One of the benefits offered by my company is a certain percentage of my gross salary is vested toward retirement. This is separate from the 3% company match. This year that number was about $1100. This boosts my 401k balance to over $12k.

I’m shifting more and more toward a retirement mindset and less from becoming debt free as I get closer to paying Navient off.

These are my loose plans and I honestly have no clue what the future holds for my career / earnings potential, living / relationship. numbers I came up with on my current salary, which for arguments sake say it’s close to the national average.

2017: $1000/mo -> +$12k -> $24,000

2018: $1200/mo -> +$14.4k -> $38,400

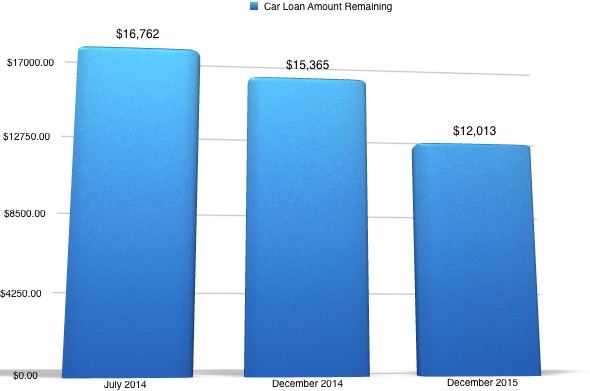

2019: $1500/mo (maxing out 401k) -> $56,400 (car will be paid off)

2020: $2000/mo -> $80,400

2021: $2000/mo – > $104,400

2022: $2000/mo -> $128,400

2023: $2000/mo -> 152,400 (the year I turn 40)

2024: $2000/mo -> $176,400

2025: $2000/mo -> $200,400

2026: $2000/mo -> $224,400 (age 43)

Using the 2020 numbers as an example with a future value of money calculator…

$80,400, adding $2,000 per month at age 37 @ 10% interest and continuing for 14 years. That makes me a millionaire and able to retire by age 51 assuming my income stays what it is and my cost of living doesn’t suddenly spike. If I take that $1,051,771 and don’t add anything to it, in 10 more years at 10% I’ll have $2,847,188 at 61. Is $2k a month a lot of money? To me in 2016 dollars on my current income yes. In 4 years assuming I get a 4% raise each year? Maybe not.

I don’t know what the future holds, but I do know this. If you want to have money when you’re older you need to start young. Maybe that means not buying the Mercedes or BMW but a more modest car instead. Or renting for a while and not sinking a ton of money into a house. I’m really seeing the light on how the poor stay poor and the rich get richer.

Last but not least, here’s another big kicker. There are people making $100k+/yr now who could easily speed this whole process up considerably and still have a decent life.

It’s late as I write this, but I just hope someone thinks about this before making a huge purchase that makes then a total slave to a job, bank or other financing company.

Put my mountain bike up for sale on Craigslist, asking 320 negotiable. I haven’t used it in a year. Was also wishing I’d find a boyfriend or even a friend that appreciated biking as much as me and would want to ride together. Got the bike in August 2013, none of those things happened and I use my road bike pretty much exclusively.

Put my mountain bike up for sale on Craigslist, asking 320 negotiable. I haven’t used it in a year. Was also wishing I’d find a boyfriend or even a friend that appreciated biking as much as me and would want to ride together. Got the bike in August 2013, none of those things happened and I use my road bike pretty much exclusively.