A few weeks ago my bf and I took a road trip to Hobbs, NM, then Roswell, and Santa Fe. We left a day earlier than planned to make a straight run from Santa Fe to Dallas. It was one of the longest drives I’ve been on since 2004. It was nice seeing the open road and getting out of Dallas. My paid-in-full Acura TLX handled the trip like a champ. My biggest complaint was that it just sucked up a fair amount of gas at a time gas prices have been near record highs. We did that trip on a budget for sure. The flights alone round-trip would’ve been about $700/person, not to mention a car rental would be needed. Hotel we got the nice employee discount on, I think it averaged out to $50/night. We also had a spa day at 10,000 waves. A hidden gem in the mountains.

I won’t sugar coat it, I spent close to $4k on a new MacBook Pro M5 Max at 0% APR. The model I had was equipped with 36GB of memory, which ended up being a bit of a bottleneck for me and my usage habits. Plus the SSD was filling up, I’ve been using 1TB models the last 10 years but now with my games, increased media generation, etc. that was bumped up to 2TB. Also Wi-Fi 7 is noticably faster, I have 4 more CPU cores, 8 more graphics cores. In other words this thing doesn’t skip a beat performance-wise. Luckily I’m getting ~$2k for it later today which will put a big dent in my $4,417 credit card balance. It was supposed to be $90 more but apparently the LCD had a pinkish tint to it. I could’ve protested it but wasn’t trying to give them any reasons to cut the value down more.

The powerful yet expensive Space Black M5 Max MacBook Pro

I was on some medication that gave me more side effects than benefits of the medication. Decided to make a series of lifestyle changes to see if I could get a similar results and so far I’m 70% of the way there. Each day I try to do cardio, take some natural supplements, and eat a little bit healthier. It isn’t going to change entirely overnight but after 4 different medications and the risk of long term health problems I decided it just wasn’t worth it.

3/31/2026

3/1/2026

Difference

% Change

3/28/2025

YoY Diff

% Change

401K

$389,495

$406,855

-$17,360

-4.3%

$303,119

$86,377

28.5%

Roth IRA

$56,714

$59,206

-$2,491

-4.2%

$49,814

$6,900

13.9%

Brokerage Accts

$5,733

$4,852

$881

18.2%

$2,494

$3,239

129.9%

Cash

$13,443

$11,161

$2,282

20.4%

$17,209

$(3,766)

-21.9%

HSA

$6,754

$6,380

$374

5.9%

$3,415

$3,339

97.8%

Total

$472,140

$488,454

-$16,314

-3.3%

$376,050

$96,089

25.6%

Credit Cards

$4,417

$0

$4,417

#DIV/0!

$93

$4,324

4633.0%

Auto Loan

$0

$0

$0

#DIV/0!

$0

$-

#DIV/0!

Subtotal

$467,723

$488,454

-$20,731

-4.2%

$375,957

$91,766

24.4%

Mortgage

$336,130

$337,077

-$948

-0.3%

Zillow Estimate

$342,600

$342,300

$300

0.1%

Equity Estimate

$6,470

$5,223

$1,248

23.9%

Net Total

$474,193

$493,677

-$19,484

-3.9%

It is no shock that the stock market is down….and my net worth took a pretty big hit. I get paid 3 times in April so things (hopefully) look significantly different in a month. My mortgage is paid up until June 1st. I will continue to dollar cost average and put money in my 2 brokerage accounts, 401k, Roth IRA, HSA, make 2 extra principal payments on the mortgage and save what’s leftover. I try to limit my consumption of doom and gloom content. I can’t stress about what is happening 7200 miles away from me, try to control what I can, and keep my expenses in check.

Despite all of this, I’m still up $92k in the past year even though there was a 4.2% drop from my last update. I’m confident there will be an improvement later this year. It feels like a number in a spreadsheet, not real tangible assets. I hit $500k for a day or 2 then a rapid drop. This is a time when riches are formed. 2020 March during the peak of covid had 12-13% losses. Feb 2020 I was at $73k NW, March was $50k, April was $65k, May was $76k.. So 3 months to be pretty much back to normal. Let’s see if history repeats itself.

On that note I’m off to bed, need my beauty sleep. Surprised you made it this far. Personal finance isn’t always entertaining, it’s a series of calculated decisions, hard work, and some luck over time.

February 2026 was a month with a lot of unexpected household expenses. $1053 for a plumbing fix, $1738 for HVAC motor and capacitor replacement. That’s $2,791 in total and completely blew my budget. I’m satisfied with the quality of work done and the outcome is better than letting things just fester and get worse. That leaking pipe could have become a huge flood leading to much more expensive repair.

I got my tax refund back in record time it was aroud $913 thanks to mortgage interest. I didn’t get to enjoy a single dime of it. My net worth briefly surpassed the $500k mark but the expenses and some slight market declines made that all short lived. I think I can hit it by April though. Still up $95k in a year and almost $3k in a month

I sold my crypto and moved some money in savings to cover these home expenses. The crypto was a loss of around $191 and I’ll consider it a tax writeoff for the most part. My New HSA will allow me to invest once the balance hits $1k. I’m excited about that. The old one is in the process of being transferred to Fidelity but there may be a bit of a wait on that.

3/1/2026

1/31/2026

Difference

% Change

3/2/2025

YoY Diff

% Change

401K

$406,855

$404,137

$2,718

0.7%

$ 320,732

$ 86,123

26.9%

Roth IRA

$59,206

$58,801

$404

0.7%

$ 52,922

$ 6,284

11.9%

Brokerage Accts

$4,852

$4,614

$238

5.2%

$ 2,321

$ 2,532

109.1%

Cash

$11,161

$11,723

-$562

-4.8%

$ 14,303

$ (3,142)

-22.0%

HSA

$6,380

$6,380

-$1

0.0%

$ 3,537

$ 2,843

80.4%

Total

$488,454

$485,656

$2,798

0.6%

$ 393,814

$ 94,640

24.0%

Credit Cards

$0

$0

$0

#DIV/0!

$ –

$ –

#DIV/0!

Auto Loan

$0

$0

$0

#DIV/0!

$ –

$ –

#DIV/0!

Subtotal

$488,454

$485,656

$2,798

0.6%

$ 393,814

$ 94,640

24.0%

Mortgage

$337,077

$338,020

-$942

-0.3%

Zillow Estimate

$342,300

$343,200

-$900

-0.3%

Equity Estimate

$5,223

$5,180

$42

0.8%

Net Total

$493,677

$490,836

$2,840

0.6%

I’ve been back in the cycling mode since the weather here has been gorgeous. Bf sold a nightstand for $35 on marketplace and now the room it was in looks a lot more open.

I had to complain to the city again about the water meter leaking. Full of water and one of the plumbers was on her hands and knees with a whipped cream cup scooping out multiple gallons.

I went roller skating for the first time in months. This picture was taken before I fell

We also saw a show at Medieval Times.

Seeing The Great Gatsby with friends this evening, have heard positive things.

I really have been trying to replenish my emergency fund reserves. Thankful to have a job, a partner who supports me, overall good health. Look forward to some much needed vacation time.

Did my annual air filter replacements too, though this one looked pretty decent after a year.

Air Filters are super easy to replace, just two clips by hand and you’re in.

Last but not least I lost a friend from Long Island due to a car accident in February. He was only 42. It happened right around the corner from my parents home. I was devastated for a whole week. He had joined the NYPD in 2021, loved his job and seemed really optimistic about life. RIP Mike.

As we finish off January 2026 I’m just trying to mentally keep track of what has happened. Not that long ago we were celebrating the ball dropping and the new year. Now it seems like more and more of the same stuff, different day.

My employer filed for Chapter 11, and there were several changes from a senior leadership perspective. Operationally there were a few major changes too that I don’t really want to comment on. Hopefully that means my employment will be on stable footing over the long term. I was very anxious in the days / weeks leading up to it. Now it feels more like an ok that happened now what kind of experience.

A pipe in the house burst several days ago when we had a deep freeze. I thought we were in the clear but apparently I grossly underestimated things. It started with the hot water side of the kitchen faucet not working. Then one day it started working again all of a sudden. However not long thereafter we started seeing water on the kitchen and garage floor. We also heard water running from somewhere which prompted to me to look outside of the house. To my dismay there was hot water flowing down the side of the house into the snow / dirt. At this point it was around 6:30 PM and I wanted to at least call a plumber to get their feedback. They told me to collect water in buckets, etc to be able to flush the toilet and have some for drinking purposes until the matter could be resolved. However after we hung up the steet-level water shutoff did not work. So the water continued to run outside until I found a handle on the hot water heater that turned it off. Roughly 2-3 hours between the time we saw the flooding and the time it was turned off. The hot water inside stopped working completely before that so no time to shower.

