This post I decided to dedicate to the topic of people in my life making poor financial decisions.

Situation 1

One of my friends recently moved from out of state to the DFW area. She has been looking for work for the past few months. Thanks to her connections, she will likely be getting a well paying job within the next few months. The couple took out a 401(k) loan that they plan to pay back over the next few months. Without the 401(k) money as a resource they would be on seriously shaky financial ground. Flash forward to today, they just moved into a luxury apartment for the rent is $1300 dollars per month (my apt is a comparable size, in a slightly less desirable location but still 5 minutes away and $773). Eventually they plan on purchasing a house, but today she doesn’t have a job and for all intents and purposes he doesn’t have a job.

A few years ago they owned a home in another state that went through a short sale because of the downturn in the real estate market. For as long as I’ve known them the husband has not had a full-time job to help support his wife, instead he chose to pursue his passion for theology which doesn’t really pay well and he earns nothing from. I think most people would have a come to Jesus moment where they would work a job that is not ideal but helps their family hit their financial goals. This has not been the case.

The wife is also providing financial assistance to her parents and brother. My guess is this has amounted to over $100k over the past decade. It’s very noble that she’s cares so much about her family, but I don’t think she is concerned enough about herself.

It’s not my place to cast judgment on my friends, but I wish I was able to impart wisdom on them. They haven’t realized it now but I think they’re setting themselves up for financial failure in the long run. looking at the power of compounding, the importance of having a sizable nest egg and not living beyond your means, They’re failing on multiple counts. On the bright side I think she will be back on target in the next 2-3 years. I have tried to help the husband with finding a job but haven’t been so successful at that. He doesn’t seem very motivated and I can’t force someone to be driven. Sure I believe in the power of faith but also that god allows us to help ourselves.

