On Monday I found out that I had incredibly high blood pressure. 140/92 then she took it again, 140/96, when I got home it was 145/104. The day before I had some drinks, a redbull, and some salty food at a local restaurant. Also more stressed than normal with work, my personal life has been going fine. I do need to make better choices when I’m out with my friends. Just because their bodies are fine with certain activities, doesn’t mean I won’t quickly start to feel the pain.

The doctor put me on a diuretic which I started taking for the first time today. Miraculously my numbers dropped to 128/78 which never would happen otherwise. Still looking look at diet and lifestyle choices more. Sodium is in everything I eat out but I can make a specific choice not to overdo it. I’m adjusting to not just eating what I have a craving for all the time, it’s rough. 😛

I’ve been trying to not look at the market as often as I used to but it’s hard. I made some recent changes due to my upcoming car purchase. Basically for my M1 account I stopped adding $400/mo and my 401k contributions have dropped to the maximum amount for the match. YTD between my 401k contributions and employer match I’m at $17,677 and $4,500 in the Roth. I almost cashed out my M1 account but literally hit the stop botton 15 minutes before the sell order would’ve kicked in.

10/5/2022

9/3/2022

Difference

% Change

401k

147,597

150,337

(2,470)

-1.8%

Roth IRA

21,115

21,516

(401)

-1.9%

M1 Account

6,120

6,388

(268)

-4.2%

EF+House

1,952

2,728

(776)

-28.4

HSA

3,019

2,982

(+37

+1.2%

Total

179,803

183,951

(4,147)

-2.3%

Credit Cards

(2,229)

2,312

(83)

-3.6%

Net Total

177,574

181,639

(4.064)

-2.2%

October 2022 Net Worth Update

So my current plan is to stack up cash and use it for the down payment on my replacement car, a 2023 Acura Integra w/Tech Package. I wanted something a bit more youthful than my mostly trusty 2016 Maxima and the BMW i4 would be almost $20k more with tax credits no longer applicable. There is a $1k refundable deposit that will go on my card presumably once the vehicle is in transit via rail. That hasn’t yet hit. The total OTD cost should be about $41,210.37 for 60 months at presumably $757.09 per month assuming the 3.9% interest rate holds. However I hate paying interest to anyone so I can accelerate this and probably pay the car off in 18 months. So hypothetically applying the $18,400 Carvana is offering me would drop the principal balance from $41,210.37 to $22,810. Divided by 18 that’s 1267/mo. or $600 everytime I get paid which is not too crazy. Just need to stop ordering DoorDash so much… 🙈 If I cash out my brokerage account I’d only have a principal balance of $16,810 to pay. Considering my salary those numbers really don’t look that bad.

Tentatively it looks like I’ll have until the end of October to decide how much I want to put down. That’s assuming the get their allocation as planned. Hopefully my Nissan’s value stays up long enough, the used market is quickly starting to drop.

My net worth is still down to a year ago where I was around $185k. Still doesn’t look like I’m breaking $200k anytime soon. I can dollar cost average but not sweating splurging for a bit on things outside of investments while the market has been in a freefall. As much as I want to retire early, I also want to start enjoying life now more. I feel guilty spending money sometimes after years and years of being in debt, but it’s about balance. Also if I’m not healthy the money means zilch.

The Non-Mustachian sporty-ish luxury-ish hatchback

Today I paid my rent a month early for peace of mind. I feel incredibly lucky to be able to do that, lots of people have high rents or just simply don’t have that luxury. I find out next week if I’m getting a raise or a bonus. Crossing my fingers for both. It’s been an intense year.

September 1, 2022. Only 4 months left until the start of a new year. Last week I visited family for the first time since 2018. I don’t want to wait that long before seeing family and friends again. I start to notice how old people are getting and it is a wakeup call. My stepdad is 70, a cancer survivor, one of my uncles is 78 and his wife, my aunt passed away in 2021 at 72. I did get the pleasure of seeing one of my closest friends in New York get married out on eastern Long Island. I’m happy for them both and wish them many years of happiness together. I also know about the financial part and that makes me a bit uneasy. Sometimes though you can only wait so long for certain events to happen in life. Maybe the ideal time to get married or have a kid won’t happen. You just have to roll with it and hope for the best.

It was also a realization that I need to start taking trips more often. Seeing the lovely Sunken Meadow Beach in the summer is a whole vibe. Hearing the waves of the ocean and seagulls squawking, smelling burgers and seafood on the shore. Feeling the laid back vibe in general in a world of hustle and bustle. I just hate the bills at the end. Some friends want me to go to Disney but that’s easily a $1500 trip between the flight, airbnb rental, tickets to the park, food and beverages. Another group of friends wants to go to New Orleans but I don’t think I want to share a room for multiple days or get shitfaced drunk / eat crap. Guess that’s the difference between being turning 30 and 39 with high blood pressure and obesity…

I did rent a nice midsized SUV a GMC Terrain. It had a lot of power and shifted so smoothly. Loved the Apple CarPlay feature and used it on every ride. The start/stop tech was pretty cool. The fuel economy was still better than my car. My parents gave me $200 to use toward the rental which iirc was $413 for Wednesday through Saturday. Kinda pricey if you ask me but it served its purpose. Can’t do an Uber for an hour drive and another hour back. That would cost about half the price.