Also…. one plumber came earlier in the day to give me an estimate and I showed her a water meter that was spraying water, she had zero interest in even touching that and told me to call the city… After the plumber came and I paid $900, I noticed very low water pressure. I called the city to have them look at the leaking water meter that day and no one showed up. The next day I called again and said I had low water pressure on top of the call from the previous day. They showed up in 15 minutes and were outside for roughly 4 hours. Hopefully I don’t get a bill later on but now my water pressure has been great since.

Who knew a small copper pipe could ruin my day?

3. Earlier in the month I decided to splurge and get some roof repair work done. One piece of roofing adjacent to the tree growing 3″ from the house and another further on the roof identified over the summer with visible hail damage. $775

4. Despite my additional expenses, I still enjoyed having fun driving in the snow and doing doughnuts. At least as much as an AWD almost 4,000lb vehicle would allow me to do in a parking lot without calling too much attention to myself.

5. To kick off things shortly after the year began my bf and I had brunch at Reunion Tower in Dallas. It was a lovely experience and I would go back again. Cheap no but within budget. It’s fun to live the high on the town lifestyle for a meal and then go back to the more affordable lifestyle in the suburbs.

6. When temperatures were much nicer in early January I took my trusty 2020 Cannondale CAAD 13 bike out for a ride on the trails. Really the only things I’ve replaced on it are tires / inner tubes, the seat, and water cages. The borderline crusty water bottles might be next, those plastics have a shelf-life.

7. I splurged on two shoes, one for workouts. The workout ones were $125 and biking ones were $86.34. I don’t feel guilty about these since the bike shoes were starting to split at the seams and are roughly 3 years old.

8. I am benefitting from having a DINK (Double Income No Kids) household though it doesn’t feel like it after the doozey of a month January has been. Having $1,675 come 100% out of my pocket with all the other expenses would be a real stretch once you add the $2890 mortgage, $150 electricity bill, $100 water bill, $80 internet bill, and the $625 per month extra going to principal. 9. Almost done with my tax preparation paperwork. It looks like I may get a small refund of a little under $1k. Thank you mortgage interest and itemized deduction. Hope to have most of it wrapped up in the next week.

1/31/26

12/30/25

Difference

% Change

2/2/25

YoY Diff

% Change

401K

$404,137

$402,229

$1,908

0.5%

$ 324,256

$ 79,881

24.6%

Roth IRA

$58,801

$57,765

$1,036

1.8%

$ 53,272

$ 5,529

10.4%

Brokerage Accts

$4,614

$3,423

$1,192

34.8%

$ 2,016

$ 2,598

128.9%

Cash

$11,723

$12,592

-$869

-6.9%

$ 11,975

$ (252)

-2.1%

HSA

$6,380

$6,343

$37

0.6%

$ 3,562

$ 2,818

79.1%

Total

$485,656

$482,352

$3,304

0.7%

$ 395,082

$ 90,574

22.9%

Credit Cards

$0

$0

$0

#DIV/0!

$ 166

$ (166)

-100.0%

Auto Loan

$0

$0

$0

#DIV/0!

$ –

$ –

#DIV/0!

Subtotal

$485,656

$482,352

$3,304

0.7%

$ 394,915

$ 90,741

23.0%

Mortgage

$338,020

$338,951

-$932

-0.3%

Zillow Estimate

$343,200

$345,200

-$2,000

-0.6%

Equity Estimate

$5,180

$6,249

-$1,068

-17.1%

Net Total

$490,836

$488,601

$2,236

0.5%

I started ramping up my investments into Brokerage accounts outside of my 401K / Roth IRA. I want my money to give me recurring income and capital growth…. Also not have to wait until 2043 to be able to access it. Especially with the way things are going with AI and my industry. You just never know.

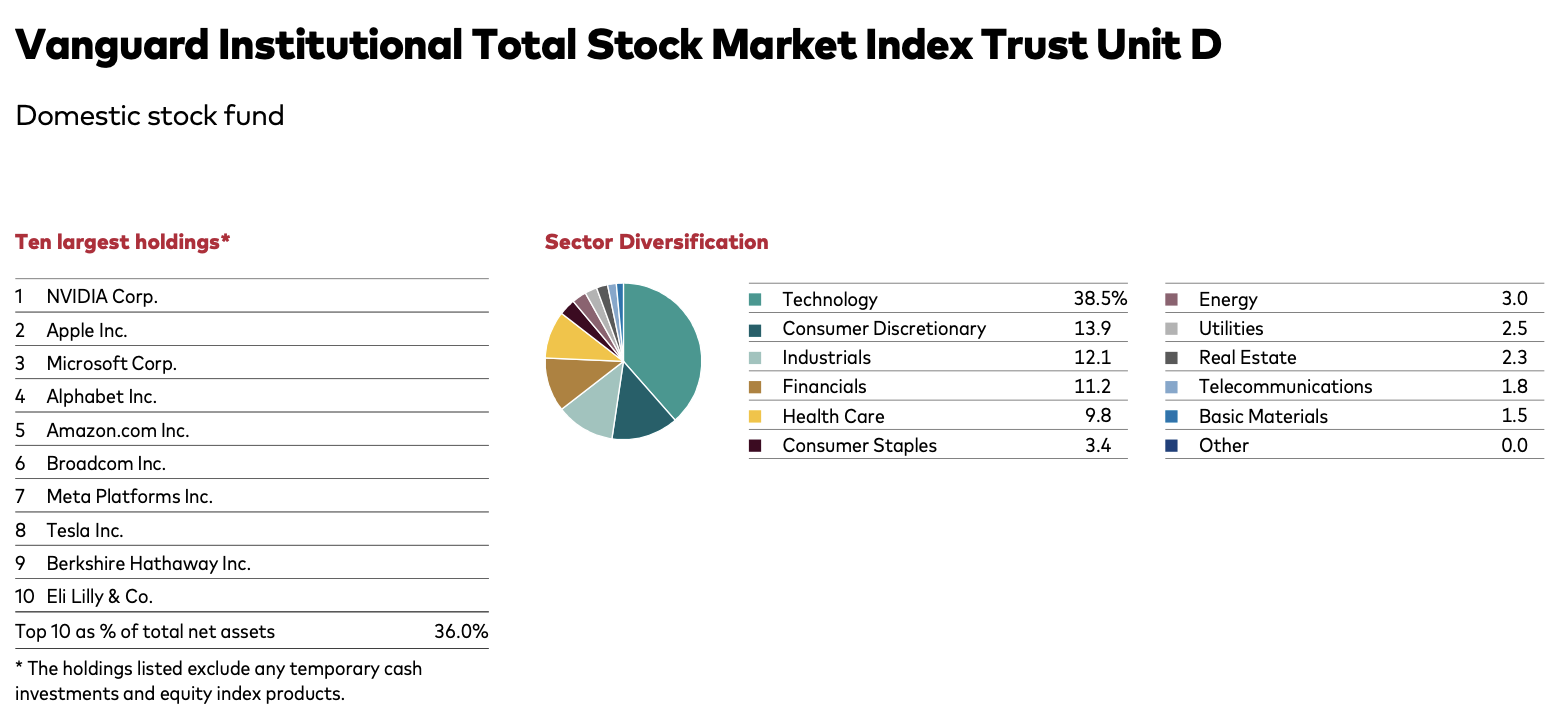

Brokerage #1 : $200/mo ($50 per week) goes in split 3 ways between a Bond ETF, Berkshire Hathaway BRK.B, Vanguard High Dividnet Yield ETD VYM. Brokerage #2 : $740/mo ($185 per week) goes into a mix of the following: BRKB ($99.56), GLD ($18.52 Gold), SCHY ($82.12 Schwab Strategic International), SLVR ($19.96 Silver), and the rest into FZROX ($611 Fidelity ZERO Total Market Index Fund). Silver just took a massive dump yesterday but I’m not discouraged. Dollar Cost Average or stop buying for a while. Are these going to make me a millionaire? Hardly but it’s something to get excited about. Could cover gas money, a utility bill, be another income stream if I fall on hard times, etc. Retirement #1: $576.92/mo ($144.23/wk ) goes into my Roth IRA. What I invest in is based on my mood that particular week but the majority of it is FZROX (94%), GLD (1.5%), SLV (1.2%), FEPI ETF (2.87%). I want to buy things here once and hold them over the long term. FEPI is generating me $36 of divideds monthly that gets reinvested. Retirement #2: $2,325 a month in 401k between my contribution and employer match. Most of this is in A Vanguard Institutional Total International Stock Market Index Trust, and about 5% in bonds.

