Lowering my automotive expenses has been top of mind lately.

Tires

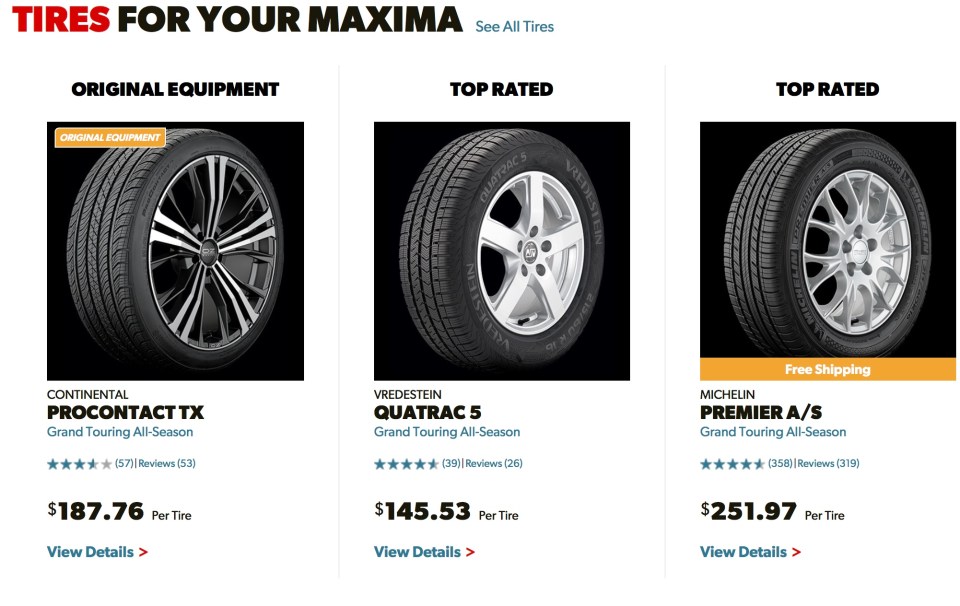

Hovering around 30k miles, the stock Continental Procontact TX tires that came on the car were ready to be replaced. I rotated them, maintained proper air pressure, never did J turns, burnouts or anything crazy like that. First it was the sidewalls beginning to show cracks, then some really bad hydroplaning even in light rain. I read reviews where people said the sidewalls were weak and started to get bubbles after hitting potholes. So I looked at my options.

The top rated 245/45R18 tire was the Vredestein Quatrac 5. It isn’t a well known company in the US, but seems to be more common around Europe. A set of 4 tires for $582.12 plus $45.28 in shipping, for $627.40. Right off the bat I save $168.92.

The tires shipped to my local Firestone shop, I leave work a little early on a Monday, deal with 45 min of traffic, only to be told by the manager… sorry we only have one guy working and 6 cars to do work on. I ask about doing it the following morning and he nope same problem, come back Saturday. I say screw it and load the cars up in the trunk and backseat of the Maxima.

Drove to a shady looking tire shop in my area that is open a little earlier. With tax they installed all 4 tires for $86. Hopefully they did the job right and I don’t have problems down the road.

Yesterday I found a $59.99 coupon for a wheel alignment at a nearby Nissan dealership. They’re a few miles out of the way but I’d brought my car there before, without any problems. I casually mention to the service advisor I have a $15 off coupon from one of their competitors for synthetic oil, but am still 400 miles from really needing a change. She then says they have a promo for $9.99 for Mobil 1 0W20 synthetic oil with a new filter. That’s like $30-35 cheaper than what I’m used to paying. About ~80 total. Helps to shop around.

For the tirerack purchase I get 5% back since I used PayPal. So $31.37 back, then 3% cashback on the subtotal or $17.46. $664.57 total for the tires. Saved a couple hundred bucks…