The markets haven’t been doing the best lately, there have been more and more talks about recession. Of particular concern is the current situation with real estate both in the states and in China, along with inflation, commodity prices, etc. There are lots of items outside my control. I’m still following the path of dollar cost averaging. Not looking at my portfolio multiple times a day comes a bit harder. I still wonder if at age 50 I’m going to say yeah I’m really glad I stayed the course at 39 or will I wish I had a more diversified investing strategy. I could switch to more dividend producing investments but those don’t necessarily have the projected or historical growth. I can buy REITs and get some of the benefits of real estate but if the sector is declining why should I buy it now? Would be better to wait. Some of the big name financial people on YouTube make Real Estate sound like the greatest thing since sliced bread. I’m not so sure.

Ok let’s talk numbers now. My 401k balance dropped 3.2%, Roth is down 2.6%, M1 account is up 2.8%, Emergency Fund is up 9%, HSA is up 3.6%. Overall I’m down about $5k which sucks, but it’s also a buying opportunity to buy when things are down. Total net worth is down $6k or 3.2%. I have a credit card balance I’m reporting out on since I’m now carrying a balance on the non 0% card ($1,199.25 balance on Apple Card). Projecting to have my card balance all paid off by the end of the month. 8/28/2021 a year ago my total investment portfolio was at $176,696.

September 2022 Net Worth Update

GMC Terrain rentalSome pics from my vacationMy Jos. A Bank suit for $161 including $24 expedited shipping

Some of the work issues I was concerned about a while back got better but still not sure if I’m getting a bonus. I still want a job that pays $120k+ / year that would help me hit some life goals a lot quicker. So the basic question is how do I do this in the next year since getting promoted again where I’m at is highly unlikely. Also what am I willing to sacrifice for this since everything has tradeoffs.

I bought some lottery tickets the other week and got $58 back. Kinda funny since I was at 7/11 around midnight thinking I’d only get $5 for getting that megaball number. That and a scratchoff I got $5 back on. It’s entertainment… 😀 Lastly I wasn’t impacted at all by the flooding last week thankfully nor did I get stuck dealing with flight delays like some of my friends were. Happy Labor Day Weekend. May you find something both fun and relaxing to do! ❤

I really wanted to believe. I put my car preorder in for the BMW i4 on 7/27 but some major changes have occurred in the weeks since.

Both the Senate and House of Representatives have passed a law that will have some significant changed on the IRS EV tax credit. (1) after December 31, 2021, and before the dateof enactment of this Act, purchased, or entered intoa written binding contract to purchase, a new qualified plug-in electric drive motor vehicle (as defined insection 30D(d)(1) of the Internal Revenue Code of1986, as in effect on the day before the date of enactment of this Act

Tomorrow 8/15 President Biden is expected to sign the bill

Dealership I’ve been working with will not be able to provide a contract on a vehicle that doesn’t have a VIN.

There are literally 0 i4s available on a lot for purchase within 300 miles.

The Texas EV rebate program hit the 2022 cap on applications being processed, so would have to wait until 2023.

The different is significance this would be the difference between a $60k purchase and a $50k one. $10k of “free” money that I would’ve been able to apply or receive back at some predetermined future date. So to coin and expression from Shark Tank. For that reason I’m out. So I’m going to keep on doing what has allowed me to double my net worth in 2 years, and quadrupled in 3 years. Maybe one day I’ll buy a BMW, or an EV in general. Just not today.

I switched my 401k back to 19% of my income and bumped up my brokerage contributions to $100/wk or $400/mo. I’m saving $500/mo in a house downpayment fund, also $500/mo in the Roth IRA. I set the rules and don’t have to go crazy. A month from now I might adjust some of these numbers. My investments are at $195,719 today and I have an 827 credit score so I’m doing something right. 😀

Last bit of ranting aside.