Total Monthly: $3,842 | Total Annual: $46,103 Mortgage Monthly: $2,879 | Total Annual: $23,548 Extra Principal Monthly: $625 | Total Annual: $7,500 With those numbers above I think I’m doing as much as I can within reason. $77,151 for the year working on my financial future. Plus the $4,150 going to my HSA so really $83,301. That’s a lot of money. If I feel like I’m stretched too thin I can always change some things. And over $15k of that is through money my bf gives me toward expenses.

Overall I wish I was up more in the past month and $500k is still a stone throw’s away. Maybe next month if the market goes up. My ultimate freedom number is $2.5M. I’m happy my mortgage balance is down $932 in the past month. The interest is a pain in the pass so I’m going to keep doing the triple payments thing while investing and saving more.

In a year my net worth is up $95k or +24%. In a month I’m up $3.3k or .7%. Important to note all my 401k investments since the year began are not yet reflected in my balance. That’s being worked on and 99% likely will be fixed by the time I share my February update. I estimate I’d have another $2,300 between my contributions and the employer match.

Speaking of hard times Amazon went through a bunch of layoffs his week and there are rumblings of Oracle laying off a bunch of people. It fucking sucks no way around that. I hope I still have more time. Also hope 2 people I know recently impacted by layoffs get back on their feet soon. Hope you guys are safe out there and getting closer to your goals.

As I type this up I’m enjoying the tail end of a trip to West Palm Beach and Fort Lauderdale. The weather has been impeccable, warmth that I wouldn’t expect to see at the tail end of December. Yesterday hit a high of 82. People were jugging up and down the streets and boardwalk like we were in the thick of summer.

December was a good month for me financially. Hit my max 2025 contribution for the Roth IRA and 401K. Ended the month still able to have a $0 balance on my credit cards. The trip I’m currently on we did on a budget through discounts, credits. Food and some other things went on the credit card but it was only a few hundred split across the two of us.

Two of the paychecks this month didn’t have my 401k contributions taken out at all so that gave me a lot more disposable income.

I just started reading a book called Zero World Problems: New Standards of Living For the Post-Materialistic economy by Aaron Clarey who also wrote the book Black Man’s Guide Out of Poverty. For context I read that book in March 2017 when my net worth was closer to *$25k*. A lot of the material in the first section I was already familiar with but it is nice to revisit some of the core principals that will help me navigate my 40s/50s and beyond. Keeping up with the Joneses really does not make us happy.

So what happened in December 2025: 1. I got a car repair close to $260 including an oil change and replacing old hydroscopic brake fluid with new fluid to improve longevity of the entire system. A little more money than I wanted to spend honestly. I can always do oil changes at the Honda dealership for $59.95 after a coupon. I think I paid closer to $100 for that and that was after a coupon. Not sure about the brakes. Sometimes you just want to get in and out though, in this case I worked while they wrenched on the car.

2. I finally beat Baldur’s Gate 3 – This came I bought about a year ago and it wasn’t super expensive. Got over 480 hours out of it which is a bit embarassing to admit. I promptly deleted the game from my SSD likely to never touch it again.

3. Got these Thai needles in bulk. My bf’s first reaction was to send it back but hey if we have 6 months worth of noodles in the cabinet that saves both time and money as long as we use them. Plus I’d argue they’re a touch more healthy than the kind you buy from the restaurant covered in sauces and oils. 4. Unsuccessfully tried to assemble a wooden cabinet for the office that had super cheap pressed wood and disintegrated on me.

5. Bought these supermarket flowers that I just love. They made it about a week and half before tossing them but it adds a nice pop of color to the space.

6. Christmas / Holiday festivities – Wicked For Good didn’t disappoint though I made the mistake of seeing it while sleep deprived in a dark movie theater.

7. West Palm Beach / Fort Lauderdale trip – Took so many pictures. I’ll post a few of them here. Lots of fun new memories and a well needed break from Dallas.

In my last post I set a net worth estimate for the end of 2025 at $480k 8. My mortgage is now paid up until March 1, 2026 (2 payments of about ~$2900 Jan and February) so it looks like my cash balance has come down a lot. I noticed these prepayments aren’t reflected on my oustanding balance yet. I like having a little buffer. Starting next month I’m going to start with the triple principal payments (2 more than normal month) scenario I mentioned in my last post.

People often overerestimate what they can accomplish in a year and underestimate what they can in a decade. Since last month my net worth is up about $5,500 and in the last year I’m up $104k or +27%. A decade ago I was in the negative $14k net worth range. Past me never would’ve thought my numbers would go up by $500k. I hope the new year brings you good health, financial abundance, and happiness. I’m going into 2026 ready to rock and roll.

12/30/25

12/1/2025

Difference

% Change

12/27/24

YoY Diff

% Change

401K

$402,229

$397,992

$4,237

1.1%

$315,581

$ 86,648

27.5%

Roth IRA

$57,765

$56,073

$1,692

3.0%

$51,574

$ 6,191

12.0%

Brokerage Accts

$3,423

$3,074

$349

11.3%

$1,644

$ 1,779

108.2%

Cash

$12,592

$15,621

-$3,029

-19.4%

$11,896

$ 696

5.8%

HSA

$6,343

$5,869

$474

8.1%

$3,559

$ 2,784

78.2%

Total

$482,352

$478,629

$3,723

0.8%

$ 384,254

$ 98,098

25.5%

Credit Cards

$0

$0

$0

#DIV/0!

0

$ –

#DIV/0!

Auto Loan

$0

$0

$0

#DIV/0!

0

$ –

#DIV/0!

Subtotal

$482,352

$478,629

$3,723

0.8%

$ 384,254

$ 98,098

25.5%

Mortgage

$338,951

$339,258

-$307

-0.1%

Zillow Estimate

$345,200

$343,700

$1,500

0.4%

Equity Estimate

$6,249

$4,442

$1,807

40.7%

Net Total

$488,601

$483,070

$5,530

1.1%

Is this blog boring and repetitive? Maybe but slow and steady wins the race. 😀

On December 9th 2024 I posted: “Personal Finance happens in the background of the rest of my life. I’m also a believer that if you don’t set goals, you have nothing to strive for and it becomes very easy to get off track. My Net Worth target for the end of 2025 is $455k. These numbers are very conservative. Does not include 2 more paychecks this month and any additional income. $36-$37k with 401k matching, Roth max is about $3k/month. I have no $1400/mo car payment, no $200/mo Equinox membership, two big things I *did* have for a good portion of 2024. This year was unprecedented, I started off at $250k and as of last month was at $385k. It’s unlikely I’m going to see that kind of unprecedented growth. I found this old chart I saved in 2021 and updated it with my current numbers.“

Fast forward to today Dec 21, 2025. Here we are one year later. I own a house, I lost ~12lb. since the election last year. My bf now lives with me, we went to Europe and saw 5 different cities. My credit card balance is still $0. Personal finance is more at the forefront of my life than the backdrop. What’s Planned 1. I’d like to fund more future investments to helps support my lifestyle *before* I hit retirement age. The house is my biggest monthly expense with a mortgage of $2,880 so my investments will be focused on easing some of that burden. I will do a hybrid of dividend-based investments and index funds. I haven’t decided exactly how much I’m setting aside but it will be a big bump from the $50/week I’ve been doing spread across 2 taxable accts. I already started with some SCHD (Schwab High Yield Dividend Fund) – https://www.schwabassetmanagement.com/allholdings/SCHD and still own VYM (Vanguard High Dividend Yield ETF), US Treasury Bonds, and BRK.B (Berkshire Hathaway Class B shares). I get about $7/mo right now in dividends that get reinvested off a $1,780 acct.

2. Provided I have continuous employment for the year I will maximize 401k contributions to the tune of $24,500. Employer match came down slightly for 2026 but the plans offered are still funds I’d consider buying except from Vanguard through a broker instead of Fidelity.

