18 donations and have raised $2,040 of their $5k goal. Here is the Link to the Donation Page on Facebook.

Donate if you would like. I hope they can get their lives back together. ❤

Three years ago! That’s how long ago it’s been since paying off my student loans. I am still not debt free. However I have been net worth positive for years now. It’s a huge relief not to owe a single dollar to Sallie Mae / Navient.

401k – $59,450.66

Roth IRA – $4,158.89

HSA – $331.10

Total Retirement: $63,940.65

Credit Cards – $1,132.86 @ 0%

iPhone X Loan – $505.60

Car Warranty – $904.75 (7 payments of $129.25 left)

Car Loan: $6,969.80 (78% done paying it off)

Total Debt: $9,513.01

I decided to ditch Betterment for my Roth IRA. No complaints about them but I just don’t like fees. Going to invest in FZROX which has 0% in fees. Hope to have this completed over the next 3 weeks.

Taking my foot off the 20% 401k contributions for a month or so to get my credit card bill down to $0.00 and pay off the iPhone X loan. Kind of silly that I haven’t been able to pay either off for months and months. One of my friends is a life coach and I wasn’t able to pay the $2500 she would charge for 6 months worth of coaching without going into massive debt. I still am undecided about whether to sign up.

My office chair broke this week. I spent about $7 fixing it with screws and bungee cord. Couldn’t in good faith drop $200 on a replacement that still could have the same poor design.

A few weeks ago my car wouldn’t start. I got roadside assistance to give me a jump, then drove to the dealership with a $20 off coupon. Needed a new battery, this one at least has an 84 month warranty. With tax I was on the hook for $143.19. Later this month I’ll spend $20 on an oil change plus whatever else the car needs. i wouldn’t say it’s an endless money pit but minimum $1k in auto expenses monthly is wearing me down.

Then over the weekend I popped a spoke on my bike. About $30 to fix it again. I have the equipment to fix it but last time I tried, I popped a spoke again the next ride. Then I needed some more Keto Fire supplements, and replaced cologne that is about to run out. Little things add up. I saw some super fit people running outside my local Run On shop. Two of the guys took off their shirt in this 90+° temperatures and had six packs. I’m still around 240-245ish 5’8 and workout regularly. I know I can get to that point again in time, with the right choices.

Seems like all these people I know are travelling all over. I wonder where they get the money. Some have a sponsor, points, drive a 10 year old beat up car, or use credit cards. I take regular detox sessions from social media. It’s proven to be good for your health.

Last but not least no matter where you are in your journey, remember to love yourself. No one is perfect, we all make mistakes in life. One of my friends former roomates was struggling with severe depression early this month. I never met the guy but saw my friend posted it had been 2 weeks since the guy passed away. Dude was in his 20s too, so much life ahead of him. Then another story of a guy who asked for a paycheck and his boss shot him. Two degrees of separation. Now the family and friends have a gofundme page up to help with the burial.

My grandmother’s would be 80th birthday is coming up. We lost her 20 years ago and my dad 5 years after that. There are only like 2 people in my family I talk to with any type of regularity, none of them live within a 1000 mile radius of Texas. Gets lonely sometimes but that’s how things are. Making new friends hasn’t been easy. I’m practicing letting go of negative thoughts and visualizing the benefits of meeting new people. It’s not easy, but the alternative just isn’t working for me. Old and bitter is not a good look on me.

Someone on one of the forums reached out to me asking what I do that’s Mustachian. My answer was pretty lame, I basically said I stop worrying about money along with a few other things. Coming from a position now of being able to fully articulate my thoughts.

1. 20% to Retirement – Even when the market is getting a beating I still contribute 20% of my gross wages in my 401k. 95% FSKAX and 5 % in bonds.

2. Take lunch to work – At least 3 times a week I bring lunch with me to work. Usually it’s a salad with some extra protein and toppings tossed in.

3. Get gas from Costco. Considering my round trip work commute is 35 miles a day x 5 or 175 miles a week that adds up. Car gets 24mpg so that’s usually 8 or 9 gallons a week at the bare minimum. Double that for everything else outside of that… So 18 gallons @ $2.40 for premium is $43, two other stations nearby are $3.00/gal which would be $54. So $11/wk savings or $572/yr

4. Cut the cord – I don’t pay for cable. My parents do and I log into their account for what I need. My boyfriend has Hulu and Amazon Prime so occasionally we will watch that.

5. Got rid of Amazon Prime – My subscription just came up for renewal. Prime is $119 per year. I rarely watch movies on there, dislike their music app and I don’t have a smart speaker. If I am patient with shipping and shop around I can often find product for cheaper.