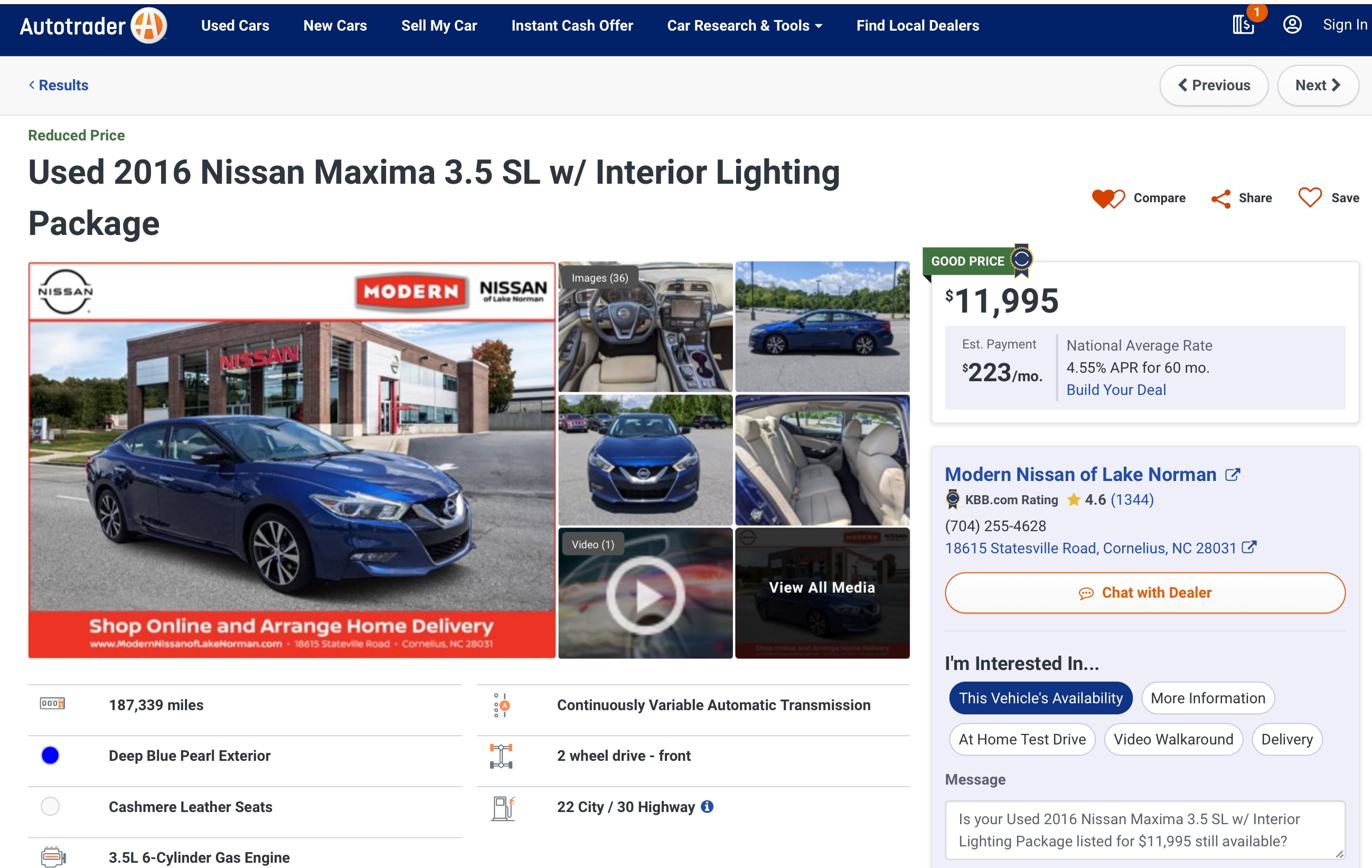

My 2016 Nissan Maxima has 72,600 miles. This one I found on Autotrader from the same year has 187,339. So maybe the old gal has a couple more years left in her?

The market has had a bit of an uptick, I’m up 9.9% for the month. Most of my investment contributions are on autopilot by design. This is promising but I still feel like there will be a drop with rumors of recession looming in the shadows. Compared to a year ago I’m up about 10.5%. Trying not to look at the numbers too much but I’m up at least. August 2020 my net worth was only $95k, that’s still almost a 2x increase. My M1 account is up 22.95% all-time right now, only 1.34% down in 1 year. Maybe I’m a better stock picker than I thought? I really like picking a couple companies I like, a few dividends, and an index fund.

Debating whether to add the money I’m setting aside for the car / home down payment here. I probably will next month because both are relevant to my overall net worth. So far my 401k lower contribution amount hasn’t kicked in yet. My higher $1134 rent payment just kicked in, from the older $955/mo amount. Still close to dirt cheap though.

The American Dream for many has become the American nightmare and nothing I do is 100% set in stone. If the tax credits completely go away for the i4 I won’t buy it. Not paying $10k more when I really don’t have to. Houses especially older ones can suck up a lot of money in repairs. A friend purchased a home last year and already she has something come up requiring $21k of repairs. My stepdad pays close to $12k per year in taxes on a house he recently paid off and says he’ll sell this year. Maybe one of these thousands of new homes being built will drop because people stop buying them. Almost time for brunch. Be well!

This is a long post. You’ve been warned. 😛 Let’s have a momentary flashback. 2012 when I started this blog I had massive debt proportional to my income. Shit, I just started my first full-time job in Marketing. My salary was in the mid $30s and my debt was over $45k. I had to count every dollar, and use everything I could to get out of debt. The numbers were too out of whack. All this debt and lack of career prospects were big motivating forces to leave New York and move to Texas. On paper it made sense even though I gave a lot of things up including being in close physical proximity to my parents and good friends at the time. I was 29 then and having a bit of a mid-life crisis. I didn’t want to be that millennial who had student loan debt for the rest of their life and racked up massive interest. Then hope the federal government bailed me out. My father was disabled and lived off an SSI check every month and a couple extra bucks from babysitting. God willing I would use the power of my mind and physical abilities to support myself in life and become independent.

So I did. I went from a total net worth of -$50k to over $200k. 5x higher net worth, better paying jobs and hitting the much coveted six figures. During a period of record inflation, covid deaths, monkeypox, international unrest, a very polarized America, what I consider a national crisis with gun violence in the country, a time when I wonder if my rights to marry the man of my dreams will be taken away. I got caught up in external factors and neglected myself.

How? Well the most visible was my weight, I hit the highest weight of my entire life on July 11, 2022 a massive 263.6 pounds. Then I got serious about cutting back on sugar and eating a normal amount of calories. Fucked around with Intermittent Fasting again. Now 18 days later I dropped 10 pounds and am still going at it. Before Covid times I was 240 and I know I can get back there again. In a completely supportive healthy non-obsessive way. With that weight comes high blood pressure, risk of stroke, lack of energy, sweating profusely in moderate intensity activities including the sports I play. So it’s a huge quality of life item.

