February 2026 was a month with a lot of unexpected household expenses. $1053 for a plumbing fix, $1738 for HVAC motor and capacitor replacement. That’s $2,791 in total and completely blew my budget. I’m satisfied with the quality of work done and the outcome is better than letting things just fester and get worse. That leaking pipe could have become a huge flood leading to much more expensive repair.

I got my tax refund back in record time it was aroud $913 thanks to mortgage interest. I didn’t get to enjoy a single dime of it. My net worth briefly surpassed the $500k mark but the expenses and some slight market declines made that all short lived. I think I can hit it by April though. Still up $95k in a year and almost $3k in a month

I sold my crypto and moved some money in savings to cover these home expenses. The crypto was a loss of around $191 and I’ll consider it a tax writeoff for the most part. My New HSA will allow me to invest once the balance hits $1k. I’m excited about that. The old one is in the process of being transferred to Fidelity but there may be a bit of a wait on that.

| 3/1/2026 | 1/31/2026 | Difference | % Change | 3/2/2025 | YoY Diff | % Change | |

| 401K | $406,855 | $404,137 | $2,718 | 0.7% | $ 320,732 | $ 86,123 | 26.9% |

| Roth IRA | $59,206 | $58,801 | $404 | 0.7% | $ 52,922 | $ 6,284 | 11.9% |

| Brokerage Accts | $4,852 | $4,614 | $238 | 5.2% | $ 2,321 | $ 2,532 | 109.1% |

| Cash | $11,161 | $11,723 | -$562 | -4.8% | $ 14,303 | $ (3,142) | -22.0% |

| HSA | $6,380 | $6,380 | -$1 | 0.0% | $ 3,537 | $ 2,843 | 80.4% |

| Total | $488,454 | $485,656 | $2,798 | 0.6% | $ 393,814 | $ 94,640 | 24.0% |

| Credit Cards | $0 | $0 | $0 | #DIV/0! | $ – | $ – | #DIV/0! |

| Auto Loan | $0 | $0 | $0 | #DIV/0! | $ – | $ – | #DIV/0! |

| Subtotal | $488,454 | $485,656 | $2,798 | 0.6% | $ 393,814 | $ 94,640 | 24.0% |

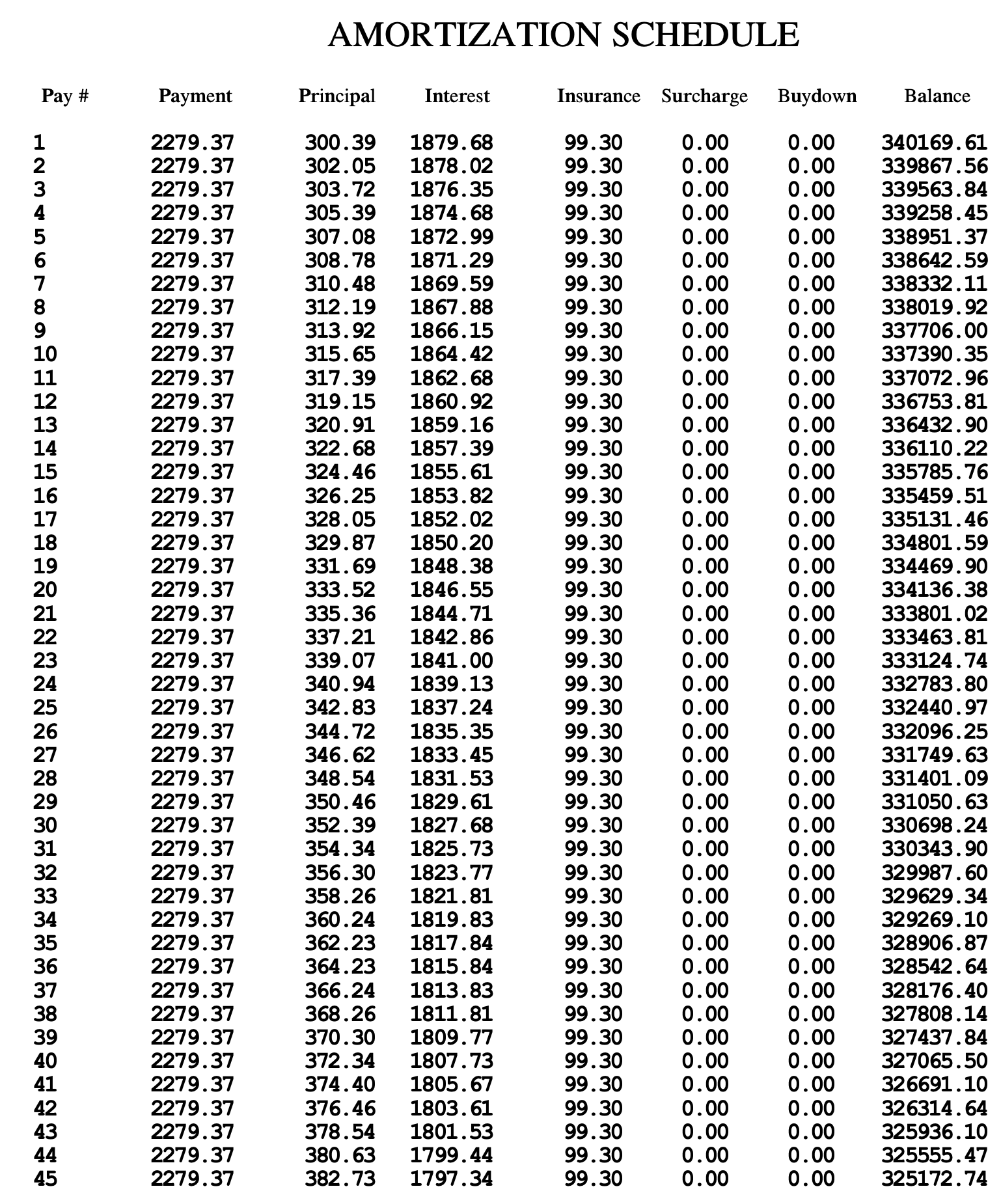

| Mortgage | $337,077 | $338,020 | -$942 | -0.3% | |||

| Zillow Estimate | $342,300 | $343,200 | -$900 | -0.3% | |||

| Equity Estimate | $5,223 | $5,180 | $42 | 0.8% | |||

| Net Total | $493,677 | $490,836 | $2,840 | 0.6% |

I’ve been back in the cycling mode since the weather here has been gorgeous.

Bf sold a nightstand for $35 on marketplace and now the room it was in looks a lot more open.

I had to complain to the city again about the water meter leaking. Full of water and one of the plumbers was on her hands and knees with a whipped cream cup scooping out multiple gallons.

I went roller skating for the first time in months. This picture was taken before I fell

We also saw a show at Medieval Times.

Seeing The Great Gatsby with friends this evening, have heard positive things.

I really have been trying to replenish my emergency fund reserves. Thankful to have a job, a partner who supports me, overall good health. Look forward to some much needed vacation time.

Did my annual air filter replacements too, though this one looked pretty decent after a year.

Air Filters are super easy to replace, just two clips by hand and you’re in.

Last but not least I lost a friend from Long Island due to a car accident in February. He was only 42. It happened right around the corner from my parents home. I was devastated for a whole week. He had joined the NYPD in 2021, loved his job and seemed really optimistic about life. RIP Mike.