I’ve decided to keep my Maxima to 150k miles possibly more. How many do I have now? About 3k. I put on average 15k/year so that’s 10 years. The 2003 I had made it to 196k before the last owner killed the engine. There is a guy on one of the car forums with an 09 that has over 300k miles.

150k is the sweet spot for a couple reasons.

It’s not high enough to the point that no one would consider buying it.

It’s two cars. Basically on my normal historic schedule that’s two cars. That means less total cost than trading and getting another one.

Still somewhat reliable with routine maintenance.

I can’t picture driving the same car over 10 years.

It makes dealing with depreciation mcouch more palatable.

It’s interesting to see YouTube celebrities talk about their (used) Lamborghini Gallardo or Dodge Charger Hellcat, err I mean Corvette z06. Those cars are 2.5-3x more expensive than mine. Not a hater but it’s a big mindset shift. For some the views they get cover the car note each month. Really makes me want to grab a GoPro or other camera secondhan, learn the ropes and start recording. The ideas are a brewing.

Several of my friends have made automobile purchases over the past two years. The names have changed to protect their identities.

Take Jordan. Jordan is in his late 20s, lives with his boyfriend. Has a Nissan vehicle that he bought used and is making payments. His payments are around 375/mo and his interest rate is about 15%. Some elements of Jordan’s life have changed and now he has a need to move out of this sedan and into an SUV. Jordan has poor credit due to mistakes made several years ago. Things have improved, but they are still far from ideal. If he buys another used vehicle he will get screwed over again with the financing because of a low FICO and high associated risk. The dealership he approached to buy another used model gave him horrible advice. The suggestion was he get out of his current car through a repo and just buy the one he wants beforehand.That way he doesn’t have to worry about making payments on two vehicles since no one wants to really buy a 5 year old car with 90k miles for what he owes.

My advice? See if a local credit union will allow him to refinance at a lower interest rate once his credit has improved. Or sell the car even though he is upside down, take a loan off to pay the difference and save enough cash to buy the SUV he really wants. In his situation, having another car loan and worrying about student loans and renting a house later this year is spreading him to soon. He will have to either get something really old like a ’99 Pathfinder or just make do with his sedan. I cannot in good faith encourage him to buy another car, the math just doesn’t work.

The next friend, we will call Adam. Adam’s situation is a little different. As a teenager his mother took out credit cards in his name, maxed them out and didn’t pay the bill. He also had one of his cars repoed several years ago when tough financial times hit. Adam is in his late 20s and recently bought a car just hours before we discussed his financial situation. Adam’s payments are ~$480/mo for 72 months on a used Kia that has a purchase price of $18k. The real kicker -his interest rate is 18%. Not 1.8%, not 6%, not 10%… 18%!!! I did some quick calculation. Over the course of his loan assuming he doesn’t refinance. His total payments will be over $34k. He said some people suggested he file for bankruptcy but that would be like a time bomb going off in his personal finances. I also believe Adam is making student loan payments, but not 100% sure.

I care about my friends, but don’t repeat their mistakes.

Cars should be something you get to enjoy, not a financial noose that makes it impossible to do anything else fun in life.

Anything over 6% interest rate on a car is insane.

Car loans over 60 months are also insane. If it takes you that long to pay it off you really can’t afford it.

Pay attention to your credit. It’s like an STD, bad past decisions can and *will* haunt you in the future.

Nothing with a motor should be more than half your gross income. I got that one from Dave Ramsey and pretty much agree. Cars will depreciate and going much above that will leave you car poor. Expenses such as maintenance / repairs, fuel costs, and insurance will eat up more cash than people who just focus on the payment will realize.

If you buy a new car and are younger, you may need to cut lifestyle elsewhere. In the case of both friends and myself, we eat out infrequently. Many millenials though are totally rejecting the idea of purchasing a car and getting into auto debt.

Credit. Protect it at all costs, ignoring it makes you much more of a slave to money due to all the interest.

Opportunity costs. Retirement planning, other activities to boost net worth. Jordan is going to college now and has a FT job. I doubt he has enough extra money to contribute into a retirement account. I have doubts about Adam contributing to his 401k because of his gripes about not having enough money to do certain things.

I’m lucky that my credit never got screwed up over the years, through my various trials and tribulations. My student loan is 4.25% and car is 1.9%. No credit card debt that carries from one month to the next. Not everyone is as fortunate. I hate paying more than I need to on anything. I used a 25% off first order coupon for Taco Cabana online. I buy items on Amazon if they’re cheaper than my local store.

It’s hard to watch people deal with financial pain, but at the end of the each day…we all make our own decisions.

No I’m not talking about Prince. Though his death was definitely a shock to me. I have listened to his music since the 1980s. Took me about a week to deal with it. Nor am I talking about my father who passed away at almost 11 years ago after 19 years of health problems related to kidney failure.

I’m talking about the death of someone else I knew. Someone I was really interested in dating. His name was Chris. He was only 29 years old. His birthday is two days before mine. Chris had his fair of struggles in life. He confided in me with a few of them. I really wished I was able to do more. We unfortunately lost touch with each other last June.