6. Use points – With my Chase Freedom Unlimited card I’m getting 3% cashback on all purchases and 5% through my regular Freedom card in rotating categories.

7. Renting – I rent a 1br/1br apartment in a suburban neighborhood. It was built in the 1980s. It’s not the lap of luxury but I’m also not worried about getting shot at night as would be the case in Downtown Dallas… I pay about $915/mo. Not saying I will never be a homeowner again, but taxes alone for property I’d consider would run around $5k/yr. That’s 5 months of rent. Who knows what 2020 may bring. I do see folks coming down in price on their expensive homes though.

8. Use rewards points – When I do go out I try to use apps like grubhub or Ritual for takeout food. With Ritual I got $5 off my first order, frequently saw $5 off Deals and 20x points (every dollar equals a point and at 10k points you get a $10 off bonus coupon).

9. Intermittent Fasting – Ok so this one isn’t for money but I have some extra lbs I want to burn. Skipping breakfast makes that process a lot easier since my body uses its fat reserves. I do consume some tea however to help suppress my appetite.

10. Travel Hack – When I do travel, I will look up prices with a service like Google Flights or Expedia. I refuse to fly Spirit or any other airline where I will feel like a sardine stuffed in a can. I try to avoid travelling on major holidays because the prices can often be double. During my trip last month to Provincetown I did an AirBNB with 4 others and split the costs. The friends cooked a few meals at their home. Little things like that add up, $20 here, $50 there.

11. Buy Discounted Tech – I never pay full price for any of my products from an Apple Store. Sales Tax alone on a $2k mac is $180. Then the prices can be hundreds more than an authorized reseller. I got a Microcenter Apple certified refurb mid-tier MacBook Pro for about $1999 vs $2799 brand new. It looked brand new when I got it, screen is great, battery works fine, no issues with the keyboard.

12. Drink out less – Some years ago when I did go out to dinner I’d often get 2 or 3 drinks. Now I try to limit myself to one. I honestly don’t miss it, I can make myself a quick something or other at home.

13. Stop trying to keep up with the Joneses. I could lease a BMW, Mercedes, or Lexus I wanted to. Maybe one day I will, but for the time being I am perfectly fine with my 3 year old Nissan Maxima.

14. Keep insurance. Without insurance I likely would be borderline bankrupt. Or struggling to pay $50k worth of medical debt. I hate paying the premiums, but it has saved me from huge expenses over the years.

15. Max out my HSA – HSA is a great concept. I get a tax deduction and can use it for things like a blood pressure monitor, orthotics for plantar fasciitis, my braces, normal doctor visits. Since I have a high deductible savings plan this is a also great buffer from unexpected medical expenses. Once I hit a savings certain threshold I can turn it into an investment account.

16. Avoid high interest and maintain good credit. Even with my student loans, after consolidation my interest rate was 4.25%. That allowed me to get ahead much quicker than others with 8, 9% or higher. My car loan is 1.9%… some people with subprime loans pay upwardsof 29%. Not blaming them, but it’s really a night and day difference.

17. Don’t lease a car – It’s different if you own a business obviously. If you have a monthly car payment that never goes away, you have no assets after 3 years. Then if your mileage goes over the terms you’re paying extra. I’m 76% done paying it off my car right now. Then I will own it, not the bank, not Nissan Motor Acceptance Corp.

18. $1-2 movies – Haven’t been in a while but occasionally there will be something that catches my eye. Occasionally I’ll sneak a snack in. Is it ethical? Maybe? But…I usually don’t like what the theaters even have.

19. Pay for a 12 month Apple Music subscription with discounted Apple Gift Cards Per month Apple Music is $9.99 ($4.99 if you’re a college student) . That’s $120 vs $99 for the annual one I have. I got a 33% discount on mine through Best Buy Rewards points, 20% sale on Apple Gift Cards at Best Buy, combined with 3% cashback on my credit card.

20. Get someone to cook for you. Food always tastes better when someone else cooks for you. Especially when they know what they’re doing. We can eat at home, then grab a drink somewhere out if we choose to. If there’s a Happy Hour special running, even better.

21. Buy Clothes on Sale – I like discounts. Clearance, sales, almost every retailer in America offers some type of deal. Even name brand designers should be on sale.

22. I wash my own car. Usually pay about $5 a week at one of those self serve bays instead of $10-15 by going to one of those modern car washes that often scratches your car.

23. I switched to a low cost energy provider. I’m projected to spend $73 this month, but typically average out to around $50.

So there you have it. 😀