Weight Comparison July 2022

What is my breakthrough moment? I went *too* far the other way though with saving and investing. Counting every dollar for every decision. Leaving myself just a couple of hundred dollars to spend on things outside of investments every 2 weeks. You can do that for a while but overall it’s not healthy in my opinion. So I’m making some changes. People might not agree with them but for me it’s what I need to do at least right now to bring more joy into my life.

I’m continuing to max out my Roth IRA each year at $6k/year and doing $300/mo to my M1 account. The M1 contributions might increase to $500/mo or more, have to see how I feel about it. My 401k contributions are dropping to 6% of my salary. $1625 a month was too high and didn’t give me enough free cash on-hand. Why do I need cash?

1. My current car has been pretty reliable with a fairly low cost of ownership. Aside from gas that is… It has 72k miles. Every 30k miles I need to do a $200+ CVT fluid change to make sure it doesn’t blow up, the shocks, and brakes are probably going to need replacement soon, new spark plugs, and normal things like oil changes. This car is also being discontinued by Nissan. 15k miles per year / 23mpg = 652 gallons of gas per year, at $4/gallon is $2,608 a year… Times 5 years that’s $13k just to fill the car up. I’ve driven Nissans for 19 years and internal combustion engine cars for 21. Nissan as a company has had multiple class action lawsuits related to the transmissions in their cars, mine squeaks and rattles when it gets cold. The service experiences I’ve had are kind of disappointing including one where I spent the better part of half a day trying to get a new tire and having the service person put in the wrong address for my Lyft ride back to the station. Used car prices are going to start dropping and a car with over 100k on the odometer I also expect to drop even more.

Last month I did try to buy an Acura Integra, but… While much better on gas, it’s still going to need to burn it. Then the power is only 200hp and it has a CVT with a turbo on top of that. 14 years of CVT transmissions I didn’t want to buy a car with one of those ever again if I can avoid it. Plus the backseat room isn’t so great and many dealers are adding thousands to the price due to market conditions. So scratch that option…. Looking at some EVs – The Tesla model 3 interior is too spartan for me, basically no buttons and you need to turn your head to the side to see your speed, and still build quality issues. It also doesn’t qualify for the current federal tax credit. Polestar is almost impossible to find, Rivian / Lucid too expensive. After an acquaintance died after a Kia / Hyundai fire I refuse to buy one even their EVs. Chevy Volts are tiny, catch on fire, and GM/Ford build quality… Mercedes EQS is too expensive. Toyota bZ4X can’t be preordered and they stopped production for August.. Hybrids like Honda Accord Hybrid are an option but more mechanically complicated and much less horsepower, torque, and fun one by comparison.

I placed an order on is the low end BMW i4 eDrive 40. The car is selling at MSRP (no markup) and there is a 10-12 month wait time. So that’s June-August 2023. The selling price is $59,570, out the door price is $64,821. It’s not cheap. From that $64,821, take $7,500 off for the federal tax credit and another $2,500 for a Texas state rebate. So now we’re down to $54,821. My trade could get $17k in a year I estimate so that’s effectively $38k being financed. Then roughly $10k in gas savings over 5 years. Those savings won’t all happen at once though. I’m trying to cashflow as much as I can starting now to not have an $800/mo payment. An extra $10k would drop that to $630/mo, $20k would be $463/mo. The tax credit / rebates would essentially knock off another $166/mo. While not super unreasonable, it’s still debt and I’d rather keep that payment as low as possible. Thinking I save $10-$15k for the down payment depending on when the car becomes available. I’ve wanted to buy an electric car since 2014 but the options just haven’t been great to me. BMW has been manufacturing them in a limited / testing capacity since 1972 and the first electic cars were in-use in America in 1897. Big oil won the battle and the electric vehicles disappeared by 1920. In 2006 the documentary Who Killed The Electric Car came out.

Stolen off Reddit, same color BMW i4 eDrive 40, a $60k toy that uses 0 gas

What about charging?

Option 1 – Most expensive – there is literally an app for that called Currently EV Charging (https://apps.apple.com/us/app/currently-ev-charging/id1624940687?see-all=reviews) that works on a monthly subscription model. They charge by the kWh. The i4 has an 84 kWh battery, so that’s 67 to get it to 80%. So let’s use the Commuter option at $15/mo / $0.58 per kWh and we schedule a fill up 3 times a week. That’s $40 + $3.75 for the most expensive option. They say they’ll deliver up to 100 miles per delivery.

Option 2 – There are more and more places to charge up. EVgo near me is $0.20/minute, charges at 50 kW. That would be 1.34 hours a week to hit 80% from absolutely 0%, 60 x $0.20 + 4.95 = $21.03

Option 3 – Another charger at 7/11 charges at 90 kWh, so that is 45 minutes. $0.55 per kWh or $37.

Option 4 – Tesla is going to open up their supercharger network at the point in the future. The assumption is they’ll start charging more than for their own vehicles. This likely will start happening before my delivery date.

Option 5 – A permit was applied for a nearby shopping area for charging (presumably free) to happen in May 2023.