3. Roth IRA will be maxed for 2026, that’s $7,500.

4. Replenish the emergency fund. 6 months would be ideal. That’s a balance of $18k at the bare minimum. Goal is to have that balance keep going up instead of treading water. Ballpark I’m thinking $700/mo. which will get me there by the Fall.

5. Triple principal payments – ~$620 of the $1300 my bf gives me monthly will go to mortgage principal each month. Combine that with the roughly $300 I’m making to principal in my regular payments will allow me to get rid of PMI a lot sooner. By default that would happen after 12 years of payments. Doing it this way could cut down to 4. Plus cutting back the total interest payments *significantly*. One year will be like making 3 years of payments. Having 2 incomes will drop the amount of money I set aside biweekly for mortgage payments from $1,450 to $1,110 or 23%.

Of course all of that is just speculative provided I still have a job for the duration of 2026. Hoping I do get another raise, if so it likely would kick in again in November. I also want to feel like I’m enjoying myself more, saving and investing everything isn’t fun.

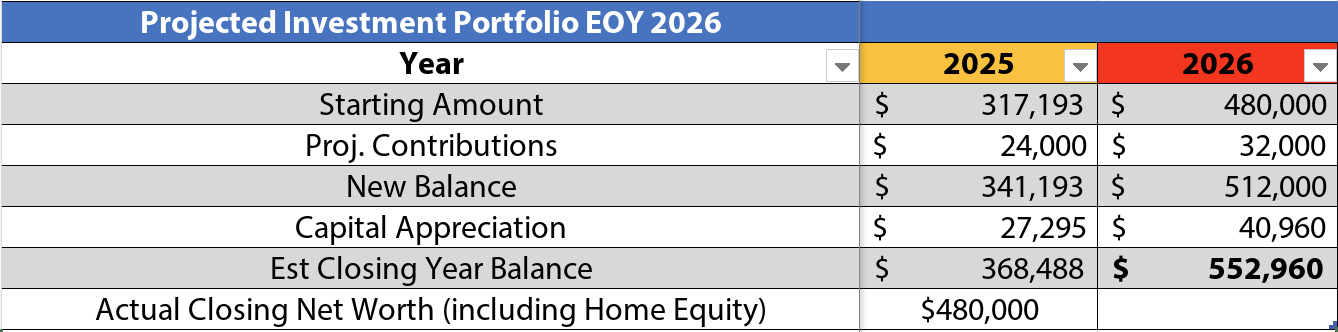

Onto the financial projections piece. My target last year for 2025 was to end the year with a net worth of $455,220. I exceeded that hovering around $480k right now

This is a super simple and conservative estimate but thinking I land north of $550k next year. I’m more likely to be up another $100k like I was last year but let’s not bank on that. Breaking the $500k ceiling will be a huge accomplishment for me from where I started out with. I want to be a good steward of what I have so I’m setup for the rest of my life. I’m well on that path. The median 60 year old has around $185k. At 42 I have $480k. I need some breathing room and my vacation can’t come soon enough. I took one day off since July for my mental health. Ok it’s 3am here and time for bed…

Today is September 4, 2025. Writing these blog posts a little bit different these days as a homeowner as opposed to renter. I successfully closed on my new home in early August 2025. 3 bedroom, 2 bathroom built in the 1970s. Close enough to Dallas to get there if / when I went to but far enough where the neighborhood is relatively quiet. My realtor who is a friend was super patient with me which I really appreciated along the journey. I didn’t feel pressured at all and a few of the properties I knew were a hard no right off the bat.

Nearly a month into the process I’m very happy with my decision and considering I just turned the ripe young age of 42 in August, I don’t think renting especially in that old apartment in that neighborhood fit my aspirations. Shortly after I moved out a woman was held at knifepoint at another complex down the block causing 12 police cruisers to show up. My immediate neighbor also wasn’t renewing her lease so that makes 2 of us. There were signs as soon as you turn down saying to lock up and basically be aware of theft. Started to feel like a third world country to be honest. Cars lined up and down the street, people repairing cars on the street, people speeding up and down the road blasting loud music.

With the purchase of a home comes along unexpected expenses and my situation is no different. Sharing a few pictures of my August experiences. I really did a lot in a month. Today I finished mowing the lawn for the third time I think? It grows super quickly in the back.

Cute goatsDFW SkylineMargaret McDermott BridgeReplaced the wiper blades and cabin filter as part of a quick weekend project

Proper maintenance of the exterior is of the utmost importance, so I needed to buy a lawnmower.Along with the lawnmower purchase were a weedwhacker and a leaf blower. The estimated cost for all these items was about $566.

Altogether the moving company cost roughly $890 including the tip if I recall correctly. They did a really good job getting all of my items packed onto the truck and delivering them without any noticeable damage.

I went through a bit of an ordeal trying to figure out how to properly connect the power cable from my electric dryer into the home.I thought I was doing something wrong but it turned out that the previous owner hired a contractor who installed a stove outlet instead of a proper 4 prong dryer outlet. We went back-and-forth for several days about them fixing it prior to my closing date. The work was never done which resulted in me making an emergency phone call to a local electrician who fortunately was able to arrive within an hour and finished up right when the movers were coming with all my stuff. The final cost of that was $265.

The home that I purchased had prior foundation work done earlier in the year. With that my online research found that it is highly recommended to transfer the foundation warranty from the previous owner to the current owner within 30 to 60 days. I jokingly say that was the most expensive piece of paper with a certificate on it that I’ve paid aside from my college degrees. $150, but I think it’s worth it for additional piece of mine and if god forbid I ever have to make a claim on the warranty.

Home essentials are also something that is important as far as making the space “livable”, That includes bedding, new towels, a step ladder, includes a 6 foot ladder to allow me to get to the roof. Also 2 $80/each custom made cellular window shades, lamp from Ikea. Estimated cost altogether I’d say is $650.

Furniture – Think I covered this last month but it was around $1100-1200. includes furniture for the living room area as well as a bookshelf, and a reading chair.

As far as an additional expense in terms of time involved/labor and less so the money aspect. I climbed up the ladder to remove a ton of debris from the gutters since I noticed when there was heavy rainfall, the water was literally just rolling off of the edge of the gutters my fear, if not quickly addressed, that would create water damage to something I wasn’t trying to deal with as a brand new homeowner.

During the middle of all of this, my semi estranged grandfather, passed away at the age of 89. I really struggled with this emotionally as I’ve not seen him in person over the last 16 years the most we’ve spoken to was approximately one hour in total, he also has not contributed to my life at all as an adult nor have I asked him to if I didn’t want to go to the service they had it would’ve been a 9 hour drive or alternatively a $700 round-trip flight. At the time no one was very communicative about whether there was even going to be a service or would it just be a viewing and that’s it. With all that said I did not go to my own grandfather’s funeral. I explained the situation to my mother, and she seemed OK with it. It was not made in haste since I just bought a house and haven’t even made the first payment having an additional expense of that scale for someone who barely made an effort… just wasn’t something that resonated in my soul. I also have never spoken to his wife or met her in person.

Temperatures in August are some of the hottest of the entire year in 2025 is no exception. Given that the square footage of this property is more than double what my apartment was so two are the projected electricity cost. That means for approximately three weeks of living here. We’re looking at an electricity bill of over $220 projected. Only recently have I taken additional measures that could help minimize that this includes some blinds that are blocking some of the light in the front two windows and using a dehumidifier, which should allow the AC to not work as hard to get the interior at the desired temperature.

Home security is another expense associated with homeownership. As a gay man living in a red state, and a minority on top of that, and not knowing any of my neighbors on top of that, I thought it would be best for me to get a home security set up with that. I did have to finance the equipment since I wasn’t buying it outright the cost of that including the labor, the equipment and taxes was approximately $2,900 (a big part of the CC balance)granted that is at a 0% interest rate. It still is considered an active/open credit line on my credit report. My goal is to pay extra as I go, but the financially smart thing to do would be to milk it as much as I can. There’s also a recurring cost for the service of the alarm of roughly $50 per month and I think it was also close to $60 per year to register with the city since that is a requirement since apparently there are a lot of false alarms.

