Usually I’m against these things on principle. I did however decide to purchase a 96mo/120k mile warranty for my car. My thought process is below:

I purchased my 2016 Nissan Maxima in March 2016. My purchase price was approximately $31,380. Currently owe $14,840.54. Overall I still like the car, but….

I’m at 35k miles. Past 36k, I can no longer order an extended warranty for it and have it be considered a new car. The bumper to bumper warranty is 36mo/36k miles, powertrain warranty is 5 years/60k miles. Currently between work, social life, and random activities I drive about 15k miles per year. That puts me at around 5 1/2 years or March 2024.

Couple of quotes off a forum I’m on for the same model:

1. “Need help….. Any Nissan techs on here?? who can I call to escalate a warranty claim. Driver seat motor seized 45 k miles dealer wants $350 for new motor showed me a seat invoice for $3,400 claims Nissan will pay 90 percent. Also said cannot just replace motor in driver seat need to order entire seat etc. I feel like that’s bogus and they are just taking a shot at me.” Then after a few comments were posted: ” It’s a lease. They can have it back broken”

2. “At 24k Miles I had transmission failure which was very disappointed Nissan warranty covered it all but I feel like the car is compromise who else had trans problem” … a second person posted “mine failed at 2K. what was the issue that caused the replacement?”… a third said “Mine failed at 48k” … a 4th “Mine failed at 18k. And the wheel bearings. And the driver seat. And the windshield is next.”

3. “Navigation screen went dark on my 2016 Maxima for 1 minute then rebooted. Should I be concerned? Car is out of warranty”

4. “Has anybody had their USB 1 port go bad? Dealership said it needs to be replaced so no CarPlay for me at the moment. They quoted me $360 for the part and labor. And no, I’m not under warranty anymore. Wondering if I could take it on myself…”

5. “I’m getting my radio replaced!!! Woohoo!!!! The Bluetooth issues I asked y’all about was annoying. I couldn’t take anymore. Thank goodness I purchased the warranty!”

6. “Hey guys, I’m a little worried…

My son came over today with his Altima and we needed to go to the store, so I let him drive my Max. My son used the keyfob to do the auto start, and then got into the car. When he put it in reverse, my husband stopped us because he heard something in the engine that he described as sounding like a plastic spray paint can being breaking like it was being run over–no we did not run over anything in the garage.

I didn’t notice anything when my son was driving, but when I made a quick run to the grocery store, I noticed that between 35-40 the car was doing the kind of surge and let up that I have felt it do in cruise. It has never done this before today. Could this be the beginning of the CVT problem that people have been talking about? I’m concerned because at over 25k, I’m coming close to my warranty expiring.

Have you experienced something like this?”

7. “Has anyone experienced a clunking noise when going over bumps or corners.Just got done with the dealership and they said its the connecting rod and will be covered under warranty.”

Since this current model debuted only 3 years ago, maybe there are some design flaws that just haven’t manifested themselves yet. So let’s compare to the 7th gen Maximas…

1. 9/2015 : “Gotta love that warranty baby!!! Should have her back by Tuesday… Somehow the motor blew and thanks bro”… I bought a 100,000 miles 5 year warranty when i bought the car..block cracked so I couldnt keep anything every little piece has to go back to nissan and I have 68,000 miles on the car” See picture of a brand new engine below the post.

2. 12/2015: “Loving this warranty… Fixed seat track, blown shock, and realigned car… # winning” Then I see a picture of a bill for $1,971.10.

3. 4/2017: “So its confirmed I have the Main Bearing Issue 😒 right outside of the warranty. Should I panic or nah?” His car only had 67,900 miles. Another person commented “I had my long block replaced at 5700 on my 2014 under warranty…the cost on the invoice was $8,300 if I had to pay out of pocket”

4. 3/2017: “Well the extended warranty approved the work and getting a new transmission 🤷🏽♂️ let’s see how long this one last 😂 also wanna thanks my dude XX XX for helping out with this. If not they would of denied that XXXX”

5. 2/2017: “Glad i brought that extended warranty. $2000 parts and labor. All i had to pay was $100.. lower control arms. Front Wheel hubs. Slid him a few bucks and he changed my belt too..” …. “The rubber on the control arms basically dry rots and starts tearing. They noticed it awhile back and pointed it out to me. Told me i would need them replaced in the near future.”