Option 6 – A bunch of free / slow as shit chargers at 6 kWh throughout the area.

Option 7 – A Chevy dealer will be opening 8 high speed chargers that will operate at 120 kWh and do a full charge in 35-45 minutes. From what I’ve read at $0.14 per hour that’s $3 for a full charge.

Option 8 – It comes with 2 years of free charging through electrify america. The nearest one to me is in Fort Worth and kinda far but there is a possibility more will be built closer to me in the next 12 months.

*Option 9 – Charge at home when I eventually buy one. This option is at least 2 years out and would be the most cost effective option. Particularly if it is semi powered with solar energy.

2. I’m going to start saving for a home. I know I’ve been talking about it for years now but I’ve reached the breaking point. The housing market is slowly correcting. I can probably get some type of downpayment assistance but not sure if I will need it. In my mind I’m still thinking 10% on a $200-250k property whether it be a townhouse or a condo. That’s roughly $20-25k by summer of 2024. Given my income I think this is doable. I don’t want to be in my 40s renting unless I’m getting some killer investment returns. The last year that hasn’t happened haha. Renting elsewhere is an option but $1700/mo and no equity would be a real bummer. At some point I’d probably inherit my parent’s / childhood home but I’m not banking on that and hopefully that’s not for a couple decades from now. The goal would be to have the house paid for completely (or at least have the money set aside to do it) by the time I’m 50.

So here’s to making some changes that I think will bring a little more excitement to my life. I’m still going to be investing. Just cutting myself some more slack for a bit.

100° day and I’m outside hugging a tree during a walk

Last but not least I’m turning 39 in just over a week on Monday. A lot of my more formidable years are behind me. The struggles of being an in the closet teen, dealing with loss, coming of age and completion of 3 college degrees in my 20s, enlightenment / slowing down / self-awareness of my 30s. I still like to think I have a lot of life ahead of me in my 40s and beyond. I’ve also seen a lot of the reverse. Stay happy, healthy, and much love. Time for bed…

Happy 4th of July! There are times I forget I have a personal finance blog. It’s been about 10 years since I started on here. With all the turbulence in the market sometimes ignorance has been bliss. I used to obsess over money, but no more. Enjoying life and finding balance in recent years has been the goal. I can’t save every $ I earn and invest it and I’m perfectly fine with that.

So that’s where my recent purchase comes into play. The 27″ Apple Studio Display. I have a 27″ monitor I use for work that works perfectly fine, a 2020 purchase. However earlier this year Apple debuted this monitor that is arguably the best build quality in the industry and one of few options. It’s 5K, not 4k and the text / graphics / video are all crystal clear. It’s got some amazing bass, 6 speakers with support for Dolby Atmos, an aluminum enclosure, 3 USB-C ports on the back. MacOS does some weird things with 4K up to 5K resolution and scaling back to 4K. You have to experience it in person, pictures don’t do it justice. With my Apple Card, I do 12 monthly payments of 0% APR or $133.25/mo and $131.92 in tax. I could pay it off in full but don’t see a reason to. Zero percent is still zero.

Apple Studio 27″ Display

So back in 2016 I bought my car for about $5k off MSRP. At the time it was a decent deal. The car is still purring along over 6 years and 71k miles later. I have a warranty on it until 2024 or 120k miles. However it’s starting to show its age, creaks and rattles in the cold, little rock chips and dings in the paint, some technology limitations like no Apple CarPlay, no LED lights, smart cruise control, or lane keeping assistance. The fuel economy is alright at 24mpg but 34 or more would be amazing especially at $5 per gallon (my car in 2015 was only averaging 29). Carvana offer is about $20k, a local Acura dealership only offered $15k and they likely wouldn’t have the car in stock until August if not later. So I politely walked out with my title, and second set of keys in hand. On top of that the offer on the car is MSRP, not even $500 less. If the economy goes south, incentives on cars will come back. I still am casually looking at other cars but the reality of the market is quite apparent.

Acura Integra offer

Some events have happened recently that left me with a bad taste in my mouth. Without going into details, it was a wake-up call to become more proactive. Doesn’t matter how much effort you put in, sometimes you still get treated like crap. Loyalty is kind of dead, have to look out for yourself. Never trust what a 3rd party entity tells you especially if you keep getting stringed along. So balancing feelings about that and not worrying about things beyond my control.

So yeah, I’m down $10,616 or 5.8% in a month, that happened. Even worse when you consider all the contributions I’m making to my investments. On 6/30/21 my net worth was $159k! I still have a lot of time left until retirement but it’s not a good feeling. I keep dollar cost averaging with the expectation the market will rebound. For me to hit that $200k goal I had my portfolio would have to increase by 16%.

Recently I went to a friend’s pool party in a much newer development than mine. It was glorious, the refrigerator, countertops, floors, lighting, pool, on-site workout facilities. I was just in awe of how beautiful it all looked compared to my no frills arrangement in North Dallas. 1983 vs 2012 design.