Pest control was another item that I needed to take care of, this house is built in the 1970s and we’re in Texas. I’ve had experiences with carpenter ants and other ants infestations, at this house. There were some mosquitoes in the yard that we were trying to take care of, along with some ants near the window that kept coming inside. I do think one of the sprays I can smell inside when the fan is on. It was particularly strong at first though it is gradually starting to dissipate. I see dead ants on the floor, which is OK though there were quite a lot overtime I do think the previous owner did some type of pest control treatment prior to leaving. Roughly $65/mo

An upcoming expense that I may have is regarding exterior plants for the property. Haven’t decided exactly on what plants. I’m going to purchase but want something nice that hopefully isn’t going to die within the next month as the seasons change I’m not entirely how much that will cost, but we’ll see…

The water and sewage bill should come in the mail soon, I’m expecting that to be $70 dollars.

There are some additional expenses associated with throwing a housewarming party, but those are relatively minor. Let’s say $100.

Refrigerator – I bought a more affordable one from Best Buy but it was the wrong size so it had to get shipped back. The one I was able to get in a timely manner came from Home Depot to the tune of $1,358.52 including tax. That was under a special buy with $801 off.

Truck Rental – Rented a truck from U-Haul for a grill my friends gave me that doesn’t work. Cost was about $110 including gas.

Handle – One of the handles in the kitchen was missing on a cabinet, prompting me to find a replacement. I went to Lowes, I want to Home Depot. They almost matched but I ended up ordering line for a near perfect fit.

Saw these cute little goats out in Terrell, TX. I didn’t pet them but they were super adorable to look at and see especially the children’s faces light up.

Went to a potluck / pool party with friends early this week and really enjoyed myself. It’s fun to continue putting myself out there and experiencing new things.

It does feel like I have gone through a decent amount of money with all of the initial move-in expenses, but many of these are one time costs. Or items that will benefit me for several years minimum. I’ve been trying to cash flow things as much as possible. Fortunately, my first mortgage payment is due the start of October so that does give me a little bit of a buffer. The mortgage lender is going to be selling it to a different company to service, fingers crossed nothing gets mixed up along the way.

My net worth is down about $5k for the month which isn’t bad considering I bought a whole house. Still up about $106k for the year. In September 2020 my total net worth was only $96k, a *lot* can happen in 5 years.

9/1/2025

7/30/2025

Difference

% Change

8/31/2024

YoY Diff

% Change

401K

$366,372

$360,084

$6,288

1.7%

$ 289,322

$ 77,050

26.6%

Roth IRA

$50,470

$49,304

$1,166

2.4%

$ 45,392

$ 5,078

11.2%

Brokerage Accts

$1,636

$1,805

-$169

-9.4%

$ 22

$ 1,614

7336.5%

Cash

$15,420

$35,018

-$19,598

-56.0%

$ 2,032

$ 13,388

658.9%

HSA*

$5,220

$4,901

$319

6.5%

$ 3,574

$ 1,646

46.1%

Total

$439,118

$451,112

-$11,994

-2.7%

$ 340,342

$ 98,776

29.0%

Credit Cards

$3,245

$0

$3,245

#DIV/0!

$ 349

$ 2,896

829.8%

Auto Loan

$0

$0

$0

#DIV/0!

$ –

$ –

#DIV/0!

Subtotal

$435,873

$451,112

-$15,239

-3.4%

$ 339,993

$ 95,880

28.2%

Mortgage

$341,000

$0

Zillow Estimate

$351,000

$0

Equity Estimate

$10,000

$0

Net Total

$445,873

$451,112

Mid bike session was proud of myself that day 10 mile ride

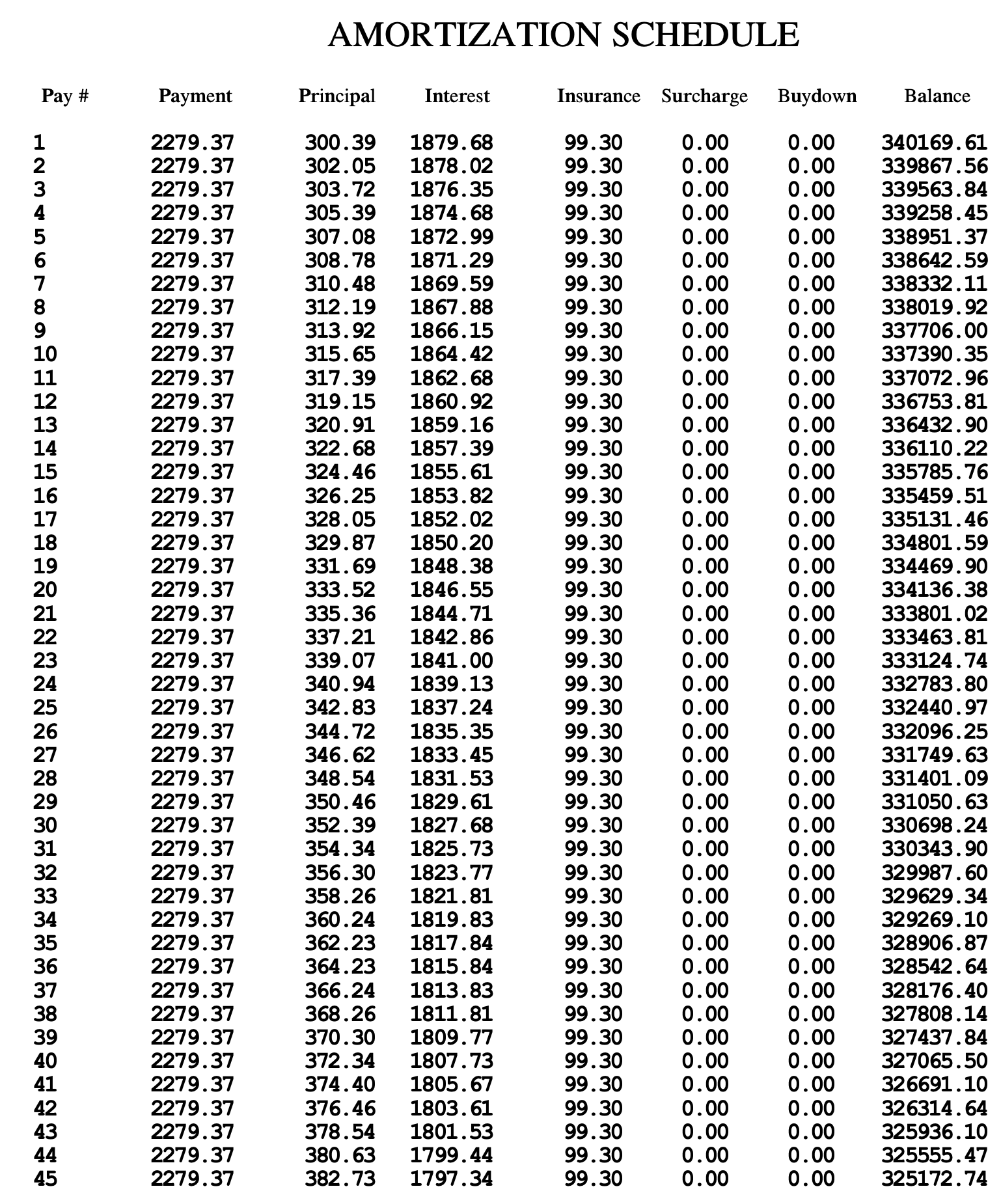

While I hate the idea of carrying extra, the alarm is at 0% so mathematically it makes no sense to pay it off early. Any money I add to principal on the mortgage will get me closer to eliminating PMI and lower my overall interest payments. And lessen the amount of time on the loan. However with the roughly $22k of interest for 2026, plus property $4k taxes, and $1200 of PMI of I would benefit from filing taxes under the itemized deduction.

Here’s a snapshot of my amortization schedule.

I asked Gemini how much extra I’d need to pay to have the mortgage gone by my target retirement age. This is what it generated: To pay off your $340,000 mortgage by October 2043, you would need to pay an additional $514.09 per month towards the principal.

This calculation is based on the provided amortization schedule and the goal of paying off the loan in 18 years (from October 2025 to October 2043), rather than the original longer term, which appears to be a 30-year mortgage.

Breakdown of the Calculation

Here’s how we arrived at that number:

Original Loan Details: Based on the amortization schedule, your original monthly payment for principal and interest is approximately $2,180.07. The annual interest rate is approximately 6.625%.

New Payoff Goal: To pay off the mortgage by 2043, the loan term is shortened to 18 years (216 months).

New Monthly Payment: To meet this new goal, a new monthly principal and interest payment of approximately $2,694.16 is required.