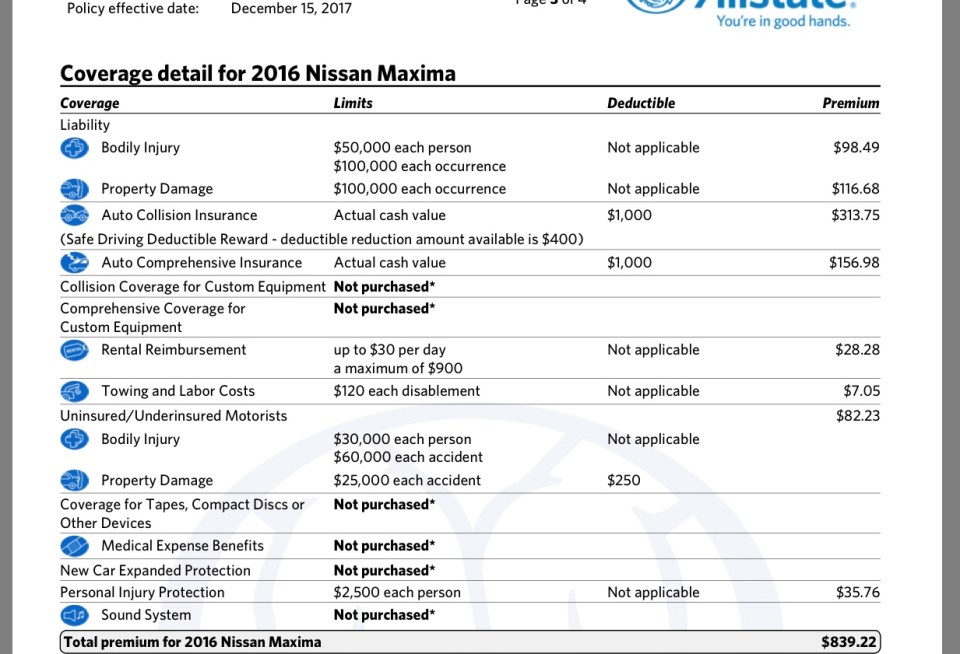

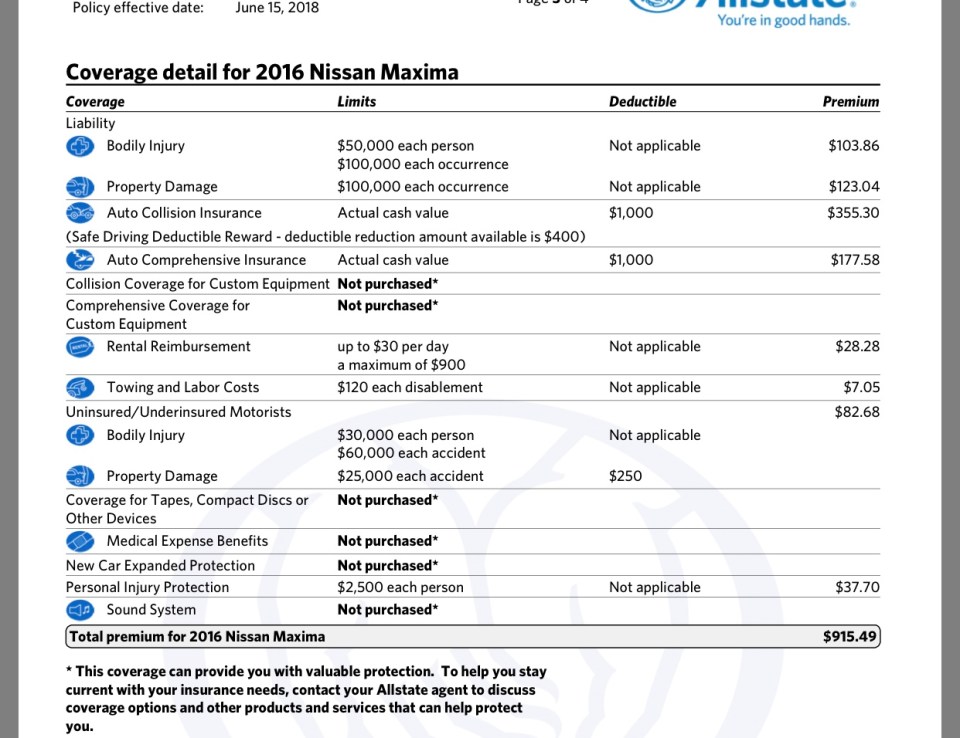

Next is insurance, Allstate’s rates are getting out of control. I’m 34, have a FICO score above 800, no accidents, no tickets. They give a slight discount for up front payment. I have priced out policies elsewhere and the price is closer to $600 for 6 months for better coverage. Potentially saving $500/yr in the process. That’s almost an extra car payment, or 10 tanks full of gas. Calling a local insurance agent who can shop around rates this week. The line must be drawn here. Progressive may be in my future. Sup Flo? haha