Wake up, wake up, wake up

It’s the first of the month (wake up, wake up)

So get up, get up, get up

So cash your checks and come up (get up, get up)

So yeah it’s July 1, 2025, the month of June was a jam packed one. My bf and I went to Porto, Paris, Versaille, Leeds Castle, and London all on one trip. As non world-traveled person I was a little overwhelmed with the notion but decided to plan ahead as much as possible. I call this a once in a lifetime trip. I took over 1,900 pictures, these are some of the better ones.

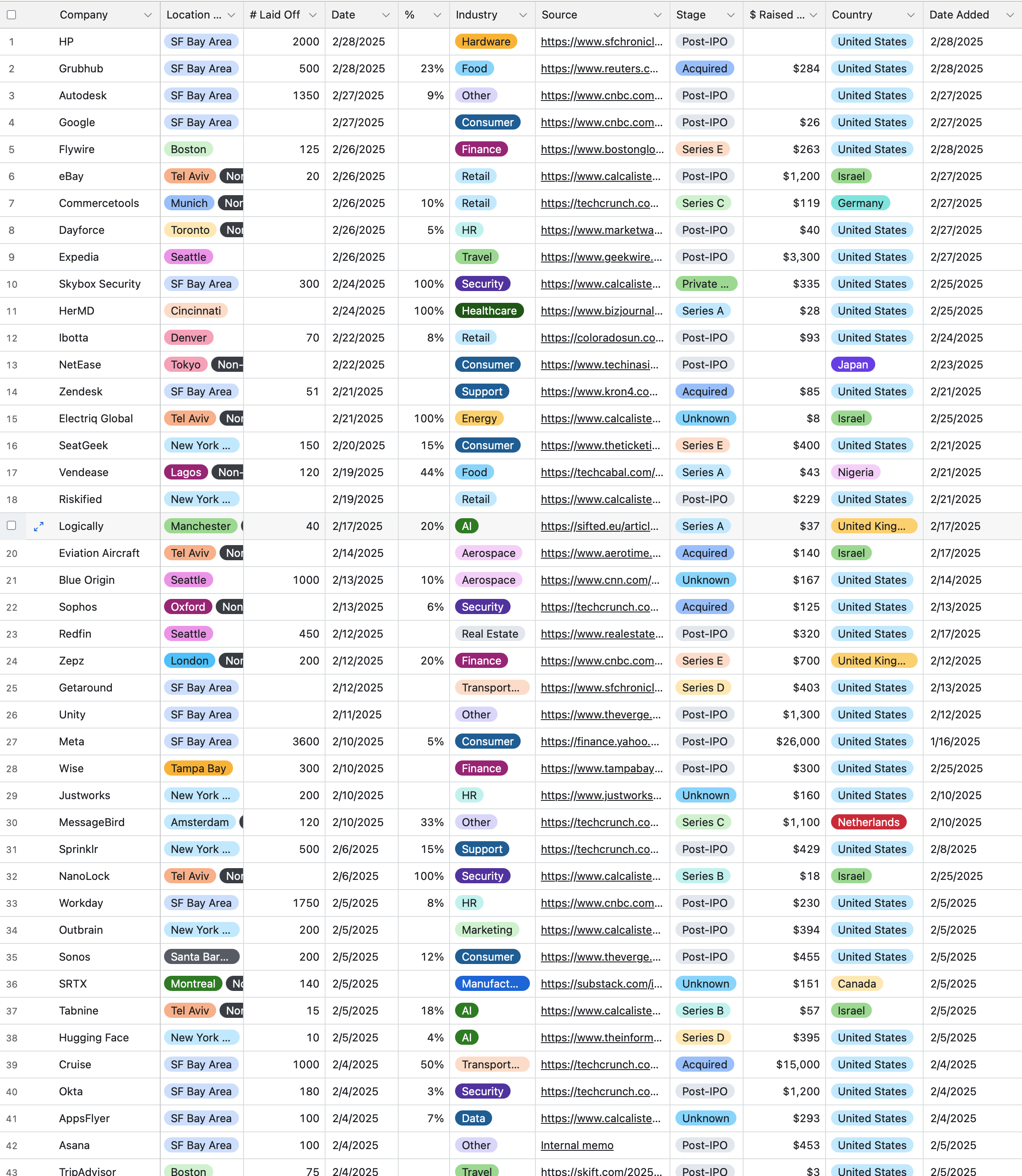

| 7/1/2025 | 5/31/2025 | Difference | % Change | 7/1/2024 | YoY Diff | % Change | |

| 401K | $ 348,738 | $ 328,591 | $ 20,147 | 6.1% | $ 273,612 | $ 75,126 | 27.5% |

| Roth IRA | $ 57,216 | $ 53,866 | $ 3,350 | 6.2% | $ 42,536 | $ 14,680 | 34.5% |

| Brokerage Accts | $ 3,710 | $ 3,278 | $ 432 | 13.2% | $ 3,079 | $ 631 | 20.5% |