Extra Principal Payment: The difference between the new and original payment is the extra amount that needs to be paid each month:$2,694.16 (New Payment) – $2,180.07 (Original Payment) = $514.09 (Extra Monthly Payment)

By adding this extra amount to your monthly payment and ensuring it is applied directly to the principal, you can significantly shorten the life of your loan and save a substantial amount in interest over time. It is always a good practice to communicate with your lender to ensure any extra payments are correctly applied to the principal balance.

I also need to think about ways to boost my income. Even an extra $500 could go a long way consistently. Maybe a raise will be in my future? 😂

I did a bit of napkin math recently and discovered that outside of my house savings, retirement, rent, HSA, insurance and taxes I’m only living on about 25% of my gross income. That to me is a big sacrifice. On top of everything I’ve been doing the last couple years to get that retirement balance up.

Someone I have been watching videos from on YouTube for years recently lost her government job as a software tester and is now exploring options at temporarily leaving the United States. Matt D’Avella on YouTube also posted a video about why he was leaving the US due to healthcare costs and not really feeling a sense of community. I get that but also think there is a certain level of priviledge associated with it. When the average person can’t afford a $500 emergency, having resources to leave and be able to sustain one’s self is sort of a luxury. Also specific to Europe I’ve read that a lot of England residents are on public assistance. ~23% of pop vs 12.6 in the US.

Home – I see some of the prices beginning to drop. One home I liked went under contract with a contingent offer right after the price dropped around $25k. I felt like a missed out on a huge opportunity but to me even almost $300k is more than I want to spend. If it comes down another $25k that would seriously get me thinking about speeding up my timeline. $2,000/mo is what I’ve been setting aside the last few months and it’s rough doing that while also paying $1300/mo for rent. $3,300 and around $2500/mo going to retirement accounts. Some days I feel like I’m going to break from this short timeline. I easily could blow the money on something but that would be reckless for my future self.

One home in particular I adore the kitchen, but the driveway needs work as it has about 13 different cracks in it. It’s also a townhome with shared walls / roof and an HOA.

Another home is about $30k more or $330k but has so much natural lighting unlike my dark dingy 700 sq ft apartment. It’s a 4 bedroom 2 bathroom home and about 1300 sq ft. The kitchen is huge and the yard is nice too.

For a mere $20k more you can get a 4br/2ba that’s ~2000/sq ft but the interior needs a bit of work and things like the bathroom / kitchen cabnets need work. Some of the flooring looks a bit dated too. My bf and I drove to a few of the units I had looked at online. One was on the same block I lived just over a decade ago. The roads were halfway dug up and the city is putting in a new sewer system which was quite the eyesore. As happy as I was to be moving into a house back then as I’m older I think of how close some of the homes were to one another.

There was another home in the same community but a few blocks over without the road tore up that I liked. It has been on the market over 4 months though and was modernized quite a bit. I liked that it was 1900 sq feet, didn’t share a roof or wall with another building. Didn’t like that the wood covering the floor of the patio area was certainly in need of replacement due to how it it was designed. Or the slightly muddy backyard area but it did recently rain so that’s completely understandable. There is also no fence, instead just some bushes between the yard and the sidewalk which is right on a main road.

Why am I not taking action right now? I have about $17k in cash not $70k for a down payment which is considered ideal. That’s a huge gap. There was just a price cut of $6k roughly 2 weeks ago. It’s one of the more expensive units in the complex so I expect it to drop more. Based on my current forecast I’ll be at $41k in cash by the end of July. That’s enough for 20% on a $205k home which doesn’t exist at the moment. I still find myself thinking they want how much? For that? And at that interest rate? I know it makes me sound like a Boomer but if the math ain’t mathing I’m not going to just settle or be house poor.

There are a total of 3 people I know who live locally and are out of work. One was laid off around the holidays, another was laid off about a month ago, and a 3rd quit his job out of frustration. A once friend now acquaintance who owed my money posted recently a GoFundMe to get work done on his car. It’s been 20 years and the equvalent of about $730 in today’s dollars, don’t think I’ll ever see that money back.

April 2025

3/28/2025

3/2/2025

Difference

% Change

3/31/2024

YoY Diff

% Change

401K

$ 303,119

$ 320,732

$ (17,613)

-5.5%

$ 257,260

$ 45,859

17.8%

Roth IRA

$ 49,814

$ 52,922

$ (3,108)

-5.9%

$ 39,020

$ 10,794

27.7%

Brokerage Accts

$ 2,494

$ 2,321

$ 173

7.5%

$ 2,367

$ 127

5.4%

Cash

$ 17,209

$ 14,303

$ 2,906

20.3%

$ 3,392

$ 13,817

407.4%

HSA

$ 3,415

$ 3,537

$ (122)

-3.4%

$ 2,693

$ 722

26.8%

Total

$ 376,050

$ 393,814

$ (17,764)

-4.5%

$ 304,731

$ 71,319

23.4%

Credit Cards

$ 93

$ –

$ 93

#DIV/0!

$ 65

$ 28

42.9%

Auto Loan

$ –

$ –

$ –

#DIV/0!

$ 13,587

$ (13,587)

-100.0%

Net Total

$ 375,957

$ 393,814

$ (17,857)

-4.5%

$ 291,079

$ 84,878

29.2%

With all the volatility happening in the American economy it should come as no surprise that my net worth is down for the month. $17k to be exact. My cash is up close to 20% from last month though. I have thoughts on what’s happening but you’ve probably seen it a lot already before. I’m still up $85k to a year ago or +29% and am continuing to dollar cost average. My cash stockpile continues to grow to the highest levels they’ve ever been which I’m extremely thankful for. Most of my investing is on autopilot these days, trying to be an active investor in this market is risky and speculative.

March was a fun month, saw a Titanic exhibit, camping in Llano/Brownwood/Fredricksberg TX, saw Enchanted Rock, LBJ museum, some cool little shops. Replaced a dirty air filter in my car in 2 minutes flat. Finished up a season or cornhole and made it to the playoffs.

Here’s to April, hoping it doesn’t rain too much and I can enjoy the outdoors. It’s past my bedtime. Hope you are all healthy, employed, and not stressing about money. Having zero in student loans, credit card debt, no personal or business loans, and low overhead is a blessing.

If you follow social media closely you’d think we’re in the middle of the great depression. The current administration is doing layoffs left and right. Across NOAA, USAID, IRS, SSA, Labor Dept, EPA, NHTSA, FEMA, TSA, HUD, Dept of Defense, NIH/CDC, Dept of Energy, Dept of Education, Department fo Veterans Affairs, U.S. Forest Service, Personnel Management, National Nuclear Safey Admin, GSA, FAA. About 30,000 people most of whom were contributing valuable services to the nation.

Layoffs.fyi screenshot March 2, 2025

Let’s not forget the private sector, going off https://layoffs.fyi there have been a slew of them across many different sectors. Thousands more high paying mostly white color jobs wiped out in an economy where it’s harder to find a job than ever. With over 1.6 million unemployed looking for job and the process taking at least 6 months having you balance sheet right can mean the difference between being homeless or having cushion to lower stress.

For me, my employer last week went through a round of layoffs. I wasn’t directly impacted but there are people I’ve worked with over the years that were. It makes me sad and wonder will I be next. How do I make myself Indespensible to the team to show my value. Also what skills do I need to brush up on to add to my value in the marketplace. My job is far from perfect but I try to give it 100% daily and be an effective leader of people.

Mr. Money Mustache recently made a post Wow, have you seen the stock market lately? I encourage you to take a look at. TLDR is the S&P500 has had a crazy run up and we may be due for a correction. It’s still going to be profitable in the long run and the economy will continue to grow. Ignore the headlines, enjoy you life and keep on investing. I’m very much inclined to agree with him. I look back at the top news stories from 20 years ago. That was 7,300+ days ago. Most of the headlines elicit a wow that happened kind of response but aside from national disasters they don’t impact our day to day lives much. If your eyes are glued to the latest updates on X, Fox / MSNBC / CNN, etc. you’ll drive yourself insane. Give me the archive version and keep the party moving.

