Month 49 Update

As I mentioned the last month… I did purchase a new car, am not relying on credit cards each month and putting aside more money toward emergency funds. As a result, I decreased student loan principal balance only by $592.32.

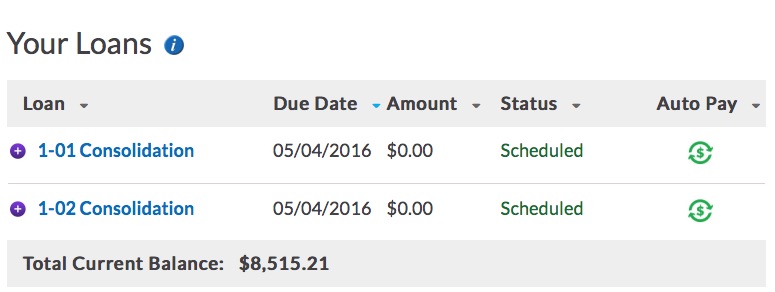

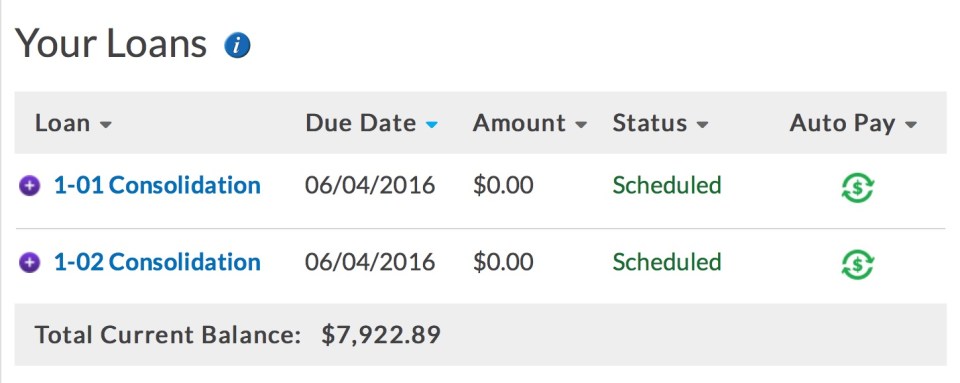

Navient: $7,922.89 @ 4.25%

NMAC: $31,188.19 @ 1.9%

Credit Cards – To be completely paid off by end of month

$69.08 (Costco Amex – groceries + gas)

$502.73 @ 12.24% (Chase card used for food / Amazon / utility items mostly)

$41.21 – Department Store card for mother’s day gift.

Total Credit Cards: $613.02

Total Debt: $39,724.10

Savings: $2800.02

This figure includes money earmarked for emergency fund, rent, car payments, etc.

Retirement:

401k – $15,166.29 – Up $1,691 since two months ago. Only $10,108 is vested.

Roth IRA – $3,315.10 with Betterment. My earnings are still -2.5%

Brokerage House – $564.07 – Down 10% due to AAPL. Might be a buying opportunity for more shares if it dips lower. Only own 6 shares which is about $3 a quarter in dividends.

Total Retirement – $19,045.46

As expected, my car insurance went up since buying the new car. $703.88 it was $592.95 before. For 65% more horsepower a 19% increase in premiums isn’t bad. I also switched everything over to e-policy to maximize my savings. Still have uninsured motorist coverage even though I have never been involved in an accident in my 15 years of driving. No tickets on my record for Texas and the ones I got in NY are no longer a factor.

Do I have any regrets about buying the car? Nope, it feels like a car that is truly made for me. Cockpit-like feel to the cabin, the effortless acceleration of the VQ engine, the exterior ground lighting, the LED daytime running lamps, no body roll in corners. Those shiny aluminum alloy rims on 245/45R18 Continental Procontact tires too. So much grip in the corners and 0-60 in 5.9 seconds. Put it in sport mode, the steering tightens up and the throttle is super responsive. The $30k 4DSC. Guy I work with with a Mercedes Benz CLA complimented me on the car, said he thought about getting one but it was 6 months too early.

2016 Nissan Maxima SV – Added $31k of debt but excites me every drive

I may be obsessed, I try not to park close to other cars and only wash it by hand with Optimum’s No Rinse car wash product. Was paying $40/week at the gas station wash with my black Altima and the results were mediocre. $15 at the regular car wash only to see a ton of swirl marks from their highly abrasive “soft touch” brushes. Now I do it all myself and can have the car completely done in 30 minutes. My absolute fastest washing the car by hand was 15 minutes. Yes I use a grit guard, microfiber towels and do a pre-spray to loosen up any dirt first, but…can’t recommend the product highly enough.

Last but not least… I decided to get serious about losing weight again. That was one the span of about a week. I threw my 6 individual packs of Famous Amos cookies in the trash. For breakfast I switched to eggs and protein (bacon, sausage or their veggie equivalents). For lunch I eat a salad and a protein source. I try not to go overboard with anything that has sugar. The protein fills me up and I crave the junk food less less. In 2015 I was 215 just to put things into perspective. The last time I did the ketogenic diet was 2012 and I got as low as 207. I was too extreme though with it and feeling dizzy all the time. Now I’m just being less hardcore while still enjoying carbs.

What good is money and fancy things if you aren’t in decent enough shape to enjoy it? This is after about a week.

Hoping to continue the trend and be in the 220s next week. Being fat and tired is not the way to live a rich, fulfilling life. Stay tuned. Thanks all for sticking around and reading all my posts.

Last but not least… Joe made a new post about 4 years later on No More Harvard Debt. Check it out. His book is pretty good too. My approach / situation / income varies but at my core I still enjoy not wasting money on things I don’t enjoy and cut back on things like food, entertainment and clothing to help reach my long term goals. Live With Passion! 🙂