| Cash | $ 23,743 | $ 26,917 | $ (3,174) | -11.8% | $ 3,222 | $ 20,521 | 636.9% |

| HSA* | $ 4,691 | $ 3,523 | $ 1,168 | 33.1% | $ 3,799 | $ 892 | 23.5% |

| Total | $ 438,098 | $ 416,174 | $ 21,923 | 5.3% | $ 326,248 | $ 111,850 | 34.3% |

| Credit Cards | $ – | $ – | $ – | #DIV/0! | $ – | $ – | #DIV/0! |

| Auto Loan | $ – | $ – | $ – | #DIV/0! | $ 8,853 | $ (8,853) | -100.0% |

| Net Total | $ 438,098 | $ 416,174 | $ 21,923 | 5.3% | $ 317,395 | $ 120,703 | 38.0% |

Onto the monthly financial updates, I am up 5.3% or $22k thanks to my savings and an uptick in the market. My HSA is asterisked because I don’t think I fully captured the balance in previous months. It’s a good amount on paper and I’m glad the number is going up. To be up $121k or 38% a year just blows my mind though. When I started this blog 13 years ago I was just trying to get to breakeven. My how times have changed. A few days ago I chagned my 401k contribution amount to get the match. No more, no less. It may slow my progress a bit but shit I have some other short term priorities.

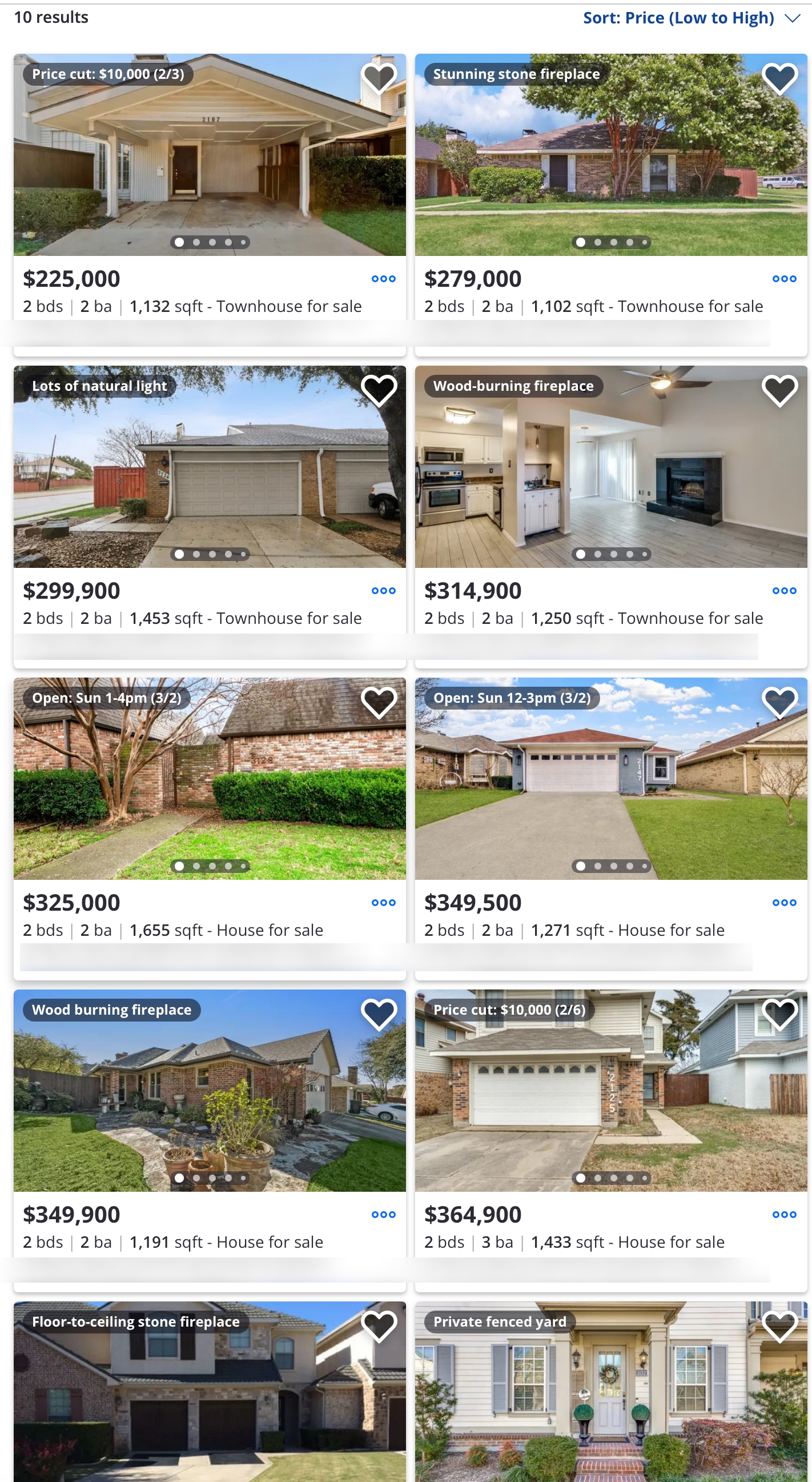

So as far as the home buying process is concerned. Let me run it down.