One of my close friends is trying to convince me Texas has turned into Gilead and I should move elsewhere closer to my family. I have mixed thoughts on that. On one hand the political climate of the country is becoming less and less welcoming to certain groups of people. There are very early talks about reversing supreme court decisions regarding matters related to gay rights and marriage equality. When I hear politicians from Texas and Florida talk, it seems like they want to take things back to 1970. Today I heard a bit of a “surmon” from a Fort Worth preacher in early June who is promoting violence. This is someone who is supposed to be preaching god’s teachings. Moving could also be incredibly stressful with no support system. New York would be the best option for me there but then my cost of living goes up Salary.com showed a 69% cost of living increase, and a 15.3% salary change increase. Really not worth it. Plus two of the nicer complexes I checked out near my hometown start at $3200/mo, the other was about $3900. This is the surburbs, not even NYC.

One of my friends put it best, he’s going to just keep dollar cost averaging and stop checking his portfolio daily. I should probably do the same but I’m a numbers guy. Can’t let the market and overall economy get to you. Just keep going strong and remember this all goes in cycles. Cheers!

June is a mere two days away. In terms of finances, I had an unexpected vet visit after taking my dog to a friend’s house. Sparing unnecessary details she had a stomach issue and needed some medication to help address it. Her eye inflammation thing also came back so they had to do a test for that. $243 later. It’s like if I don’t constantly watch what she’s eating she will eat whatever she possibly can…

In terms of quality of life… My current approach is to behave like I’m taking myself out on a date. Even though I am very much single. I would see acquaintances of mine go on trips together, or even have parties without me or even mentioning an invite. If that’s how it’s going to be, why wait for them at all. Do my own shit with people I like spending time with, or do it alone.

I was in a bit of a dark place earlier in the month. The shooting at a supermarket in Buffalo, NY. Then the tragedy in Uvalde TX at an elementary school. One of my friends is from the area and he’s wanting to do some type of charity for the victim’s families. More recently there was a shooting 3 miles from me at an apartment complex where 2 people were dead and one injured. Late last year the 23 yo son of a lady I worked with was hanging with the wrong crowd and someone shot at the group through the garage and he was shot and killed.

The gun violence in America is out of control, the leaders in states like Texas are making it easier to get guns. I think our governor was supposed to be show up for an NRA meeting just a few days after.. On top of that, If you’re a minority, you’re at a much higher risk of being pulled over and shot by a police officer or being subjected to other types of police brutality. Then I thought about the church shootings, and Pulse nightclub… It’s so easy to go down that rabbit hole. I honestly had to take a break from the news, it’s so damn depressing. It triggered anger, anxiety, helplessness, and PTSD all at once. I couldn’t focus on my daily routine. I’m doing better now, but it wasn’t easy to try and pivot.

One group I played on a sports team with this season. The last 3 games we had to forfeit due to a lack of players. When we did play morale was low because we never won any games, no one would show up for practice. Then I’d see the captain and a few players get together to play a different sport just a few days later (after a supposed injury) and talk about how amazing it was. Kinda rubbed me the wrong way. Plus a few other things I’ll leave out on here. Moral of the story is sometimes it’s better to coordinate with strangers vs people you know who are sketchy.

Beside that, last week Monday was 18 years since my father passed away, later in the week was my mom’s birthday, and mom / stepdad’s 17 year anniversary was just a few days later. I haven’t been back home since 2018 and still feel bad about that, especially when I see people who see their family every weekend or once a month. New York is such an expensive state to live in, I don’t think I could easily make the numbers work and aggressively contribute to retirement even on my current salary.

I also found out that my boss is leaving whom I’ve worked with on and off going back to 2013. Kind of not sure what the future holds. I’m in good standing with my other boss and overall, just a big adjustment in management styles. They’re looking to backfill his position but who knows how long that will take…

Aside from that let’s talk about what’s currently going on with finances. The market has been all over the place.

5/30/22

4/30/22

Difference

% Change

401K

$152,176

$149,369

$2,807

+1.9%

Roth IRA

$20,856

$20,231

$625

+3.1%

M1 Acct

$5,239

$5,070

$170

+3.3%

Crypto

$0

$1,236

-$1,236

-100%

Buffer Fund

$2,050

$1,250

$800

+64%

HSA

$2,292

$1,932

$360

+18.6%

Total

$182,613

$179,087

$3,526

+2%

June 2022 Net Worth Update

I completely sold all of my crypto. I thought I would be a HODLer but didn’t feel lke losing the last $900 in my portfolio. I think I lost close to 60% of what I invested, a couple of days before LUNA crashed (I didn’t own any). Everything I held just kept dropping and dropping, and dropping some more. It was an experiment, there was a time when I planned to invest significantly more but didn’t have the appetite for it. In hindsight that was a smart decision. I’ll get a tax benefit come year end as a capital loss. The above gain is a little bit deceiving since I have been contributing close to $2,600/mo in my investments including matching. Compared to June 2021 I was at $151k, so still up roughly 21% up

My HSA finally hit the $2k mark meaning everything above is also now going into and S&P 500 index fund. It’s a milestone I’m hitting for the first time ever so that’s a good thing. It doesn’t seem like that long ago where I didn’t even have enough extra money to put into an HSA.

This memorial day I went on a little retreat to a park in Little Elm. Nice break from sitting in the apartment staring at screens all day. I didn’t get in the water but I walked on the boardwalk and through the nature trail. Even when there are some bad times, it’s important to resync, be present and focus on ourselves / a few close people. The weight of the world’s problems shouldn’t fall on me.