6. 4/2018: “This car…. as soon as it’s out of warranty the factory head unit goes out. Then the A/C. Now it’s just reading whatever now. Car is almost paid off and I just started moddinh. Now I have electrical issues. Emissions are due at the end of the month and I cant even pass.”

7. 7/2014: “Just left the dealer. Maxi needs $2k in repairs and warranty just expired. Guess I know where my tax return money is going toward. Smmfh.”

8. 10/2015: “This is what I was quoted today by Nissan Service department. My warranty covers everything but the front Struts, 2 front tires, rear taillight, and the 60, 000 miles service tunes up. After doing the calculation that’s a whole lot of money.” Proceeds to show a bill for $5,246. THe biggest of which were the steering rack, motor mount and tail light unit.

9. 2/2017: “So my 2010 with 126 (6k outta warranty) cvt just flat out died no warning no signs no issues…only person happy about this was the dealer because they wanted me to trade up for a 17 SR a month ago…shoulda took the deal when I had the upper hand..#cvtboom”

10. 4/2016: “Yup! Just got the news it is indeed my AC compressor that died. Thank GOD I kept that extended warranty because I was seriously contemplating cashing it in as this car hasn’t given me not 1 issue in 2 years until now. But even then I will take that as opposed to anything pertaining to the engine or CVT. 😊”… “Didn’t cost 1 cent with my Platinum Extended Warranty😁. Just have to bring it back in the morning because the part isn’t in stock. But that’s like an $700-$1000 job….ughhhh”

I considered trading in for a different car in a less premium class. After factoring in present / future depreciation, a new set of tires I recently purchased, how few other cars on the market have both the power / size at a comparable price point, sales tax, markup, miscellaneous fees… The decision was very clear. Keep it, pay it off, in 18 months it and the warranty will both be gone.

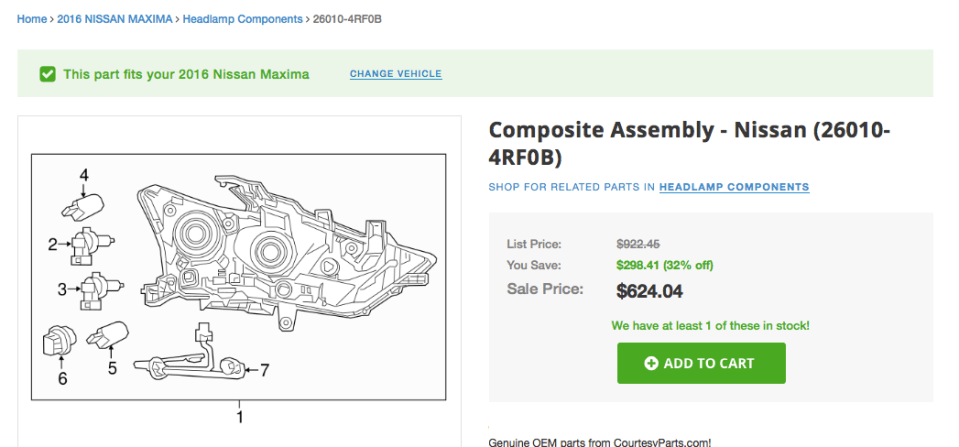

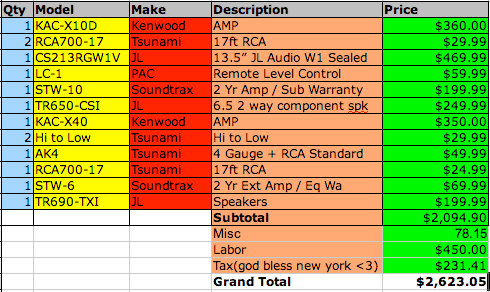

I’ve already had to make one warranty claim for moisture in my headlight. The part alone costs over $600. Then add-in labor associated with dropping the front bumper, removing the old unit, installing a new one, and reattaching the bumper…

How much did it cost? $2,585 total, 0%, $258 up front and 18 payments of ~$130. This will cover me for 96 months from my vehicle in-service date, up to 120k miles. 8% of the original purchase price of the car. I did try shopping around at 2 local dealers. One only wanted to cover me to 72k miles for the same price. I politely declined, another only offers warranties through Fidelity Warranty Services, which has a ton of negative reviews… Another never called me back even though I emailed them, and spoke to a salesperson and receptionist…. I know, not the most exciting thing in the world… Short of getting a cheap used car and driving the wheels off it, I do think I’m setting myself up for long term financial success.