1 – The townhouse I liked but had reservations on due to the fact it was a townhouse with an HOA with a small driveway and over 2200 sq ft. Just too much space for 2 people if you ask me. Not to mention the expected utility costs. Also the adjacent unit was under renovation and who knows what the neighbors you share a wall will be like.

2 – The house I really really fell for. It had a pretty new roof, lots of natural light, vaulted ceilined. However the elderly man had mobility issues and was adamant about doing a leaseback where he’d rent from me until the time the property was sold. Looking back maybe that was a blessing in disguise, it was under 1300 sq ft and a 2/2 and the seller actually raised the price the same day I made my offer. Wild. Then we discovered it needed some major foundation work. Plus there were issues with improper drainage which was apparent with the mud in the backyard and there wasn’t any grass on the property just mulch. So that was a bust, lost my inspection money but got the earnest money back relatively quickly.

3 – House I currently have an offer on. Inspection was supposed to happen yesterday but wasn’t told the bathroom was going to be ripped apart prior to the inspector showing up. Oops. So it might happen today or possibly another day. This property has the foundation work already done along with renovations. Closing is supposed to happen early August. Really hoping third time is a charm. I’ve seen over 15 individual properties and driven past an additional 10 before ruling them out. No duplexes, nothing that looks like someone died or was tortured in the home, nothing with major foundation work needed. It’s a 3/2, over 1500 sq ft. a deck, privacy fence. I’m excited but also a bit cautious about the process especially managing it on one income the first year. One way or another I’ll be out of this apartment by late August.

I will need about $19k at closing, plus the cost of movers, paying the homeowners + car insurance upfront of ~$3,200 and maybe buying a new couch. So let’s say $6k between now and then. Hence why I’m temporarily pulling back on the retirement, maybe until the end of the year and ramping back up for 2026. Six month emergency fund target is $18k and it’s going to be challenging to hit with one income contributing to the mortgage.

On a positive note the bathroom remodel looks pretty nice, that just got finished today. Pardon the dirt inside, that’s leftover from the construction. Beforehand it was this cheap fiberglass stuff that was attached to the wall securely but tapping on it felt cheap and made me think ok how long is this going to last. This also will help with resale value. Also I likely won’t be doing any major home repairs in the first year or so. The big thing as long as it’s in my power to do so is not to put any expenses on credit cards that won’t be paid in full over the course of a month.

I’m supposed to get a detailed inspection report soon likely tomorrow or Saturday. Took notes of things called out by the inspector.

1. Water pressure – low, also some leaking near water main. Gave demo of bathtub and sink water running at same time, sink dropped to a trickle. Is it a major plumbing issue or something minor?

2. Insulation in attic – not fully insulated, makes A/C work harde

3. Electrical box – Safety concerns no ground rod and wiring for some of the outlets

4. Carpenter ants – frass in front bedroom window – needs to be treated.

5. Washer dryer hookup – No vent from where the dryer would physically be, currently located on other side of the building.

6. A/C 5 ton unit should be 2.5 so may be oversized for the house – inspector to lookup and verify

7. HVAC system not intaking enough air for the unit, temp drops too quickly without dehumidifying the ai

8. Roof – minor damaged from tree branch exposed fasteners

9. Leak in the master bedroom ceiling – Staining but not sure if root cause was fixed

10. Dishwasher – Kitchen – Doesn’t open fully without hitting the oven due to the narrow clearances / handle sticking out of bottom tray. Dishwasher was originally on the opposite side of the sink and moved over.

11.Garbage disposal – not functioning in the kitchen likely needs to be replaced.

12. Microwave – Have addendum for stainless steel, still see the white microwave in there as of 7/4

Foundation looks good but was told I will likely will see cracks in the walls over the next year as it settles. Inspector recommends leaving it for a year then doing the surface-level repairs. There is another home I was going back and forth on but hate the kitchen and kitchen layout though I do like the solar aspect of it. Everything has tradeoffs, I still like what I see overall. though in current state I’d give it a 6.5/10, getting fixes for some of the big items would bring that up to an 8. I don’t want the hassle of trying to address things myself plus some of the basic things will really lower the appraisal of the seller doesn’t address. I haven’t hit the buy button on furniture or appliances yet but weighing different options. I have a couple factors working in my favor but we’ll see. I still want out of this apartment. Fingers crossed on the third one being a charm. My option period ends in under a week. 😬

Anyway thanks for reading this if you’re still out there. Happy 4th of July! Pictures below taken 7/3/25 at a nearby Home Depot parking lot as I was going to buy work gloves. Peace out.