Beach Pic 1. It’s a water bottle backpack, not a harnessBeach Pic 2Beach Pic 3Billiards Balls – My OCD side wanted all the numbers to be face up but oh well 😛

Thinking about splurging on a few things. Yesterday I dropped about $220 on clothes and a pair of shoes at Nordstrom Rack. The shoes they replaced I bought in 2019 and threw out because the foam was coming out of the heel. Thinking about getting the fancy 5k Apple Studio Display, there’s nothing equivalent on the market but it’s also missing some features I want. Also these gas prices have me thinking about something more fuel efficient. 23mpg with 4.70/gallon premium.. 10k miles a year, that’s a little over $2k for just gas. In 5 years assuming prices are the same that’s $10k assuming gas prices don’t go up even higher. By then the car will be 11 years old and resale will be pretty low compared to the $20k I can get today. Decisions….

I’m thankful for what I do have even if it’s not quite the way I want it to be yet. I’ll be working again in less than 9 hours. I aim to be an efficient problem solver, it can be hit or miss. Ok that’s where I’m at now. Sometimes it feels like no progress when I look at just the numbers but I’m buying ownership of companies at a discount.

Trying to avoid the 40-life crisis, but I’m reading stories of people in their 40s / 50s and thinking yeah I’m going to try to do better. I’m going to have some money in retirement, I’m not going to rack up unnecessary debt, I’m not going to wait until I’m old to enjoy travelling. I’m going to find love. I’m not going to neglect my health or let regrets and fear hold me back. I’m not going to buy a mcmansion and buy things to impress people I don’t even talk to. These are just thoughts.. Ok bed time.

Back in the olden days when Debt Free Alpha was just a young lad, I worked at two supermarkets. The first was in 1999 at this store called Met Foodmarkets. I would ride my Raleigh M-20 mountain bike about about a mile to work and park my bike in the back of the store. I made a whopping $5.15 per hour, no benefits, and worked the registers. I learned a lot from that experience about how not to be an effective boss and how I was yearning for more in life.

Fast forward to 2001 I worked at a different supermarket, which I quit once then got rehired after a few weeks of my rapidly dwindling savings. During my employment there I met a friendly, but insecure young lady by the name of Stacey. She rode her bike to work, worked in the Bakery, and was afraid to learn how to drive. We became friends and over the years I’ve seen her blossom into a confident, passionate person.

I still can’t believe she’s rocking the 2010 MacBook Pro. I remember when she was shopping around for different laptops and couldn’t decide which one to get. Stacey if you’re reading this, it’s 2022. The 2021 Apple Silicon MacBook Pros are pretty dang amazing. 😉

A common theme of this particular episode is getting out of your comfort zone and not selling yourself short. Looking back over the course of my life and career making those changes are what allowed me to grow and hit salary and investment goals I didn’t think would be attainable before the time I hit 40.

Lastly I’m trying to avoid burnout and it’s close to midnight but I hope you are all doing well. The last two days have pulled at my emotions but I’m staying focused on what I as an individual do have the power to control. Deep breaths, meditation, one step at a time. Tomorrow I have meetings for the entire day from 8:30-5:30, then meeting friends after that. wish me luck.

I consider myself middle class though based on this 2020 tool by the Pew Research Center I am within the Upper income tier along with 21% of others in the area.

Income Tiers for DFW

I don’t feel like I’m Upper Class, more like middle class. As a single person I don’t own a home, travel very frugally when I do, don’t spend too extravagantly. Then inflation, inflation, inflation. Speaking of, my rent is expected to go up $180/mo from $955/mo to $1,135. That’s an 18.8% increase from where I was

What are the pros living here? It’s relatively quiet, my neighbors stay out of my business, neither the dog or I have to walk up a long flight of stairs, parking is decent and they don’t tow cars if someone stays here for a few hours / days. It’s still cheap relative to both my income and in terms of what other people pay. One of my friends in Frisco has a Ring camera and has had packages stolen or knocked around, drunk young guys ring his bell at all hours of the night. I haven’t had to experience any of that.

The Cons? I’ve been here since Dec 2014, the complex was built the year I was born, the inside is a bit lacking of frills, the stove is pretty old, there isn’t a bunch of natural lighting, I have only one friend who lives within a 5 mile radius and that’s someone I used to date so we don’t really hangout. For any company I do have over, the place isn’t that impressive. The fixtures, the flooring, the paint on the walls. The worst is the bathroom, the glaze is flaking off the tub, the ceiling has spots of mildew that just gets painted over. Since the flood last year, pieces of tile either have glue that doesn’t adhere to floor, or the grout between the tiles has a slight water damaged look upon close inspection. My neighbors were smoking in their unit for a while and the smell would come under the door into mine almost daily. I had to complain multiple times about it. They’ve since stopped but I smell whatever meat they cook in my unit too and it is not a very appealing aroma. Nothing is walkable apart from a little convenience store, barbershop, and taqueria that opened up. Desirability to me of these places is fairly low.

I haven’t signed the renewal paperwork yet but I am starting to look at other alternatives that would be at $1200/mo or a bit above that.

Option 1 – MacArthur Ridge Apartments – $1294/mo – $200 Pet fee, $20/mo pet rent, $75 application fee, $75 admin fee. Built in 1991 so not that much newer. 4 stories. Read reviews about the lower levels being moldy. 2 years ago someone wrote about them increasing rent by 18% more from year 1 to year 2. People complain about the walls being thin, parking situation is not good.