Situation 2

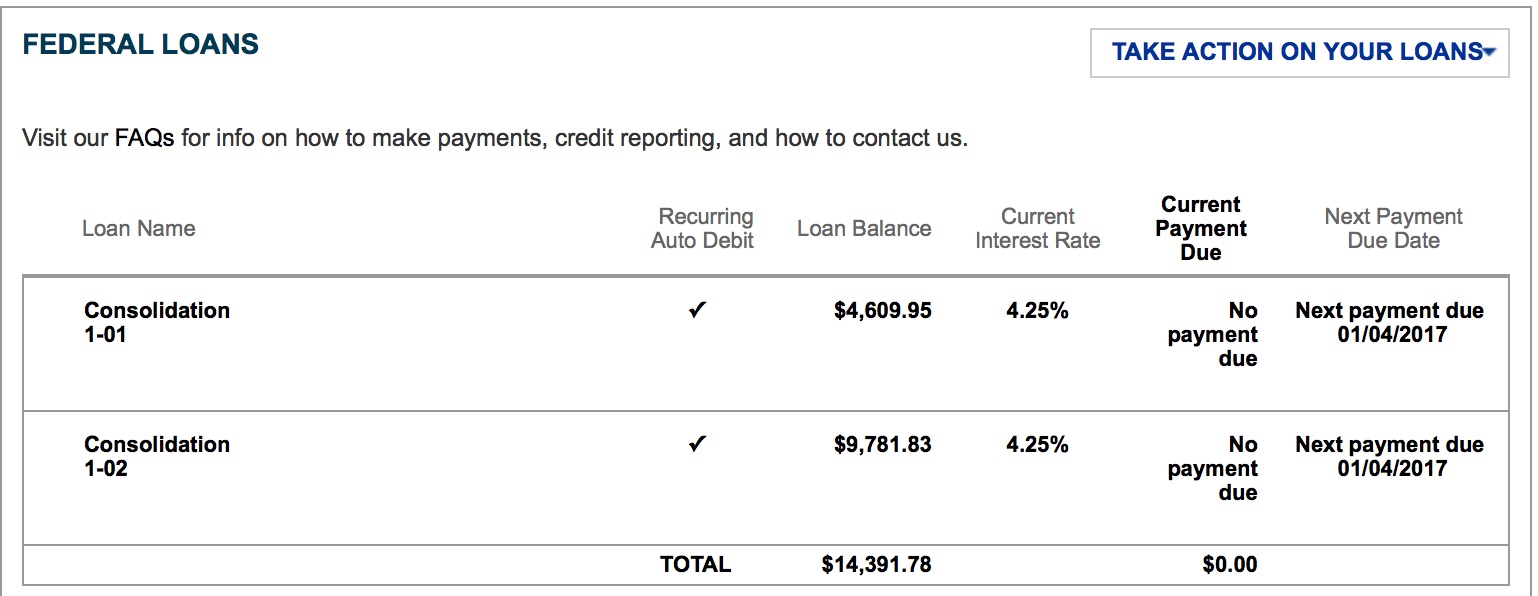

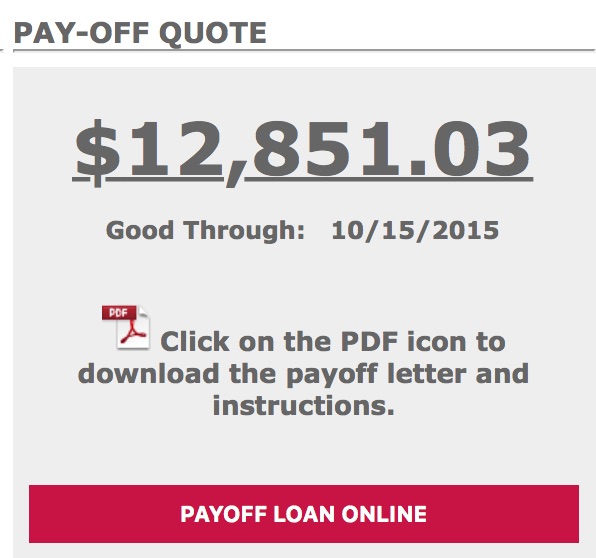

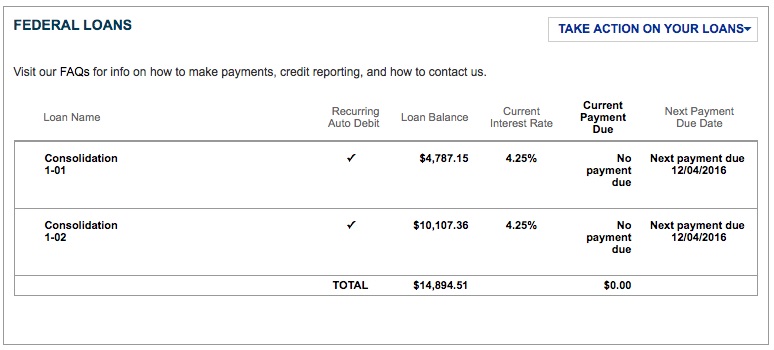

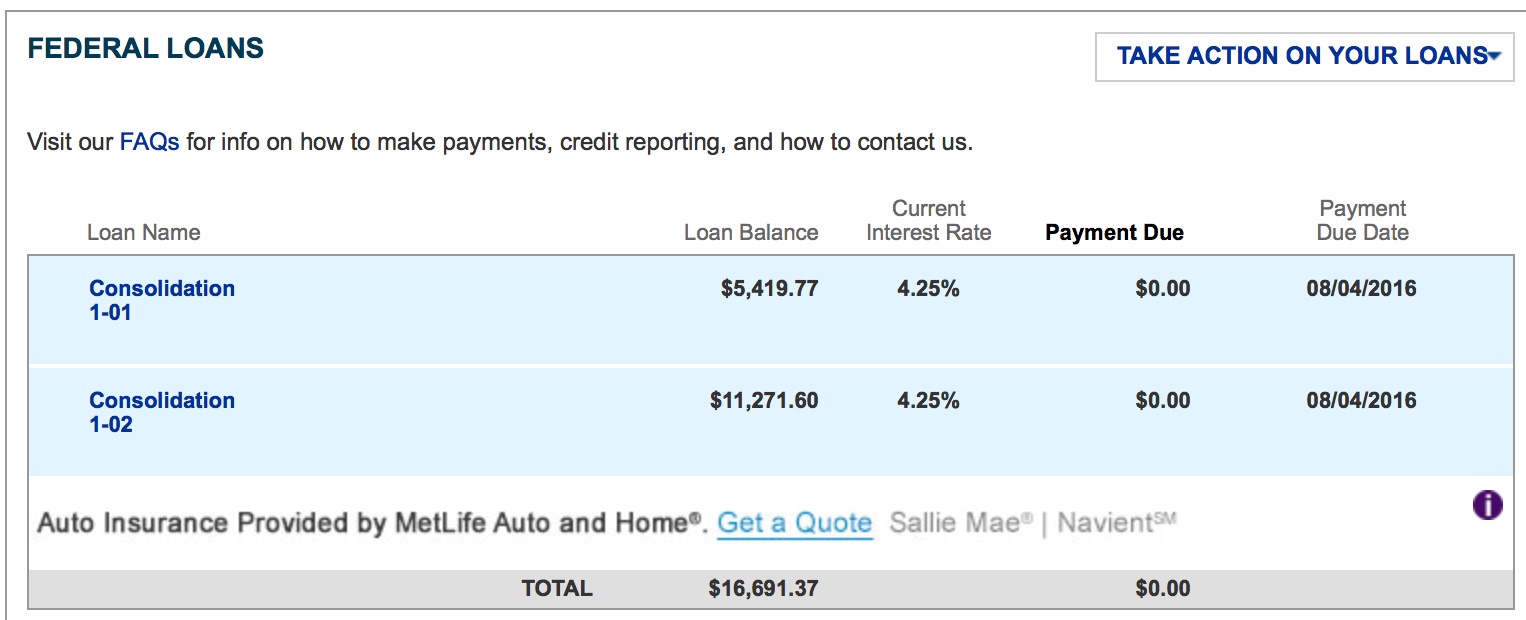

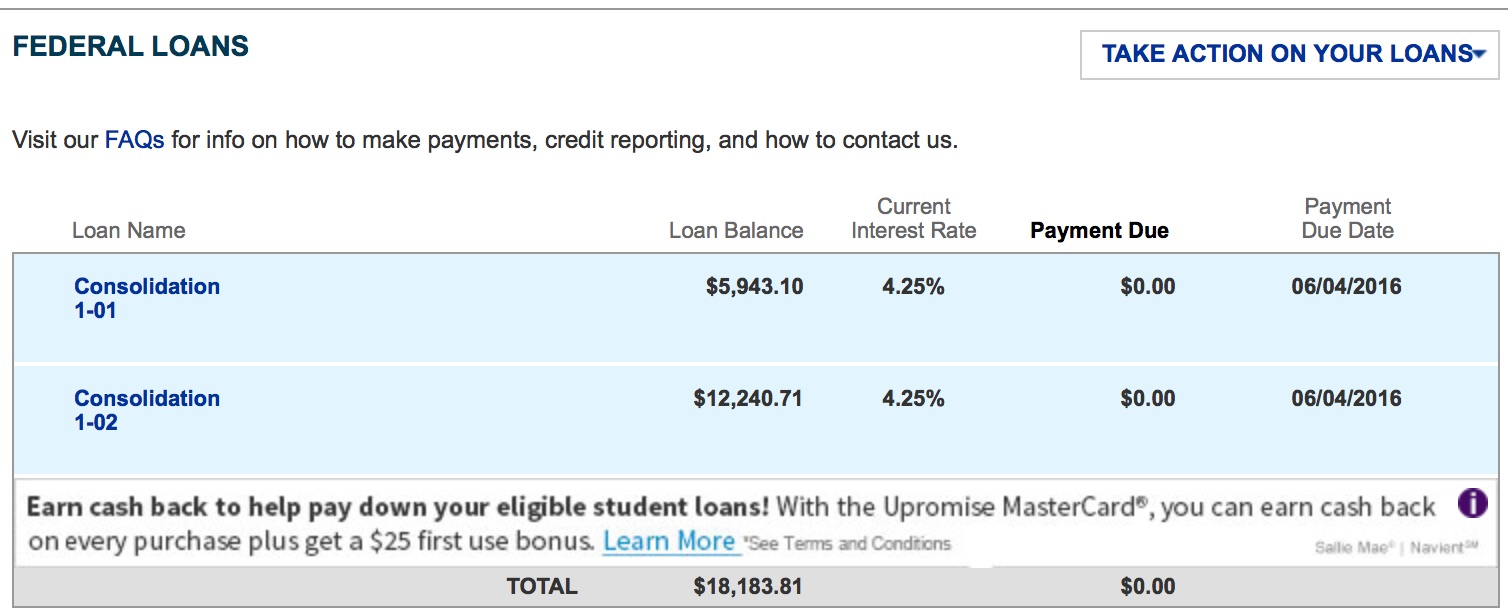

One of my other friends recently confided in me she has over $120,000 dollars in student loan debt. At what interest rates you might ask? Between 5-9%. Currently she is on the income-based repayment plan, commonly referred to as IBR. She quit her stressful corporate job and instead works as a babysitter. Although she’s well paid for what she does, she’s making minimum payments on her loans while interest accrues. Combined she and her husband grossed over $100k last year. Gross vs net though, two very different things.

Let’s look at a compounding. Starting out with a $120k balance and paying $300/mo. I don’t know exactly how much she pays but it’s probably less than that. I used this calculator so no idea how accurate the numbers really are.

Year 1 : $127,505

Year 2 : $135,713

Year 3 : $144,692

Year 4 : $154,512

Year 5 : $165,254

Year 6 : $177,004

Year 7 : $189,856

Year 8 : $203,914

Year 9 : $219,290

Year 10 : $236,109

Luckily in her case she is set to inherit 2 houses in the US and another in another country. Down to road she could sell those and be student free. Not everyone has this luxury and what does that leave her with? An underfunded retirement plan, no real estate and probably some hefty tax bills. She’s given up hope and is just paying what she can for now.

My father died with serious debt. Over $50k as I recall, mostly from medical expenses. I wasn’t blessed with a silver spoon in my mouth. I’m not perfect. I love my friends and family and wish the best for them. Seeing my father poor from the age of 2 up until I was 20 left a lasting impression on me. He didn’t have any much control over his situation, due to his renal failure. As long as I am able to I’m gonna fight damn hard to learn from all of this. To do otherwise would just be plain ignorant Life is more than money, but a few poor decisions can haunt us for a lifetime.