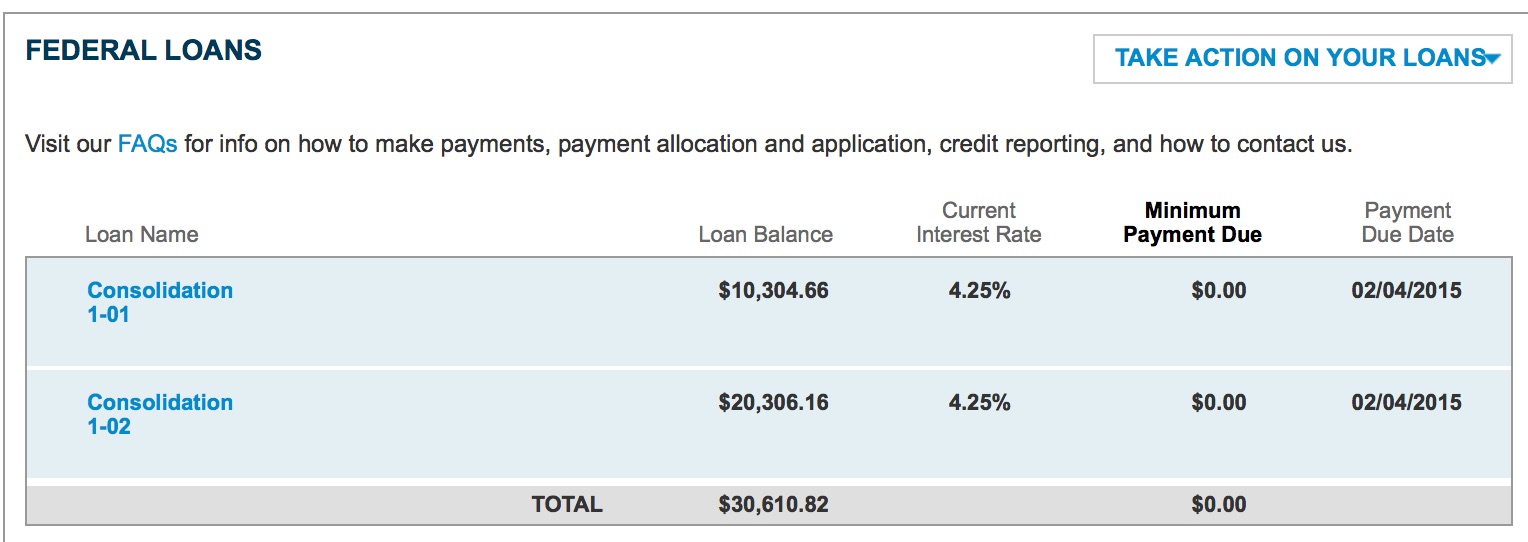

| 3/31/2023 | 2/28/2023 | Difference | % Change | |

| 401K | $173,931 | $167,673 | $3,611 | +3.7% |

| Roth IRA | $27,186 | $25,508 | $1,678 | +6.6% |

| M1 Acct | $770 | $663 | $107 | +16.1% |

| Cash | $3,135 | $3,635 | ($500) | -13.8% |

| HSA | $3,030 | $2,988 | $42 | +1.4% |

| Total | $208,053 | $200,468 | $4,938 | +3.8% |

| Credit Cards | $0 | $163 | $(163) | -100% |

| Auto Loan | $12,938 | $14,382 | $(1,444) | -10.0% |

| Net Total | $195,115 | $185,923 | $6,545 | +4.9% |

March was a rough month, effectively sick for over 2 weeks and still have a lingering cough. Overall I’m doing much better now but missed out on some activities with friends and felt like a total hermit. The brother of someone I went on a few dates with on and off over the years passed after getting tonsil surgery in his sleep. Dude was literally the same age as me too. Also a guy I dated before the pandemic and am friends with now is dealing with complications from a relatively procedure he had in early 2022 and having thyroid problems. He’s currently on medical leave, unable to work, and likely will have to undergo two, possibly 3 surgeries. An acquaintence of mine lost his job of 8 years working for an insulation company, he bought a house a few years ago he saved up a long time for. Hopefully he lands back on his feet soon.

My neighbors moved out, didn’t have anything bad to say about them other than the smoke that I had to complain about a few times since it vented into my unit. There are actually 5 out of 8 units in this building that will be available here between now and July. Can’t say I fully blame them, the price they want for a 1br ranges between $1,316 and $1,447. I pay $1,134 and presumably that amount is going to increase. For the last few months I pay my rent 3-4 weeks early so I don’t have to worry about it. When I get paid next week I’ll make the payment for May.

I’m happy that I was able to make a dent in my auto loan balance, it’s still a stretch to pay $1,444 in car payments in a month. $2,163.56 a month (including matching) is going in my 401k, $500+ a month in the Roth IRA and $100/mo in the M1 account. Up $6,545 in a month or 4.9% in a year. Net worth is essentially flat to a year ago which is good considering I bought a new car in October and financed $26k.

The overall state of the economy is still concerning to me, I see lots of doom and gloom content one day on YouTube and the next day the stock market is having it’s best year ever… Clickbaiting at its finest. Even Michael Burry of The Big Short fame said he was wrong. By following a lot of these folks you can miss out on major gains. Between capital gains, missing the best days of the market in any given year, and not dollar cost averaging due to fear. I would however keep adding to that emergency fund and maintain some diversity in assets (something I still need to work on). The layoffs at many big companies is very much a real thing however, seems like the numbers keep going up.

Lastly a bit of a rant… I see more and more people who don’t take personal accountability for their actions. I don’t know exactly what the root cause is but after how many years do you still blame your parents, society, a person of a different race, gender, orientation, insert the blank. People would rather point the finger than take action and focus their energy on improving their situation. I’ve been guilty of it too and try to remind myself in new situations that I might be my biggest obstacle.

Case in point was some bloodwork I had in March. The numbers aren’t good but knowing is a big part of the battle. Cutting back on sodium, alcohol, drinking more water, and eating more vegetables is how I will claw my way back. Also playing kickball again starting this afternoon and I’m super excited. Much love. Don’t give up the good fight whatever that may be for you.

The place gave me a quote for a dental cleaning + surgery removal that was been $900 and $1300. I decided that was too much and wanted a second opinion.

The place gave me a quote for a dental cleaning + surgery removal that was been $900 and $1300. I decided that was too much and wanted a second opinion.

The brings me to a combined total of $1,151.33. I love my dog, despite the huge vet bill. At least my card is 0% until May and I can probably pay this off in full within 30 days.

The brings me to a combined total of $1,151.33. I love my dog, despite the huge vet bill. At least my card is 0% until May and I can probably pay this off in full within 30 days.