Option 2 – Summerbend – $1,311 /mo – $250 pet fee, $20/mo pet rent All 6 reviews on page 1 of apartments.com basically said it was the worst place they lived and to stay away. People said there were issues with the foundation, cracks in the floors, roaches. Sounds like a shitshow.

Option 3 – Hyde Park at Valley Ranch – $1,340/mo for a renovated unit a comparable size to where I’m at now. $150 pet deposit, $150/mo pet fee. Read reviews about water being turned off. Bad parking, poor management, people talk about having to wait month to get the a/c fixed. Even worse than the other ones. It was built in 1986. Sounds like a hard pass.

Option 4 – Avalon 8801 – $1,404 / mo – The inside looks great, it would be about 50 sq/ft more than what I am in now. The floors are a wood laminate which also would be an upgrade. However the pricing increase is pretty high at 47% more than what I pay today or 23% after the increase. 2 months ago someone posted that the place was infested with German roaches. I saw 4 different pictures of roach traps that were full of roaches. No, no no. Also built in 1986. No because my quality of life sounds like it would go down and not up.

Option 5 – Villas at Beaver Creek – $1,175 / mo – Looks nice inside, relatively modern. $300/mo pet deposit. $10/mo pet rent. $80/mo to park in a garage. $30 for covered parking, $100/admin fee, $40/application fee. Built in 1993. People mentioned issues with the a/c 10 times and roaches 16 times. That doesn’t sound like an improvement at all.

Option 6 – The Lyndon – $1,401/mo. $300 one time pet fee, $100 pet deposit, $20/mo pet rent. Management is poor, maintenance seems very slow to respond to various requests tenants have had. The floors / walls are thin from what people have written. Built in 1998. Would it be an improvement? No.

Option 7 – MAA Addison Circle – $1,460/mo for something comparable to what I’m in now. $425 dog fee, $20/mo pet rent. One of my friends used to live here when it was owned by Post. Now it goes by a different name. Tenants complain about the call box not being functional, same with the elevator, slow maintenance. One said there was a 30% increase for their rent renewal. They talk about trash in the hallways and dog poop in the stairs. Also pool area being dirty.

I have 2 weeks to decide whether to stay or leave. I’ll keep looking but it all doesn’t look very promising right now. Not to mention moving would probably be about $900 depending on the location, how many boxes are needed, setting up new utilities and all that stuff. Factoring in the pet and processing fees too. I don’t know if it’s worth it especially with some of the reviews I’ve been reading.

Choosing to be happy is something I try to make a daily goal of mine. That can mean taking breaks from dating apps, going out for a walk in nature, taking pictures, karaoking it up, binging on some Netflix, cudding with my dog on the couch, and viewing content from some of favorite YouTubers. It also can be coming to terms with the past, journaling how I feel about different situations and then getting it off of my mind. Or repeating the serenity prayer. “God, grant me the serenity to accept the things I cannot change, courage to change the things I can, and wisdom to know the difference.

There is so much going on in the world and with people who are either friends, acquaintances I care deeply about. It’s a balancing act between showing empathy, but also trying not to let their circumstances, or their trauma affect my mental health. Then being happy for once close friends who leave without saying goodbye. That’s part of life though, trying to be the best version of yourself and spending the most precious resource available (your time and energy) wisely.

4/30/2022

4/1/2022

Difference

% Change

401k

$143,369

$162,197

-$12,828

-8%

Roth IRA

$20,231

$21,773

-$1,542

-7%

M1 Acct

$5,070

$5,419

+$349

-6%

Crypto

$1,236

$1,701

+$465

-27%

Buffer Fund

$1,250

$1,626

-$376

-23%

HSA

$1,932

$1,415

+$517

+37%

Total

$179,087

$194,131

-$15,044

-8%

Is it a bummer my net worth went down 8% in a month with me still contributing a total of about $2,700/mo into my investments? Yes. Do I think this will be temporary in nature? In the grand scheme of things yes, but the rest of 2022 might be a rocky year. I did receive a $228 dividend on FSKAX on 4/8. Individual stocks in my M1 account have taken such a beating. AMZN is down 49%, MSFT is down 17%, TSMC down 24%, Google down 25%, Disney down 49%. My Vanguard index fund VTI is only down 1.29%.

My go-forward strategy is to keep on going with dollar cost averaging and not lock in my losses. I think the market is overreacting. Worst case is I lower my contributions

I got Covid a little over 2 weeks ago while on vacation of all places. My Emergency Fund declined since I had a bunch of unexpected expenses on my trip. That includes 2 nights at a Best Western, super expensive food deliveries in the Boston area (one meal for 3 people was close to $85, another for myself at the hotel was $40). Having insurance is nice since my urgent care visit didn’t have any out of pocket expenses.

As far as health is concerned I still have a bit of a residual cough that comes and goes but I’m mostly back to my old self.

The vacation was a hit otherwise and aside from getting sick it was nurturing to my soul to get away from Dallas for a bit and be close to home.

Living room of the place we rented an AirBnbTook a cooking class at the North American headquarters of a well known cutlery vendorMy friends had the room with the massive tub, I was jealousOne of my friends is a wine aficionado. I could drink wine out of a box but this was quality. 🙂