Yesterday I went to look him up on Facebook and found that he passed away just over a month ago. **One Month** I don’t know from what. I feel a sense of loss. I never met any of his family members. He wouldn’t let me get close enough to be a regular figure in his life. I tried a few different occasions. Work or other things going on his life got in the way. Wish I could hold him again and tell him to stay strong and that everything would be alright. He was a beautiful person inside and out, just wanted to see him at his true potential. Not working crazy hours at a hotel just to make ends meet. His family setup a gofundme page to help with burial expenses.

I’m just speechless. RIP Chris. You will be missed. Not just by me but by all the people you’ve touched. ❤

As I mentioned the last month… I did purchase a new car, am not relying on credit cards each month and putting aside more money toward emergency funds. As a result, I decreased student loan principal balance only by $592.32.

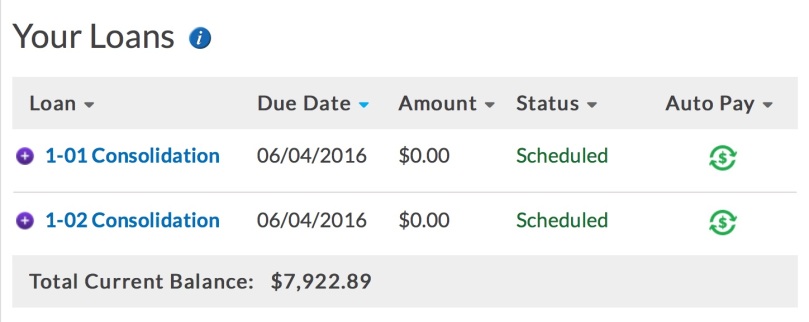

Navient: $7,922.89 @ 4.25%

NMAC: $31,188.19 @ 1.9%

Credit Cards – To be completely paid off by end of month

$69.08 (Costco Amex – groceries + gas)

$502.73 @ 12.24% (Chase card used for food / Amazon / utility items mostly)

$41.21 – Department Store card for mother’s day gift.

Total Credit Cards: $613.02

Total Debt: $39,724.10

Savings: $2800.02

This figure includes money earmarked for emergency fund, rent, car payments, etc.

Retirement:

401k – $15,166.29 – Up $1,691 since two months ago. Only $10,108 is vested.

Roth IRA – $3,315.10 with Betterment. My earnings are still -2.5%

Brokerage House – $564.07 – Down 10% due to AAPL. Might be a buying opportunity for more shares if it dips lower. Only own 6 shares which is about $3 a quarter in dividends.

Total Retirement – $19,045.46

As expected, my car insurance went up since buying the new car. $703.88 it was $592.95 before. For 65% more horsepower a 19% increase in premiums isn’t bad. I also switched everything over to e-policy to maximize my savings. Still have uninsured motorist coverage even though I have never been involved in an accident in my 15 years of driving. No tickets on my record for Texas and the ones I got in NY are no longer a factor.

Do I have any regrets about buying the car? Nope, it feels like a car that is truly made for me. Cockpit-like feel to the cabin, the effortless acceleration of the VQ engine, the exterior ground lighting, the LED daytime running lamps, no body roll in corners. Those shiny aluminum alloy rims on 245/45R18 Continental Procontact tires too. So much grip in the corners and 0-60 in 5.9 seconds. Put it in sport mode, the steering tightens up and the throttle is super responsive. The $30k 4DSC. Guy I work with with a Mercedes Benz CLA complimented me on the car, said he thought about getting one but it was 6 months too early.

2016 Nissan Maxima SV – Added $31k of debt but excites me every drive

I may be obsessed, I try not to park close to other cars and only wash it by hand with Optimum’s No Rinse car wash product. Was paying $40/week at the gas station wash with my black Altima and the results were mediocre. $15 at the regular car wash only to see a ton of swirl marks from their highly abrasive “soft touch” brushes. Now I do it all myself and can have the car completely done in 30 minutes. My absolute fastest washing the car by hand was 15 minutes. Yes I use a grit guard, microfiber towels and do a pre-spray to loosen up any dirt first, but…can’t recommend the product highly enough.

Last but not least… I decided to get serious about losing weight again. That was one the span of about a week. I threw my 6 individual packs of Famous Amos cookies in the trash. For breakfast I switched to eggs and protein (bacon, sausage or their veggie equivalents). For lunch I eat a salad and a protein source. I try not to go overboard with anything that has sugar. The protein fills me up and I crave the junk food less less. In 2015 I was 215 just to put things into perspective. The last time I did the ketogenic diet was 2012 and I got as low as 207. I was too extreme though with it and feeling dizzy all the time. Now I’m just being less hardcore while still enjoying carbs.

What good is money and fancy things if you aren’t in decent enough shape to enjoy it? This is after about a week.

Hoping to continue the trend and be in the 220s next week. Being fat and tired is not the way to live a rich, fulfilling life. Stay tuned. Thanks all for sticking around and reading all my posts.

Last but not least… Joe made a new post about 4 years later on No More Harvard Debt. Check it out. His book is pretty good too. My approach / situation / income varies but at my core I still enjoy not wasting money on things I don’t enjoy and cut back on things like food, entertainment and clothing to help reach my long term goals. Live With Passion! 🙂