If I do end up getting laid off… 1. Company has a severence package in place – I’d rather not disclose the amt but it’s significant and would be close to 22 weeks worth of pay. 2. I currently have a stockpile of cash that I’ve been saving for a potential home purchase – Almost $12k 3. There are things I could sell for close to $1k if neded 4. I have a Roth IRA that I can pull from without penalties. My cost basis might not be exactly right but it’s close to $30k 5. 401k hardship distribution – Not ideal given the need to grow the investments, and 10% penalty 6. 401k loan Per Fidelity: With a 401(k) loan, you borrow money from your retirement savings account. Depending on what your employer’s plan allows, you could take out as much as 50% of your vested account balance or $50,000, whichever is less. An exception to this limit is if 50% of the vested account balance is less than $10,000: in such a case, the participant may borrow up to $10,000. 7. If I really really had to I could break my lease and move back in with parents 1600 miles away but that literally would be the option of last resort. 8. Unemployment would cover some of my expenses – Maximum weekly unemployment benefit is $577 available for up to 26 weeks. That’s $15k. 9 Sell my car currently valued at $34,400 on Carvana and get something 10 years old and significantly cheaper. A 2015 version of my vehicle is about $18k. That’s $16k right there.

Hopefully things stay secure and I never have to leverage any of the above options. I do believe in being prepared just in case. I’ve been keeping my momentum going on this blog for 13 years I don’t want to start going back now.

Enough about that, what the heck have I been up to the past month? 1. Filed taxes for 2024. I paid sooo much in taxes and still owed a little under $200. 2. Sold the wheels from last month on eBay. Got a few lowball offers and ended up settling at $85 plus the cost of shipping. My payout was ~$107. I’m not sure how the math works on that. I’m sure they’ll bill me for it again later. 3. Was getting over a bit of a nagging cough that wouldn’t go away. It’s 90% better now but super annoying and was at my whit’s end. 4. Covid / Flu shot – It’s the season of people getting sick including 3 people on my dodgeball team 5. Finished dodgeball – Fun season and I managed to avoid getting injured so that’s a plus. 6. Saw this cute art exhbit in Grapevine TX dedicated to Wicked. I saw the movie “only” once but go a little crazy with the soundtrack hahaha.

7. Getting back into the fitness journey flow. It tires me out sometimes but it beats the alternative option. I also am learning I don’t drink nearly as much water as I should be. My energy levels are higher, my skin is clearer, along with other benefits. 8. Friends and I did an escape room for a friend’s birthday and watched the Superbowl together. Kendrick Lamar deserves all the accolates he’s been receiving lately. Not Like Us and Humble are my jams.

Ok ok let’s talk about a net worth update.

3/2/2025

2/2/2025

Difference

% Change

3/1/2024

YoY Diff

% Change

401K

$ 320,732

$ 324,256

$ (3,524)

-1.1%

$ 247,070

$ 73,662

29.8%

Roth IRA

$ 52,922

$ 53,272

$ (351)

-0.7%

$ 37,111

$ 15,811

42.6%

Brokerage Accts

$ 2,321

$ 2,016

$ 304

15.1%

$ 2,189

$ 132

6.0%

Cash

$ 14,303

$ 11,975

$ 2,328

19.4%

$ 3,589

$ 10,714

298.5%

HSA

$ 3,537

$ 3,562

$ (25)

-0.7%

$ 3,067

$ 470

15.3%

Total

$ 393,814

$ 395,082

$ (1,267)

-0.3%

$ 293,026

$ 100,788

34.4%

Credit Cards

$ –

$ 166

$ (166)

-100.0%

$ 440

$ (440)

-100.0%

Auto Loan

$ –

$ –

$ –

#DIV/0!

$ 15,314

$ (15,314)

-100.0%

Net Total

$ 393,814

$ 394,915

$ (1,101)

-0.3%

$ 277,272

$ 116,542

42.0%

My net worth in the middle of the month got as high as $404k then with some of the recent economic updates it went down. Am I at the mercy of the markets? Yes and I’ve been recently trying to diversify slightly away from that while also leveraging Dollar-Cost-Averaging.

I’m not quite a dividend investor. However I am chugging along slowly with my 4-4.5% in a high yield savings account. So far my little balance has yielded my $80 since December. My FEPI investment (cost basis ~$1008 current value $942) paid $20 in dividends in Feb, $20.86 in Jan, $21.16 in late December. Mid December I got a $536 dividend payment from FZROX in my Roth IRA. For My 401k I Got a $3,079 dividend from FSKAX. I got a few other dividends, $7 here, $2.50 there. It all adds up

Am I bummed about my net worth being down from the start of February? Not really. $1k decline is really nothing in the grand scheme of things. I’m still up over $116k from where I was last year. I also expect to see extra income come through this month and will likely end up with 50% more cash than I have today. A year ago I had about 3 months rent set aside in cash. The average person would struggle to handle a $500 unexpected expense without using a credit card. Meanwhile I’m living the debt free lifestyle with a healthy amount of cash reserves. So even if the $2k/mo I’m setting aside on top of other expenses / investments makes me feel “forced poverty” sometimes, it’s for a good purpose.

Throughout the week I look at homes for sale, the prices are coming down. Currently there are 3 homes in the development I once lived in. They aren’t selling. The homes I think are nice average out to be about $385k most of them are 3 bedroom, 2 bathroom. That’s a $77k downpayment. I have 18% of that right now and my lease ends mid-August 2025. That’s basically 5 months away… 3 bedroom homes in the area:

So the next question… Do I need a 3 bedroom home for 2 people? Well, I do work from home and dedicated “office” space would be nice instead of working from my bedroom or living room. Plus if my partner moves in with me he should have his own space. Same for if my parents come to visit though that hasn’t happened in over 6 years…

2 bedroom homes: These two bedroom homes are priced a bit lower but not *that* much cheaper. I will say the some of these look a bit more modern. About $30k cheaper in some cases the savings are more. Those savings of $40k-$70k add up. I can look in other areas too, a change of pace could do me a bit of good.

I looked at condos in the area as an option, but one had an $812/mo. GTFO here with that nonsense. Another option had that fee at $609/mo. With the insurance included I guess it’s not soooo bad but stil let’s say that’s $200 of it. “All Facilities, Association Management, Insurance, Maintenance Grounds, Sewer, Trash, Water”. You don’t have a garage to park your car in, or a driveway and still have taxes on top of that. Another property it didn’t include insurance on for $451/mo. Then no guarantee they won’t jack up the HOA dues again the next month. These units also don’t move quickly. One property has been on the market for 190 days and they also historically don’t appreciate at the same rate as stand-alone homes.

I’m still looking and hoping the prices keep coming down more. There are so many units on the market right now. I also hope that I don’t lose my job since that could push things back a longggg time. In any case I’ll keep saving and to have the ability to do that I’m thankful. Going to focus on the things I can control and try to adapt to the ones I cannot to the best of my ability. Off to enjoy the rest of my Sunday now. Cheers!

Typing this one up a few early as I will be driving home from San Antonio New Years Eve. It has been quite a year, one which for me will go in the history books as my best year ever. Never before in my life has my net worth been this high before. To cross the $300k threshold and be a stone’s throw away from $400k. I am up $134k from the start of the year and mostly flat to where I started off December due to fluctuations in the market. When I started this blog I was negative $47k in debt, I saw the Sallie Mae / Navient loans show up on my credit report history. Those were some really dark days and I’m glad I drove myself to write about my struggles with that experience. No one cares about my finances as much as I do and that continues to be the case.

One of my bonuses came through last week and it all went right into my Wealthfront account. I moved money over from the Apple Savings account that paid a lower interest rate. With the sign up incentive I’m getting a sweet 4.5% APY until March then back to 4%. My primary financial institution money market pays only .2% and the checking is 0%. Would be .4% if I did a certain amount of debit transactions monthly but even on $2k that’s $80 for the year and risky if I run into any issues with fraud or need other protections. High yield is where it’s at. Here’s the link to Wealthfront if you want to sign-up and get an extra .5% for 3 months: https://www.wealthfront.com/c/affiliates/invited/AFFD-TFLJ-KLGR-FZTR

Car debt sucks but I give myself a bit pat on the back for paying mine off within a year. $17k isn’t chump change. I tell myself you can’t get a new one again until it hits 100k miles. I’d make an exception if the alternative gets more than twice the fuel economy.

Fancy gyms are a luxury – Will I go back to Equinox again? Only if I lived closer to one, $215/mo is still a shit ton of money to workout especially if you aren’t using all the amenties. Did I feel like a wealthy person going there? Sure. With personal trainers though you could easily double that cost per month. It was nice seeing Ferraris, high end Mercedes and Tesla SUVs in the parking lot.

