Gonna take some time out and give a shot out to the people who have inspired me on this journey.

- Joe at No More Harvard Debt. Joe is close to my own age, also has an MBA and got sick and tired of being stuck in debt. He started in August 2011 and finished in 7 months.

- Pete at Mr. Money Mustache – He showed that retirement is attainable by the age of 30. He lived below his means and put more of his income into retirement / investments than really anyone else. The idea that I could have enough to retire by my early 40s is appealing to me. Plus his forum and following keep the motivation going.

- Patrick Combs – He inspired me to reach for more out of life and not lest the past dictate my future. His Good Think blog motivated me to go to college. The story Man 1 Bank 0 also was appealing as someone who used to work in the banking industry.

- Early Retirement Forums – A little intimidating at times since everyone’s income seems to be more than double mine… but some of the stories people have posted are inspiring. Not to mention feedback on how I’m doing.

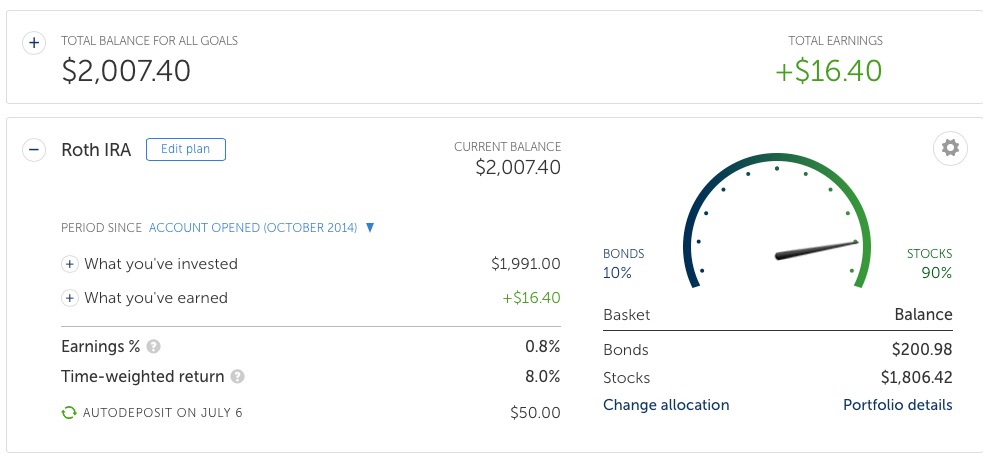

- Listen Money Matters – Originally two guys from my neck of the woods (northeast NY) who have a no nonsense approach to money and investing. They inspired me to get a Betterment account and do steady contributions into my Roth IRA. After 2009 I got spooked and thought never again.

- Dave Ramsey – As a gay man who is not in alignment with any one religion, the idea of listening to advice given by an Evangelical Christian seems unlikely. Agree or disagree with him, Dave has a track record that works. I cut back my consumption since it’s repetitive. Sometimes people with a big mountain to climb need the repetition though.

- Suze Orman – Love her, hate her. She’s become famous by telling people to clean their act up.

- Rick Edelman – Ric Edelman offers a unique perspective as a financial advisor. His firm has billions of assets under management. Unlike many of the other experts he has a keen eye on exponential technology and the latest developments in the industry.

- Ramit Sethi of I Will Teach You to Be Rich – I have automated my finances and am amazed at the successes of people taking his courses. I haven’t grown a pair of balls yet in that area, but I still have a vision of what’s possible.

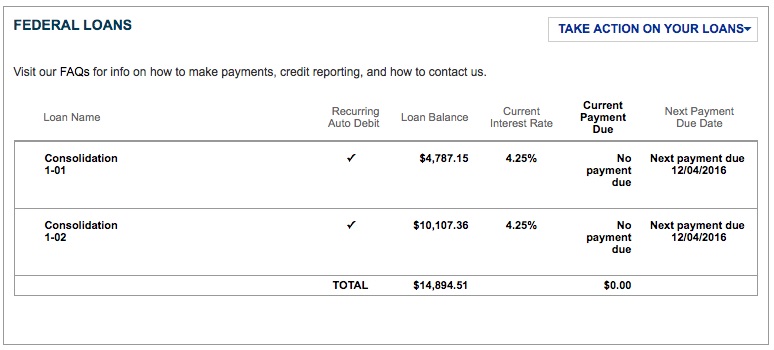

- Me – I’ve made a lot of progress and will continue to make a lot. I’m very anxious to have the student loan debt gone. This month I almost refinanced my student loan through Earnest. Despite a $200 lower minimum monthly payment, the .43% higher interest rate, negative effect of taking a new loan out on my credit and extended my payments longer than the end of 2016 were not.