Dogs are expensive, mine toward the end was close to $250/mo between vet visits / medication, grooming, food. Would I get another one? Yes but in a bigger space and it needs to be one that bonds with me.

Your home is your sanctuary. When I had the ant infestation that persisted for months I felt like a prisoner to a colony that did as it wished, invading my personal space, my kitchen, my laundry room area, the area around the front door. I bought some LED lights to give my place a little different vibe. Warm if I want, or any other range of colors in the RGB spectrum.

I don’t need to have the best of the best when it comes to tech. For both my laptop – in both size, memory, and cpu cores…and Phone – in terms of storage capacity I downgraded. Happy with both purchases. New AirPods Maxes came out but just a different connector with no other changes, new color for the same Apple Watch Ultra 2. I’d be a fool to drop cash on either product when mine is near identical.

Bf moving closer me to me has been a blessing. I was able to help him after a minor fender bended he experienced this month, we spend more time together in general, it’s been way easier to take him to work or run errands vs living in a bad part of Fort Worth.

With bad health you are poor. My blood pressure is a good example of that. When I was taking the medication my stomach was always upset. Then when I was off it my numbers were sky high, not far from where people would be admitted to the ER. Switched to a new one and it’s been working better.

Debt – I don’t villainize debt anymore the numbers just need to be in the right ratios relative to savings / investments and income. My unofficial rule is pay off all normal sized debt in a month, for anything that is more of a stretch pay it off in 3. I’ve also been incredibly blessed to have been steadily employed since 2013, something I don’t take for granted. I know 3 people who are looking for jobs right now. I’ve seen TikTok videos of people getting laid off right before Christmas. It’s rough out there.

Travel – Quebec, Toronto, Houston, Little Rock – Getting outside of my little 700 sq ft bubble has been extremely invigorating to my soul and I hope to do more travel.

Experiences – I can be a cheapskate but I very much appreciate a unique experiences. We went to a fancy restaurant in downtown dallas a few weeks before Christmas and plan to go another one on this coming trip. Holiday light shows, friends christmas parties. It can add up but after working hard for the entire year a little here and there on my salary, it isn’t going to break me.

Cash – Not physical cash but having money liquid. I’ll still max out my retirement accounts, but diversifying outside of that is a big part of my strategy into the new year. Will I have enough for a downpayment? Hopefully, but having all my money tied up to where I can’t access it until I’m 59 1/2 or longer just doesn’t sit well with me. This way I have runway if unforeseen circumstances occur or a buffer for my upgrade to a 2br or 3br place. I say place because home ownership #s just don’t jive with me yet. 20-25% lower we can talk but right now no deal.

In my 2025 Financial Goals post – My goal is to be up to $455k next year and I’m sticking to that. 18% or $70k higher than where I’m at now. If we hit an 8% Rate of Return that means “only” $38k more I have to earn / save to get there. Hope you’re all thriving out there. Here’s to 2025!

So it’s been a year since I said goodbye to my dog Sasha. It doesn’t carry the same level of sadness it once did but I am still reminded of her presence. Kind of thinking about getting a dog again, but not in the 700 sq. foot apartment.

I got a raise and bonus at work and feeling good about it. Is it life changing? Not exactly but it’s helping me keep up with inflation and I am extremely thankful to be receiving anything. Especially in today’s environment.

Last month I set a lofty goal to start saving $1k per paycheck toward my home fund. Have I been able to stick to that? Yes. I have $4k currently saved. FHA is 3.5% or $350k is $12k. I’m on track to have more than that by the time my 42nd birthday rolls around.

I’ve had a few celebrations and done some gifting but all of that was paid for any not much in the grand scheme of things. For his 31st birthday I got my bf mostly practical items and we went out to high tea at The Adolphus in Downtown Dallas. For a friend’s birthday we covered his dinner at Goldie’s, along with alcohol and drinks. Was it cheap? No sometimes you need to spend a little more for the experience and to return the kindness of others.

After much deliberation I’m keeping my 16″ MacBook Pro M3 Max. It’s got 48GB of RAM, 16 CPU cores, 40 GPU cores, 1TB of storage, beautiful screen. No need to drop $1300 on a new 14″ one that has very similar specs. Save / invest that money and when the next shiny thing comes out the current latest and greatest will be on sale. Heck there are people still rocking the M1 Max for professional needs and those came out 3 years ago. For next year’s Europe trip I can bring the iPad Pro with me and use it as “desktop” for a week and a half. Also I rarely push this system to the absolute limits and trying to get better at not leaving a ton of windows / tabs open in my browser. Also testing out the Brave browser instead which is much better than Safari with memory management. As I type this up, the CPU is about 90% idle.

Next week will be a trip to Hot Springs, Arkansas and probably Little Rock as well. Going to take a scenic drive and have never been to either city. Some nice restaurants, lots of sight seeing, hoping the weather cooperates.

Speaking of driving, I had an unexpected situation hitting some debris on a dark service road. Thought it was a brick or something to that effect. Oh this is a tiny item my car isn’t lowered or anything, surely it will clear it. I was mistaken and have a $301 bill to prove it.. The service cut me me a break, the original quote ws about $100 more. I tried to be extra nice and also got the other warranty work done so it was productive even though the lack of a loaner car for 4 days was a little bit annoying. The aluminum plate piece would scrape on the ground every time there was a little raised part of the road.

The kickball season has come to a close for me, it was fun to have plans on the weekend to do something outside of the apartment. It kind of gives me a little more life too, being around people in their 20s and 30s. Much more sense of adventure than I have sometimes. It’s eye opening how they were talking about $100k being a good salary to live off of in Dallas. I remember trying to hit that target for years and years. Then it happened. Now I don’t really realize I earn quite a lot compared to the average person.

FOMO is a real thing for me and I am not really where I expected to be at this age. Sometimes you work toward a goal and fall flat on your face. I am not letting that discourage me though. I will soon have the most cash I’ve ever had on hand since I had a windfall in 2022. I’m not used to not investing every single dollar and having a little bit left over. I do feel guilty about not maxing out my 401k. 35% of the money I don’t put in retirement is just going to the tax man. For a couple hundred in my pocket it’s not really worth it since I’m missing out on potential tax-deferred growth. So back to maxxing out I go.

11/1/2024

10/1/2024

Difference

% Change

401K

297,764

297,589

+175

+.1%

Roth IRA

47,977

47,091

+886

+1.9%

Brokerage Acct

882

549

+333

+60.7%

Cash

8,686

3,547

+5,139

+144.9%

HSA

3,490

3,465

+25

+.7%

Total

358,799

352,240

+6,559

+1.9%

Credit Cards

0

832

-832

-100%

Net Total

358,799

351,408

+7,390

+2.1%

Up $7,390 in a market that has recently taken some hits. There is a strong possibility of hitting a $400k net worth in the next year. Last year as proud as I was of my progress I was “only” at $217k so up 65% or $142k in a year. ::cough::

I don’t have anything to complain about right now. Saving toward a new place to live, my investment acct is up, I’m not letting money burn a hole in my pocket. I have a well paying job and a loving supportive partner. Losing a few pounds though I’m still up 40 pounds since covid and working from home. I didn’t gain it all at once so I can’t reasonably expect to lose it that quickly either. Steady consistent effort over time, that’s what it’s all about. That, not making dumb decisions, and a little bit of luck.

Still haven’t decided if I’m going to visit family in December since I basically have the week of christmas off. Weather is a big unknown but I do still have a Southwest credit that hasn’t been utilized. I’d also need to rent a car otherwise I’d be stuck at home with parents home most of the entire trip which also isn’t ideal.

I voted early last month, election day will soon be upon us. I wanted to find good reasons to support one side but kept coming up short. I’ll leave it at that. Also Harlan if you’re reading this I and probably others can’t leave any comments on your blog, I tried 3 times and it kept loading. 😛

I found my 1st grade school pictures from October 1989. That was 35 years ago and I remember most of that era at least from a 6 year old perspective. There is one person who I can’t remember the name of but everyone else is still around and doing well from what I can tell at least. Hope you guys and gals are doing well out there.

I also see Joe’s blog https://nomoreharvarddebt.com/ is public again even if it’s dormant. It’s still a good resource on how to think differently from society with personal finance even a decade later. Maybe the Gen Z crowd will discover some of the advice from your elders is good. 😉